Is It Too Late To Consider Moody's (MCO) After Recent Share Price Weakness?

Moody's Corporation MCO | 0.00 |

- If you are wondering whether Moody's at around US$448 per share is offering good value right now, or if the stock is already pricing in a lot of optimism, this article breaks that question down in plain terms.

- The stock is roughly flat over the last month with a 1.0% return. However, that sits against a 10.1% year to date decline and a 3.4% decline over the past year, following stronger 3 year and 5 year returns of 48.1% and 46.3%.

- Recent market attention on credit risk, debt markets and regulatory changes has kept rating agencies such as Moody's in focus. Investors are weighing how shifts in issuance activity and corporate borrowing conditions could relate to long term prospects. At the same time, discussion around financial sector regulation and capital markets activity has added another layer of context to the stock's recent moves.

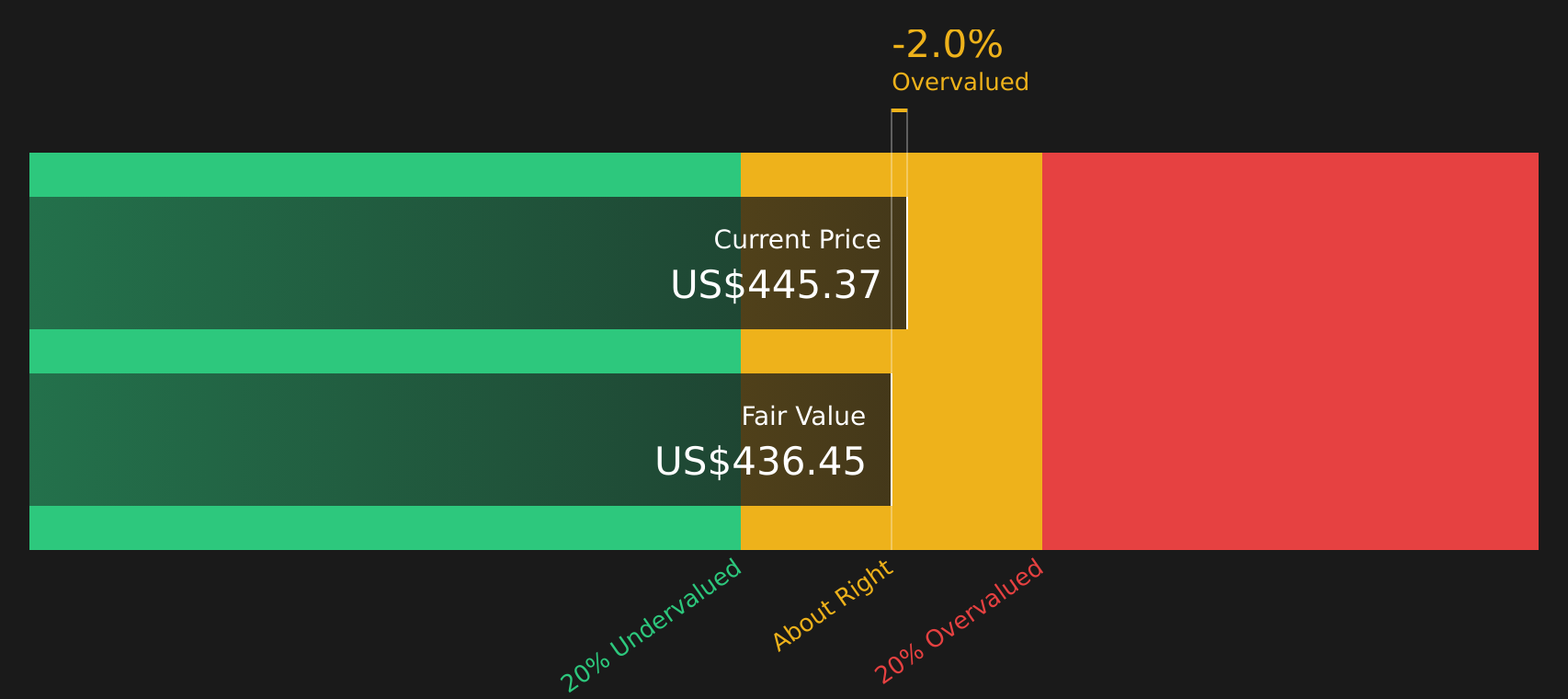

- Moody's currently has a valuation score of 1 out of 6, so only one of six checks points to the stock being undervalued. The next sections will walk through what different valuation methods indicate about that number, before finishing with a more holistic way to think about value at the end of the article.

