Is It Too Late To Consider Par Pacific Holdings (PARR) After Its 255% One Year Surge?

Par Pacific Holdings Inc PARR | 0.00 |

- If you are wondering whether Par Pacific Holdings at US$62.25 is still attractively priced after a strong run, the next sections will walk through what the current market price may be implying about the stock.

- The share price has pulled back with a 5.2% decline over the last week and a 3.7% decline over the last month, even though the year to date return stands at 73.8% and the 1 year return at 255.1%.

- Recent news coverage has focused on Par Pacific Holdings as an oil and gas refiner and marketer listed on the NYSE. Investor attention often centers on how changing energy market conditions feed into refining margins and asset values. These themes help frame why the strong multi year share price performance of 192.4% over 3 years and 379.2% over 5 years is now being weighed against questions about what is already priced in.

- On Simply Wall St’s 6 point valuation checklist, Par Pacific Holdings currently scores 5 out of 6. Next comes a closer look at traditional valuation methods like P/E and discounted cash flow, and then a different way of thinking about value that brings the story together at the end of the article.

Approach 1: Par Pacific Holdings Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth by projecting the cash it may generate in the future and then discounting those cash flows back to today’s value.

For Par Pacific Holdings, the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month Free Cash Flow is reported at about $280.4 million. Analyst and extrapolated projections, all in $, include a forecast Free Cash Flow of $244 million in 2029, with a full set of annual estimates and extrapolations out to 2035 supplied to the model.

