Is It Too Late To Consider Seagate Technology Holdings (STX) After Its Recent Surge In Price

Seagate Technology Holdings PLC STX | 0.00 |

- Wondering if Seagate Technology Holdings at around US$751 a share is still offering value, or if most of the opportunity has already played out.

- The stock has been volatile recently, falling around 8.1% over the past week, after very strong returns of 39.2% over 30 days and 161.2% year to date, with a very large gain over the last year and an increase of about 12x over three years.

- Those sharp moves have come alongside persistent attention on Seagate as a key storage supplier for data center and AI related demand. Investors are closely watching how its positioning in that ecosystem could affect long term cash flows. Broader enthusiasm around AI infrastructure and data growth has helped put the stock in focus for both momentum traders and valuation focused investors.

- Simply Wall St currently gives Seagate a valuation score of 3/6. The rest of this article compares different valuation approaches on the stock and then finishes with a broader framework that can help you think about value beyond just the headline metrics.

Approach 1: Seagate Technology Holdings Discounted Cash Flow (DCF) Analysis

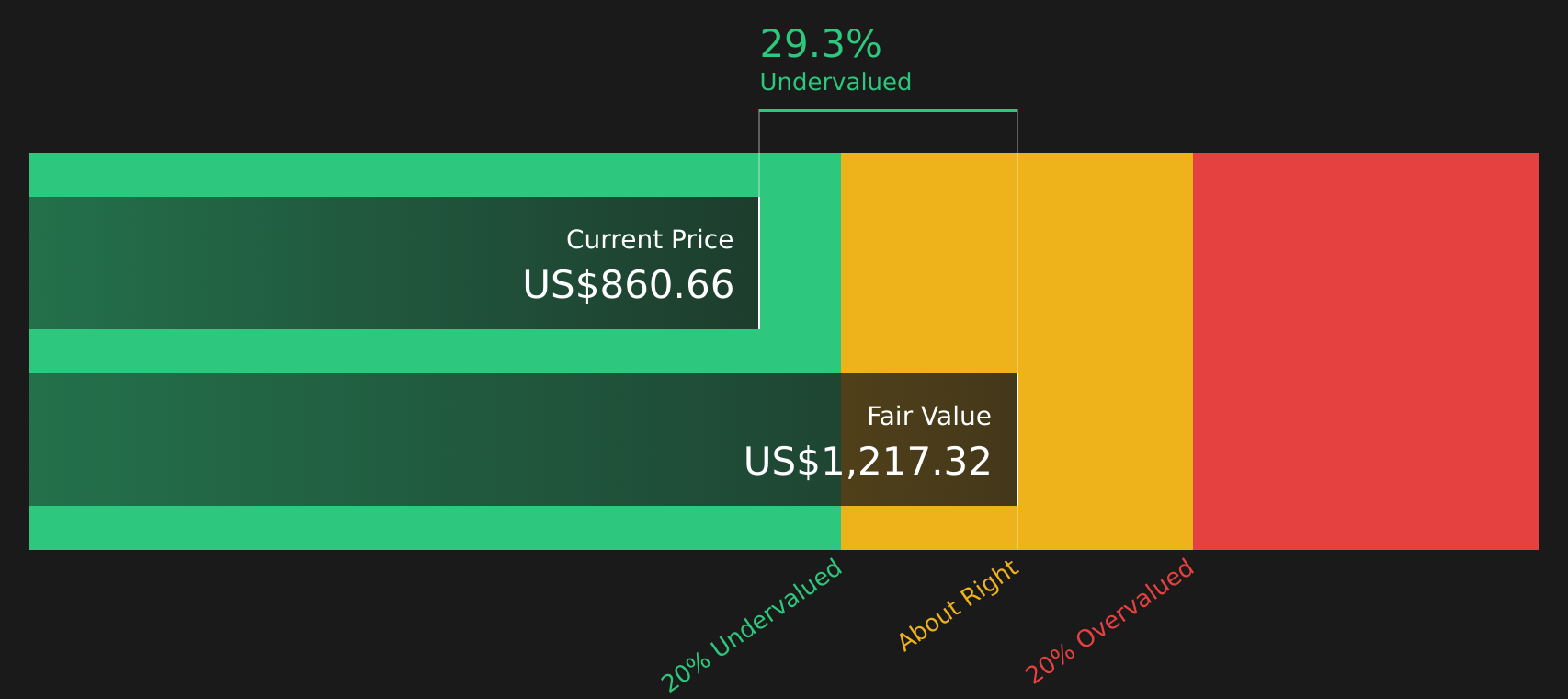

A Discounted Cash Flow model estimates what a stock could be worth by projecting future cash flows and discounting them back to today. For Seagate Technology Holdings, the model uses a 2 stage Free Cash Flow to Equity approach, anchored on last twelve months free cash flow of about $2.47b.

