Is It Too Late To Consider Philip Morris International (PM) After Its Strong Multi‑Year Rally?

Philip Morris International Inc. PM | 0.00 |

- Wondering if Philip Morris International at around US$188.99 is pricing in too much optimism or still leaving room on the table for value-focused investors.

- The stock is roughly flat over the past week with a 7-day return of a 0.3% decline, but sits on a 15.1% gain over 30 days, 17.9% year to date and 9.8% over 1 year, which puts recent moves in clear contrast to longer-term performance including a very large 3-year return and a 148.5% return over 5 years.

- Headlines around Philip Morris International often center on its product portfolio, regulation and its role in the global tobacco sector, which can all influence how the market thinks about risk and long-term cash flows. These themes help frame why the stock price can shift even when there is no single, company-specific catalyst in play.

- Despite all of this, the company currently has a valuation score of 1 out of 6, so next comes a closer look at what traditional valuation methods say about Philip Morris International, followed by an even more comprehensive way to think about what the stock might be worth.

Philip Morris International scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

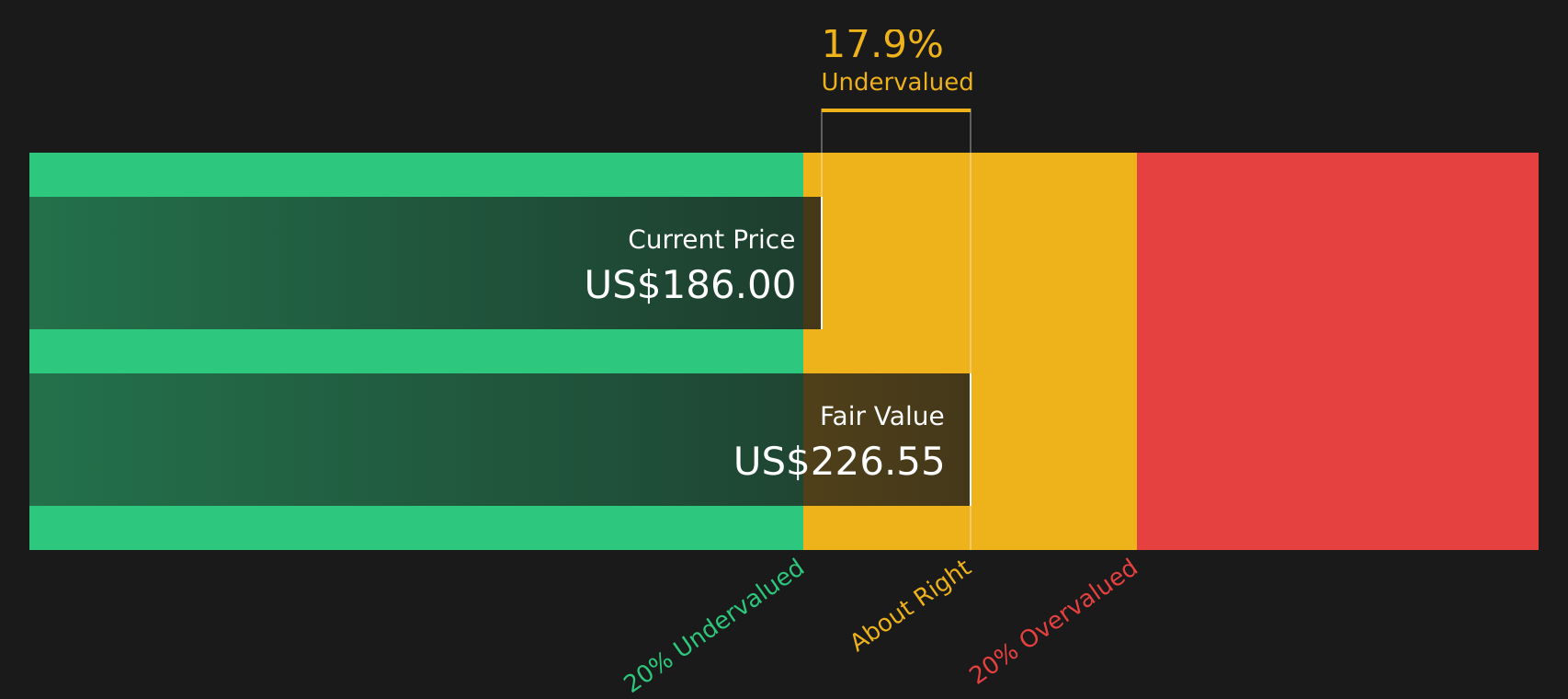

Approach 1: Philip Morris International Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth by projecting future cash flows and discounting them back to today using a required rate of return. It is essentially asking what Philip Morris International’s future cash generation is worth in today’s dollars.

