Is It Too Late To Consider NXP Semiconductors (NXPI) After Strong 1 Year Share Gains?

NXP Semiconductors NV NXPI | 0.00 |

- If you are wondering whether NXP Semiconductors stock is offering solid value at its current price, it helps to step back and look at what the recent share performance and fundamentals are really telling you.

- The stock last closed at US$321.88, with returns of 10.7% over the past 30 days, 45.5% year to date, 56.2% over 1 year, 82.5% over 3 years, and 78.3% over 5 years, although it did slip 2.2% over the past week.

- Recent news coverage has focused on how NXP Semiconductors is positioned within the broader semiconductor sector and how investors are weighing that positioning against ongoing demand for its products. This context is important when thinking about whether recent price moves reflect changing expectations for the business or simply shifts in sentiment toward the sector.

- NXP Semiconductors currently has a valuation score of 3 out of 6, which means some checks flag the stock as potentially undervalued. The next sections will walk through different valuation methods and then finish with a broader way to think about what this score really means for you.

Approach 1: NXP Semiconductors Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes estimates of the cash a company could generate in the future and discounts those back to today, aiming to show what that stream of cash flows might be worth now.

For NXP Semiconductors, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month free cash flow is about $2.31b. Analyst and extrapolated estimates have free cash flow reaching $5.50b by 2030, with interim projections between 2026 and 2035 ranging from roughly $3.60b to $7.23b, all expressed in dollars and discounted back to today.

