Is It Too Late To Consider Seagate Technology Holdings (STX) After A 328% One-Year Rally?

Seagate Technology Holdings PLC STX | 513.28 522.00 | +2.02% +1.70% Pre |

- If you are wondering whether Seagate Technology Holdings is still reasonably priced after its strong run, this article will walk through what the numbers say about the stock's value.

- At a last close of US$425.99, the stock has seen a 36.4% gain over the past 30 days, alongside a 48.1% return year to date and a very large 1 year return of 328.0%. These changes can influence how investors think about both upside and risk.

- These moves have come as investors react to ongoing developments around data storage demand and sentiment toward technology hardware companies in general, with Seagate often treated as a proxy for that theme. This article is not tied to a specific event; instead, it is intended to give you a standing reference point whenever price shifts catch your eye again.

- On our framework, Seagate holds a valuation score of 3 out of 6. This means some checks suggest the shares may be undervalued while others do not. We will walk through those standard valuation approaches next, then finish with a more rounded way to think about value.

Approach 1: Seagate Technology Holdings Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes estimates of the cash a business could generate in the future and discounts those amounts back to what they might be worth in today’s dollars.

For Seagate Technology Holdings, the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow is about $1.68b. Analysts and internal estimates project free cash flow rising to $6.40b by 2030, with a detailed path laid out each year between 2026 and 2035. Early years are based on analyst inputs, while later years are extrapolated by Simply Wall St using the earlier growth pattern.