Analysts and internal estimates project Seagate’s free cash flow reaching $11.72b in 2030, with a detailed path laid out from 2026 to 2035. These projections, expressed in $, are then discounted each year, with the 2030 cash flow, for example, discounted to about $7.90b. The discounted values across the forecast period are summed to arrive at an estimated intrinsic value of $1,314.60 per share.

Compared with the current share price of about $751, the DCF output implies the stock is 42.9% below this intrinsic estimate, which indicates that Seagate is trading at a sizeable discount based on these cash flow assumptions.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Seagate Technology Holdings is undervalued by 42.9%. Track this in your watchlist or portfolio, or discover 51 more high quality undervalued stocks.

Approach 2: Seagate Technology Holdings Price vs Earnings

For profitable companies, the P/E ratio is a useful way to think about value because it links what you pay for the stock to the earnings the business generates today. Higher expected growth and lower perceived risk usually justify a higher “normal” or “fair” P/E, while slower growth or higher risk tend to point to a lower one.

Seagate Technology Holdings currently trades on a P/E of 70.82x, compared with a Tech industry average of 21.97x and a peer average of 58.71x. Simply Wall St’s Fair Ratio for Seagate is 79.12x. This Fair Ratio is a proprietary estimate of what a reasonable P/E could be for the company, based on factors such as its earnings growth profile, profit margins, industry, market cap and specific risks.

Because the Fair Ratio incorporates these company specific drivers, it can be more informative than a simple comparison to peers or the broad industry, which may have very different growth and risk characteristics. On this basis, Seagate’s current P/E of 70.82x is below the Fair Ratio of 79.12x, which suggests the stock is trading at a discount to this earnings based valuation framework.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Seagate Technology Holdings Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives bring this to life by letting you attach a clear story about Seagate Technology Holdings to your numbers, link that story to a forecast for revenue, earnings and margins, and then see a Fair Value that you can compare with the current price, all inside the Simply Wall St Community page where millions of investors share their views.

For example, one Seagate Narrative on the bullish end ties a Fair Value of about US$1,096.35 to assumptions of faster revenue growth, much higher profit margins at 55.78% and earnings of US$16.0b. In contrast, a more cautious Seagate Narrative anchors a Fair Value of about US$375.00 to revenue growth of 13.50%, profit margins at 26.24% and earnings of US$3.9b. As news or earnings arrive, these Narratives refresh automatically so you can see how updated information shifts Fair Value and whether, for your chosen story, the stock looks closer to a buy, a hold or a sell decision point.

For Seagate Technology Holdings however we will make it really easy for you with previews of two leading Seagate Technology Holdings Narratives:

Fair Value: US$770.43 per share

Gap to this Fair Value: currently trading about 2.5% below that figure

Implied revenue growth used in this story: 30.04% a year

- Assumes AI and cloud demand for high capacity storage, plus HAMR Mozaic drives, support strong revenue growth and a much higher profit margin profile over time.

- Treats build to order contracts and agreements with large cloud and hyperscale customers as key supports for earnings visibility and cash flow.

- Views debt, trade policy and competing storage technologies as real risks, but still sees the current price as close to what analysts consider a fair reflection of those growth and margin assumptions.

Fair Value: US$375.00 per share

Gap to this Fair Value: currently trading about 100.3% above that figure

Implied revenue growth used in this story: 13.50% a year

- Frames Seagate as heavily exposed to traditional HDDs at a time when customers are expected to lean harder into energy efficient storage like SSDs, which could cap long run growth.

- Assumes that higher R&D and manufacturing spending on next generation HDDs weighs on profitability if volumes or pricing do not keep pace.

- Argues that, even with earnings growth, the current share price sits well above what more cautious analysts view as a reasonable multiple on 2029 earnings.

Once you are clear on which story feels closer to your own expectations for AI storage demand, HDD versus SSD adoption and long term margins, you can use that narrative as the lens to interpret the current Seagate share price.

Do you think there's more to the story for Seagate Technology Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.