Moody's scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Moody's Excess Returns Analysis

The Excess Returns model asks a simple question: are shareholders earning more on the equity in the business than they require as compensation for risk, and if so, how much is that surplus worth today?

For Moody's, the starting point is a Book Value of US$17.14 per share and a Stable EPS estimate of US$20.12 per share, based on weighted future Return on Equity estimates from 7 analysts. That implies an Average Return on Equity of 76.99%, which is above the modelled Cost of Equity of US$2.09 per share. The difference between what the equity is earning and what it costs, the Excess Return, is US$18.03 per share.

Using a Stable Book Value of US$26.13 per share, based on weighted future Book Value estimates from 5 analysts, the model capitalizes these excess returns to arrive at an intrinsic value of about US$431.07 per share. Against a current share price around US$448, this comparison leads to an assessment that Moody's stock is about 4.1% overvalued, which is close enough to the model's estimate that it sits within a reasonable band for long term investors.

Result: ABOUT RIGHT

Moody's is fairly valued according to our Excess Returns, but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

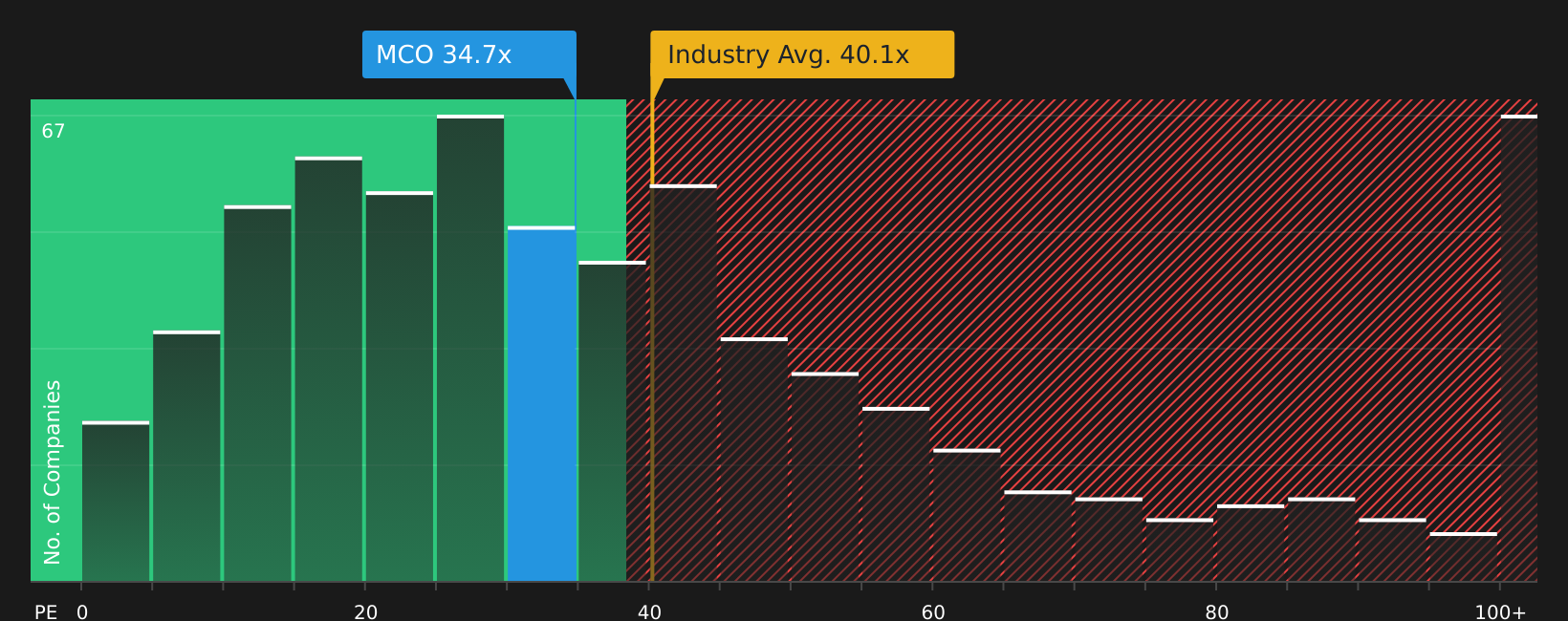

Approach 2: Moody's Price vs Earnings

P/E is a useful yardstick for a profitable company like Moody's because it links what you pay for each share to the earnings that the business is already generating. In general, higher growth expectations and lower perceived risk can support a higher P/E, while slower expected growth or higher risk usually point to a lower, more conservative multiple.

Moody's currently trades on a P/E of 31.4x. That sits below the Capital Markets industry average P/E of about 42.8x, but above the peer group average of 24.8x. Simply Wall St's Fair Ratio for Moody's is 17.2x, which is an estimate of what the P/E might be for the company, given its earnings growth profile, industry, profit margins, market cap and risk characteristics.

The Fair Ratio is more tailored than a simple peer or industry comparison because it adjusts for company specific factors instead of assuming that all stocks in the same industry warrant similar multiples. Comparing Moody's actual P/E of 31.4x with the Fair Ratio of 17.2x suggests that the stock is trading at a richer level than this model indicates.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Moody's Narrative