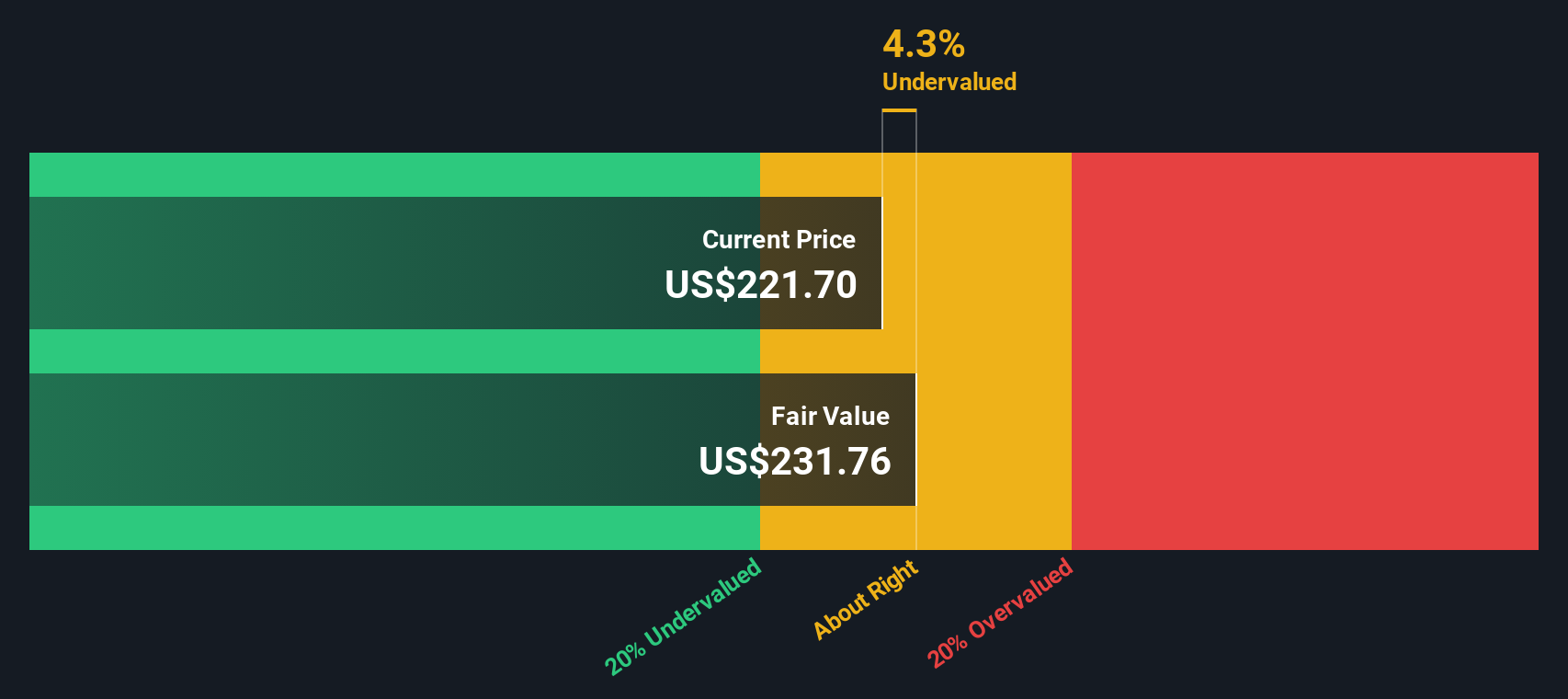

When all those future cash flows are discounted back and added up, the model points to an estimated intrinsic value of about $613.27 per share. Compared to the recent share price of $425.99, that implies the stock is 30.5% below this DCF estimate. This suggests the market price is meaningfully lower than the model’s central valuation.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Seagate Technology Holdings is undervalued by 30.5%. Track this in your watchlist or portfolio, or discover 55 more high quality undervalued stocks.

