Is It Too Late To Consider Sanmina (SANM) After Its 102% One Year Surge?

Sanmina Corporation SANM | 0.00 |

- If you are wondering whether Sanmina's current share price offers value or signals that you may be late to the story, it helps to step back and look at what the recent returns are really telling you.

- The stock recently closed at US$154.47, with returns of 17.2% over 7 days, 23.4% over 30 days, a 3.0% decline year to date, and 101.8% over the past year, alongside 176.8% over 3 years and 274.6% over 5 years.

- Recent price moves sit against a backdrop of ongoing investor interest in electronics manufacturing services and broader conversations about where value and risk sit in this part of the market. For a stock with this kind of long term return profile, it is understandable that some investors are now asking whether expectations are running ahead of fundamentals.

- Simply Wall St currently assigns Sanmina a valuation score of 1 out of 6. The next sections will walk through what that means across different valuation approaches and then finish with a way to judge value that goes beyond any single model.

Sanmina scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

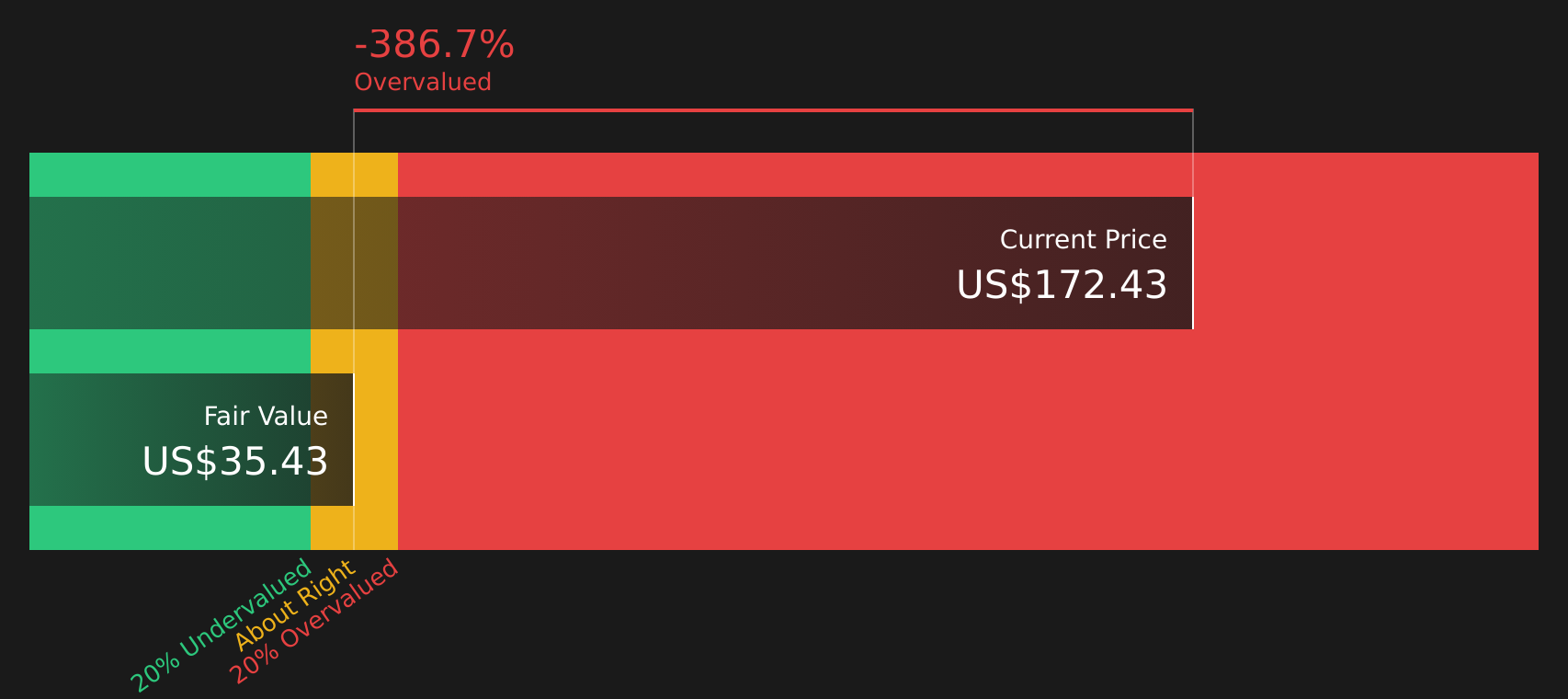

Approach 1: Sanmina Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a company could be worth by projecting its future cash flows and then discounting those amounts back to today using a required rate of return. It is essentially asking what those future dollars are worth in today's terms.

For Sanmina, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flows available to shareholders. The latest twelve month free cash flow is about $552.7 million. Analyst estimates and extrapolations point to projected free cash flow of around $258.4 million in 2035, with a detailed path of annual projections between now and then built into the model.

When all these projected cash flows are discounted back to today, the DCF model arrives at an estimated intrinsic value of about $66.96 per share. Compared with the recent share price of US$154.47, this implies the stock is 130.7% overvalued according to this specific set of assumptions.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Sanmina may be overvalued by 130.7%. Discover 57 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Sanmina Price vs Earnings

For a profitable company, the P/E ratio is often a useful shorthand because it tells you how many dollars you are paying for each dollar of current earnings. It is a quick way to line up price against the earnings power that is already in place.

What counts as a “fair” P/E usually reflects what investors think about a company’s growth prospects and risk profile. Higher expected growth or lower perceived risk can support a higher P/E, while slower expected growth or higher risk can justify a lower one.