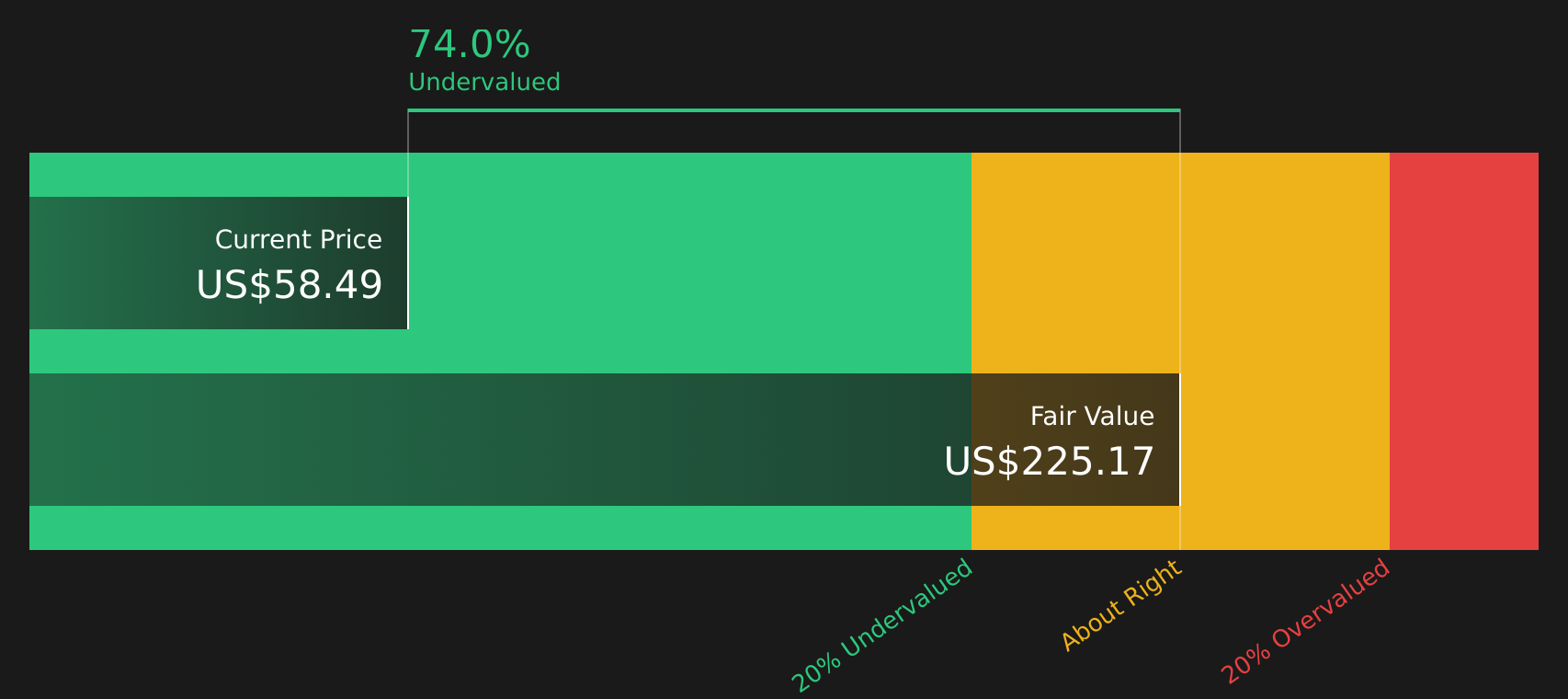

Based on these cash flow projections, the DCF model points to an estimated intrinsic value of about $123.63 per share, compared with the current share price of $62.25. That implies the stock is about 49.6% below this intrinsic value estimate, which indicates that the model’s assessment of value is higher than the current market price.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Par Pacific Holdings is undervalued by 49.6%. Track this in your watchlist or portfolio, or discover 51 more high quality undervalued stocks.

Approach 2: Par Pacific Holdings Price vs Earnings

P/E is a common way to value profitable companies because it links what you pay for each share directly to the earnings that support that share price. In general, higher growth expectations and lower perceived risk can support a higher P/E, while lower growth expectations and higher risk usually line up with a lower, more cautious P/E range.

Par Pacific Holdings is trading on a P/E of 6.78x. This sits well below the Oil and Gas industry average P/E of 14.20x and is also below the broader peer average of 14.21x. On the surface, that kind of discount can suggest the market is pricing in lower growth, higher risk, or more cyclical earnings than the average peer.

Simply Wall St’s Fair Ratio for Par Pacific Holdings is 13.40x. This is a proprietary estimate of what a “normal” P/E could be, given factors such as earnings growth, industry, profit margins, market cap and company specific risks. Because it looks at those drivers directly, the Fair Ratio can be more tailored than a simple comparison with peer or industry averages. With the current P/E of 6.78x sitting well below the Fair Ratio of 13.40x, the stock screens as undervalued on this metric.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Upgrade Your Decision Making: Choose your Par Pacific Holdings Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so meet Narratives, a simple tool on Simply Wall St's Community page that lets you attach your own story about Par Pacific Holdings to a set of numbers like fair value, future revenue, earnings and margins. You can then compare that fair value to the current share price and see how it stacks up against other investors. For example, some might see a US$80 fair value based on steady margins, share buybacks and an 11.1x future P/E, while others might anchor on US$40 with softer revenue assumptions and an 8.8x future P/E. All of this information is kept up to date as new news, forecasts and earnings are added.

For Par Pacific Holdings, however, we will make it really easy for you with previews of two leading Par Pacific Holdings Narratives:

These narratives sit on opposite sides of the debate. Reading both can help you decide which set of assumptions feels closer to your own view before you look at the latest share price or valuation models again.

Fair value used in this bullish narrative: US$80.00 per share

Implied undervaluation vs last close: about 22.2% below this fair value

Revenue growth assumption in the model: 53.1%

- Focuses on partnerships, industry consolidation and logistics integration that support margins, pricing power and cash flows across refining and retail.

- Assumes earnings in the model are supported by steady profit margins, a higher P/E of 11.1x by 2029 and ongoing share count reduction through buybacks.

- Flags risks around decarbonization policies, geographic concentration, refinery upgrade costs and leverage, and encourages you to test whether those risks change your own fair value.

Fair value used in this bearish narrative: US$40.00 per share

Implied overvaluation vs last close: about 55.6% above this fair value

Revenue growth assumption in the model: 5.7% decline

- Highlights headwinds from electric vehicle adoption, stricter emissions rules and concentrated, aging assets that could pressure throughput, margins and free cash flow over time.

- Builds a case around lower future revenues, slimmer profit margins at 3.8% and a P/E of 8.8x in 2029, which together anchor the US$40.00 fair value.

- Notes that stronger renewable fuel partnerships, resilient regional margins and solid liquidity could challenge this cautious view, so you are asked to weigh how likely those offsetting factors are.

If you want to go beyond these previews and see how the bullish and bearish numbers compare line by line, including earnings, margins and valuation assumptions, it is worth reading the narratives in full alongside the latest data on Par Pacific Holdings.

Do you think there's more to the story for Par Pacific Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.