Earlier the article mentioned that there is an even better way to understand valuation. This is where Narratives come in. Narratives are a simple tool on Simply Wall St's Community page that let you combine your view of Moody's future revenues, earnings and margins with a fair value estimate, then compare that to the current share price so you can decide how to act when the two are far apart. Because Narratives update automatically when new information such as earnings, analyst revisions or news is added, you can see in real time how different storylines stack up. For example, one Moody's Narrative on the platform currently anchors on a fair value of about US$159 while another sits closer to US$551. This shows how two investors can look at the same stock, plug in different assumptions and end up with very different conclusions about whether the current price around US$448 looks attractive or not.

For Moody's however we will make it really easy for you with previews of two leading Moody's Narratives:

Fair value: US$551.41 per share

Implied discount to this narrative: about 18.6% relative to the recent price around US$448.64

Revenue growth assumption: 6.55%

- This bullish narrative leans on Moody's wide moat in credit ratings, high operating margins and returns on capital that exceed its estimated cost of capital.

- The author applies several valuation methods, including DCF, EPS growth, and historical multiples, to arrive at a fair value above the recent share price.

- AI risk and possible shifts in global regulatory trust are acknowledged, but the narrative views Moody's long established position and contractual stickiness as key supports for the investment case.

Fair value: US$159.00 per share

Implied premium to this narrative: about 182.2% relative to the recent price around US$448.64

Revenue growth assumption: 13.76% decline

- This more cautious narrative highlights how valuable Moody's regulatory position and data assets are, while still judging the stock price as too rich against a lower fair value estimate.

- It focuses on the ratings business and analytics software as entrenched, cash generative assets, but weighs those strengths against assumptions for future free cash flow and required returns.

- The author frames the view as a disagreement with higher implied multiples, treating the stock as expensive relative to modeled future cash flows and an assumed hurdle rate.

These two Moody's Narratives give you a clear range of viewpoints, from a higher fair value anchored in multiple valuation methods to a more conservative one that leans on strict return hurdles. Once you have seen both, you can decide which assumptions feel closer to your own and adjust your expectations for the stock accordingly.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Moody's on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Moody's? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.