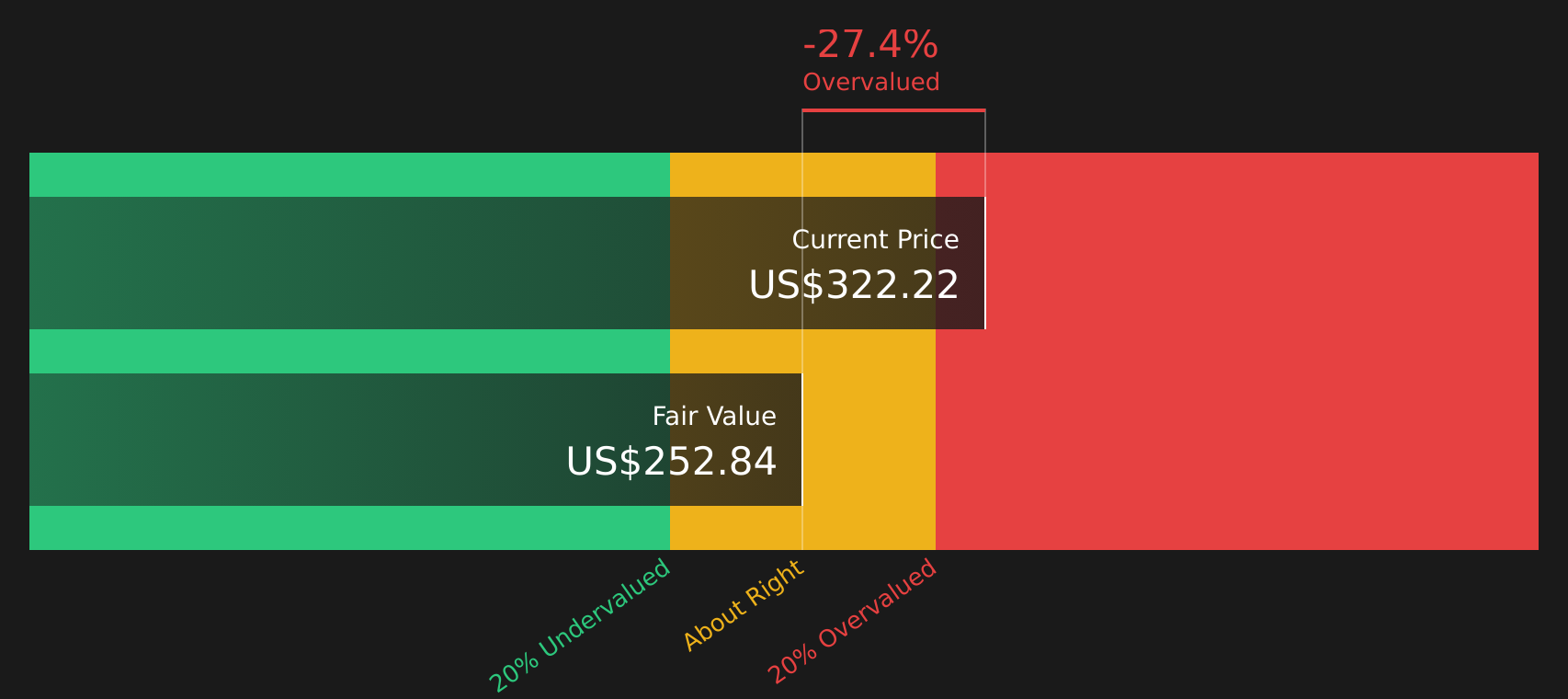

Putting these projections together, the DCF model arrives at an estimated intrinsic value of about $256.45 per share. Compared with the recent share price of $321.88, this implies the stock is trading at roughly a 25.5% premium to the DCF estimate. On this particular cash flow model, NXP Semiconductors stock appears overvalued.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests NXP Semiconductors may be overvalued by 25.5%. Discover 47 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: NXP Semiconductors Price vs Earnings

For a profitable company, the P/E ratio is a straightforward way to think about what you are paying for each dollar of current earnings. Investors generally accept that higher growth and lower perceived risk can justify a higher P/E, while slower growth or higher risk usually point to a lower, more conservative P/E range.