Sanmina currently trades on a P/E of 36.65x. That sits above the Electronic industry average P/E of about 31.99x and below a peer group average of 77.48x. Simply Wall St also calculates a proprietary “Fair Ratio” of 32.86x for Sanmina. This Fair Ratio is designed to be more tailored than a simple peer or industry comparison because it blends factors such as earnings growth, profit margins, industry, market cap and key risks into a single reference multiple.

Comparing the current P/E of 36.65x with the Fair Ratio of 32.86x suggests Sanmina is trading above that reference level, so on this metric the stock screens as overvalued.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Upgrade Your Decision Making: Choose your Sanmina Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives are Simply Wall St’s way of letting you attach a clear story to the numbers by linking your view of Sanmina’s business to a forecast for revenue, earnings and margins, then through to a Fair Value that you can compare with today’s share price. All of this happens inside the Community page, where Narratives are refreshed automatically when new earnings or news arrive. One investor might back a higher Fair Value around US$200 based on expectations for AI and energy driven growth, while another leans toward US$135 because they focus more on customer concentration and margin risk. Both can see in one place how their story translates into numbers and what that means for their own investment decisions.

For Sanmina however, here are previews of two leading Sanmina Narratives:

Fair value: US$168.75

Implied mispricing versus last close: 8.5% discount to this fair value

Revenue growth assumption: 27.7%

- Analysts cite recent acquisitions, including ZT Systems, along with automation and higher value manufacturing as key drivers of future revenue and earnings.

- They note that ongoing investments, a solid balance sheet and buybacks are expected to support earnings per share over time, even with more measured margin assumptions.

- Main watchpoints include customer concentration, integration and supply chain risks, and the possibility that large capital projects may not deliver the expected returns.

Fair value: US$145.00

Implied mispricing versus last close: 6.5% premium to this fair value

Revenue growth assumption: 35.3%

- This narrative focuses on Sanmina's significant exposure to a small number of large cloud and AI data center customers and the risk that order timing or program ramps could affect earnings.

- It highlights that margin improvement depends on a shift toward higher margin programs while several end markets such as automotive and transportation are currently described as soft.

- It also notes sizeable capital spending and new facilities, where slower than expected volume or customer qualifications could weigh on free cash flow and limit earnings progress.

If you want to go beyond the previews and see each storyline, the assumptions behind it and how other investors are interpreting the same numbers, See what the community is saying about Sanmina.

Do you think there's more to the story for Sanmina? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.