Philip Morris International most recently generated trailing free cash flow of about $10.60b. On Simply Wall St’s 2 Stage Free Cash Flow to Equity model, analysts supply near term estimates, then further cash flows are extrapolated. For example, free cash flow is projected at $13.53b in 2025, with a series of projected figures through 2035 that generally sit around the $11b to $15b range, all expressed in $ and discounted back each year.

Adding these discounted cash flows together gives an estimated intrinsic value of $161.82 per share, compared with a current share price of about $188.99. That gap implies the stock is assessed as around 16.8% above this particular DCF estimate, suggesting limited margin of safety on these assumptions.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Philip Morris International may be overvalued by 16.8%. Discover 49 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Philip Morris International Price vs Earnings

For profitable companies, the P/E ratio is a useful way to think about what you are paying for each dollar of current earnings. It ties the share price directly to the bottom line, which is usually more stable than revenue alone and more meaningful than asset values for ongoing businesses.

What counts as a “normal” or “fair” P/E depends on how the market views a company’s prospects and risks. Higher expected growth or lower perceived risk can support a higher P/E, while lower growth expectations or higher risk tend to justify a lower one.

Philip Morris International currently trades on a P/E of 26.6x. That sits above both the Tobacco industry average P/E of 12.4x and a peer group average of 20.5x. Simply Wall St’s Fair Ratio for Philip Morris International is 26.9x, which is a proprietary estimate of what the P/E might be given factors such as earnings growth, profit margins, industry, market value and risk profile. This Fair Ratio can be more tailored than a simple comparison with peers or the broad industry, because it adjusts for company specific characteristics rather than applying a single sector multiple to everyone.

With the current P/E of 26.6x close to the Fair Ratio of 26.9x, the stock looks priced at roughly a similar level to what this framework suggests.

Result: ABOUT RIGHT

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Philip Morris International Narrative

Earlier it was mentioned that there is an even better way to understand valuation, and on Simply Wall St this comes through Narratives. These let you set out your story for Philip Morris International by linking your view on its smoke free shift, regulation and margins to a concrete forecast for revenue, earnings and P/E. You can then compare the resulting fair value with today’s price on the Community page, where millions of investors share and update their Narratives as new news or earnings arrive. One investor might align with a more optimistic Philip Morris International view that anchors around a fair value of about US$210, while another might sit closer to a more cautious Narrative near US$153. You can see both, test your own assumptions and decide how the stock fits your portfolio.

For Philip Morris International, however, we will make it really easy for you with previews of two leading Philip Morris International Narratives:

Fair value in this bullish narrative: US$192.60 per share

Current price vs this fair value: the stock is about 1.96% above this level

Revenue growth used in this narrative: 6.52% a year

- Analysts in this camp see smoke free products, digital sales channels and broader geographic reach supporting revenue, margins and cash generation over time.

- The narrative is based on higher profit margins and a 24.6x P/E in 2029, with earnings modeled at US$15.4b and EPS of US$9.95.

- Key watchpoints include the structural decline in cigarettes, illicit trade, regulation, currency swings and the pace of smoke free adoption.

Fair value in this bearish narrative: US$170.00 per share

Current price vs this fair value: the stock is about 10.64% above this level

Revenue growth used in this narrative: 5.72% a year

- The cautious view stresses public health pressure, tighter rules, ESG driven divestment and cigarette volume declines as ongoing headwinds.

- It assumes earnings of US$14.4b and EPS of US$9.33 by 2028, with a lower 20.6x P/E and a higher cost of capital weighing on valuation.

- Risks to this downside case include stronger than expected demand for smoke free products, successful expansion into new markets and supportive regulation for reduced risk offerings.

If you want to go beyond these snapshots and weigh the trade off between upside and risk in more detail, you can review the full set of community views on valuation, growth and regulatory exposure for Philip Morris International using To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Philip Morris International on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Philip Morris International? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.