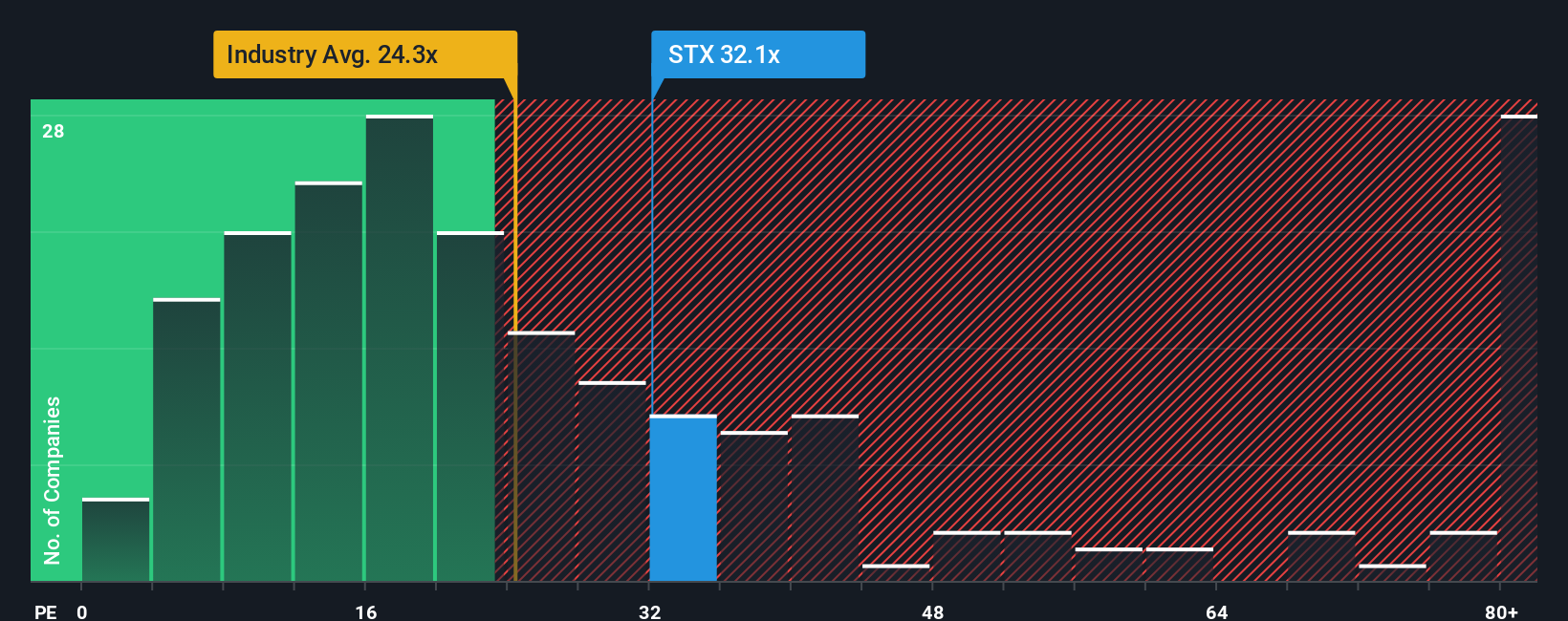

Approach 2: Seagate Technology Holdings Price vs Earnings

For profitable companies, the P/E ratio is a useful way to think about what you are paying for each dollar of current earnings. It ties the share price directly to the business’s ability to generate profit, which many investors naturally focus on when comparing opportunities.

What counts as a “normal” P/E depends a lot on expectations and risk. Higher growth usually supports a higher multiple, while more uncertainty or weaker profitability tends to push a fair P/E lower.

Seagate Technology Holdings currently trades on a P/E of 47.16x. That is higher than the broader Tech industry average of 22.19x, but below the peer group average of 60.85x. Simply Wall St’s Fair Ratio for Seagate is 45.26x, which is the P/E it estimates would be reasonable given factors such as earnings growth, industry, profit margin, market cap and company specific risks.

This Fair Ratio is more tailored than a simple comparison with peers or the industry, because it adjusts for Seagate’s own characteristics rather than assuming all Tech stocks deserve the same multiple.

Compared with this Fair Ratio, Seagate’s actual P/E of 47.16x is slightly higher, which points to the shares being a bit overvalued on this measure.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 23 top founder-led companies.

Upgrade Your Decision Making: Choose your Seagate Technology Holdings Narrative

Earlier we mentioned that there is an even better way to think about value. On Simply Wall St's Community page you can use Narratives, where you write the story you believe about Seagate Technology Holdings, link that story to your own forecast for revenue, earnings and margins, and the platform converts it into a Fair Value that you can compare with the current price. This can help you decide if, when and at what price you might want to buy or sell. That Fair Value then updates automatically as new news or earnings arrive. One investor might build a very optimistic Seagate view in line with a Fair Value of US$505 per share, while another might lean toward a cautious view closer to US$115.79. Both are simply different, clearly quantified stories behind the same stock.

For Seagate Technology Holdings, we will make it really easy for you with previews of two leading Seagate Technology Holdings Narratives:

Fair value: US$505.00 per share

Implied pricing gap vs last close: about 15.7% below this narrative fair value

Revenue growth assumption: 31.56% a year

- Expects faster adoption of high capacity HAMR based drives, tighter supply, and AI related data growth to support higher revenue, margins and cash flow than many current models assume.

- Sees restructuring, automation and vertical integration lifting free cash flow conversion and giving the company more room for debt reduction and capital returns.

- Flags real risks around a faster shift to flash storage, customer consolidation, regulation and potential demand shocks, which could pressure margins and earnings if they play out differently.

Fair value: about US$297.09 per share

Implied pricing gap vs last close: about 43.4% above this narrative fair value

Revenue growth assumption: 13.75% a year

- Assumes solid revenue growth from AI driven data center demand and HAMR adoption, with room for higher margins as pricing and manufacturing shifts feed through.

- Ties the fair value to expectations for stronger HDD pricing power and disciplined capacity additions, but with more moderate growth and valuation multiples than the bullish view.

- Highlights competition from SSDs, policy and tax changes, debt and cycle risk as factors that could cap valuation or lead to multiple compression if conditions change.

If you want to go beyond the numbers and see the full reasoning, you can step into these storylines yourself, compare them with your own expectations, and decide which one, if either, fits how you see Seagate over the next few years. Curious how numbers become stories that shape markets? Explore Community Narratives

Do you think there's more to the story for Seagate Technology Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.