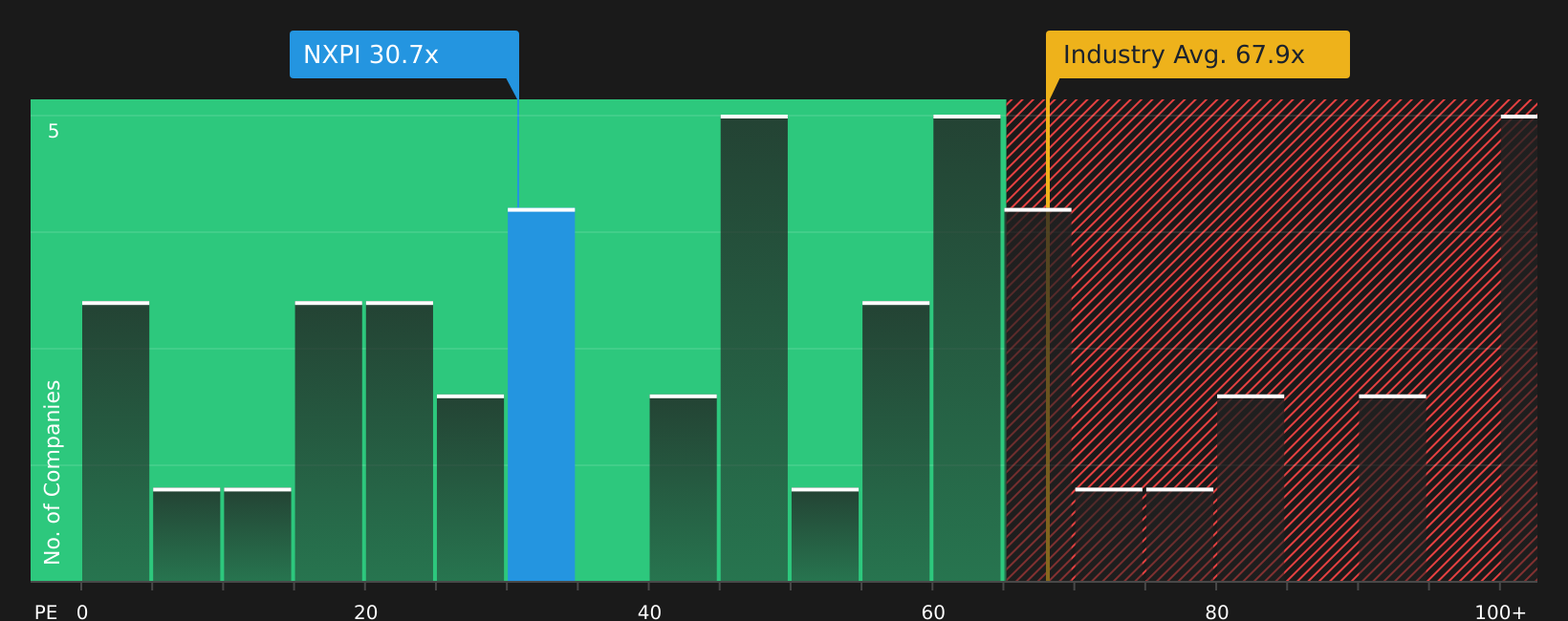

NXP Semiconductors currently trades on a P/E of 30.63x. This sits below the broader Semiconductor industry average P/E of 68.35x and also below the peer group average of 84.65x, so the stock is pricing in a lower multiple of earnings than many sector peers. Simply Wall St’s Fair Ratio for NXP Semiconductors is 40.65x, which is its proprietary estimate of what a more appropriate P/E could be, given factors such as earnings growth, profit margins, industry, market cap and company specific risks.

Compared with a simple industry or peer comparison, the Fair Ratio is designed to be more tailored to the company by adjusting for those fundamentals and risk factors rather than assuming all Semiconductor stocks deserve similar multiples. Since the current P/E of 30.63x is below the Fair Ratio of 40.65x, the stock screens as undervalued on this P/E based approach.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your NXP Semiconductors Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so this is where Narratives come in as a simple way for you to attach a clear story to your assumptions about NXP Semiconductors and then link that story to a forecast and a fair value estimate.

A Narrative on Simply Wall St is your version of NXP Semiconductors in story form. You spell out what you think happens to revenue, earnings and margins, and the platform turns that into a financial model with a Fair Value that you can compare directly with the current share price to help decide whether the stock looks cheap or expensive to you.

These Narratives live on the Community page and are used by millions of investors. They update automatically as new data arrives, so when fresh earnings or news hits, the numbers and the gap between Fair Value and price refresh without you rebuilding everything from scratch.

For NXP Semiconductors, one investor might align with a more optimistic Narrative that points to a Fair Value around US$371.24, while another might lean toward a more cautious view closer to US$200. Seeing those side by side helps you decide which story best matches your expectations before you act.

For NXP Semiconductors, however, we will make it really easy for you with previews of two leading NXP Semiconductors Narratives:

Each one reflects a different view on how fast the business could grow, what margins might look like, and how that could line up with today’s share price. Use them as starting points, then adjust the story to match your own expectations.

Fair value in this bullish Narrative: US$371.24 per share

Implied discount to this fair value at the last close of US$321.88: about 13.3% below the Narrative fair value

Assumed annual revenue growth: 14.25%

- Sees edge AI, automotive software, and higher semiconductor content in vehicles and industrial automation as key drivers for higher revenue and margin potential over time.

- Assumes operating efficiencies, cost control and localized manufacturing support higher operating leverage and more resilient earnings.

- Recognizes risks from geopolitics, sector concentration, competition and regulation, but views these as manageable within a higher fair value of about US$371.24.

Fair value in this more cautious Narrative: US$298.29 per share

Implied premium to this fair value at the last close of US$321.88: about 7.9% above the Narrative fair value

Assumed annual revenue growth: 10.36%

- Places more weight on modest demand recovery, auto exposure and intense competition in China, which could keep growth closer to consensus expectations.

- Assumes disciplined cost control and acquisitions help earnings, but also flags that higher expenses and integration risk could pressure margins.

- Arrives at a fair value around US$298.29, with analysts on average viewing the stock as close to fairly priced on these assumptions.

These two Narratives give you a clear range of outcomes, from a higher growth, higher fair value view to a more conservative, closer to consensus setup. The key step now is to decide which assumptions feel more realistic to you, then adjust the revenue growth, margin and valuation inputs until the story lines up with how you see NXP Semiconductors.

Once you have that, you can track how new earnings reports or news affect the gap between your fair value and the market price, rather than reacting only to short term share moves.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for NXP Semiconductors on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for NXP Semiconductors? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.