Is It Too Late To Consider Viasat (VSAT) After Its 7x One Year Share Price Surge

Viasat VSAT | 0.00 |

- This article looks at whether Viasat, at around US$72.61, may still offer value or whether its current price already reflects the full story, by walking through key signals investors are watching on valuation.

- The stock has been volatile recently, with the price falling 10.8% over the past week, rising 11.5% over the past month, and recording a large 1-year return of about 7x, alongside a 93.0% gain year to date.

- Recent headlines have focused on Viasat's role in satellite connectivity and communications services, as well as investor reactions to changing expectations around its growth profile and capital needs. This mix of enthusiasm and concern helps explain the sharp share price swings seen over shorter time frames.

- On Simply Wall St's valuation checks, Viasat scores a 5 out of 6. Next, this article will look at how different valuation approaches interpret that score, then outline a way to think about value that goes beyond any single model.

Approach 1: Viasat Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes projected future cash flows, then discounts them back to today to estimate what the company could be worth right now. It is essentially asking what future cash generation is worth in today’s dollars.

For Viasat, the latest twelve month Free Cash Flow is about $360.3 million. Simply Wall St applies a 2 Stage Free Cash Flow to Equity model that uses analyst estimates for the early years, then extrapolates further cash flows out to 2035. Within this framework, projected Free Cash Flow in 2028 is $466.5 million, with later years also estimated and discounted to today.

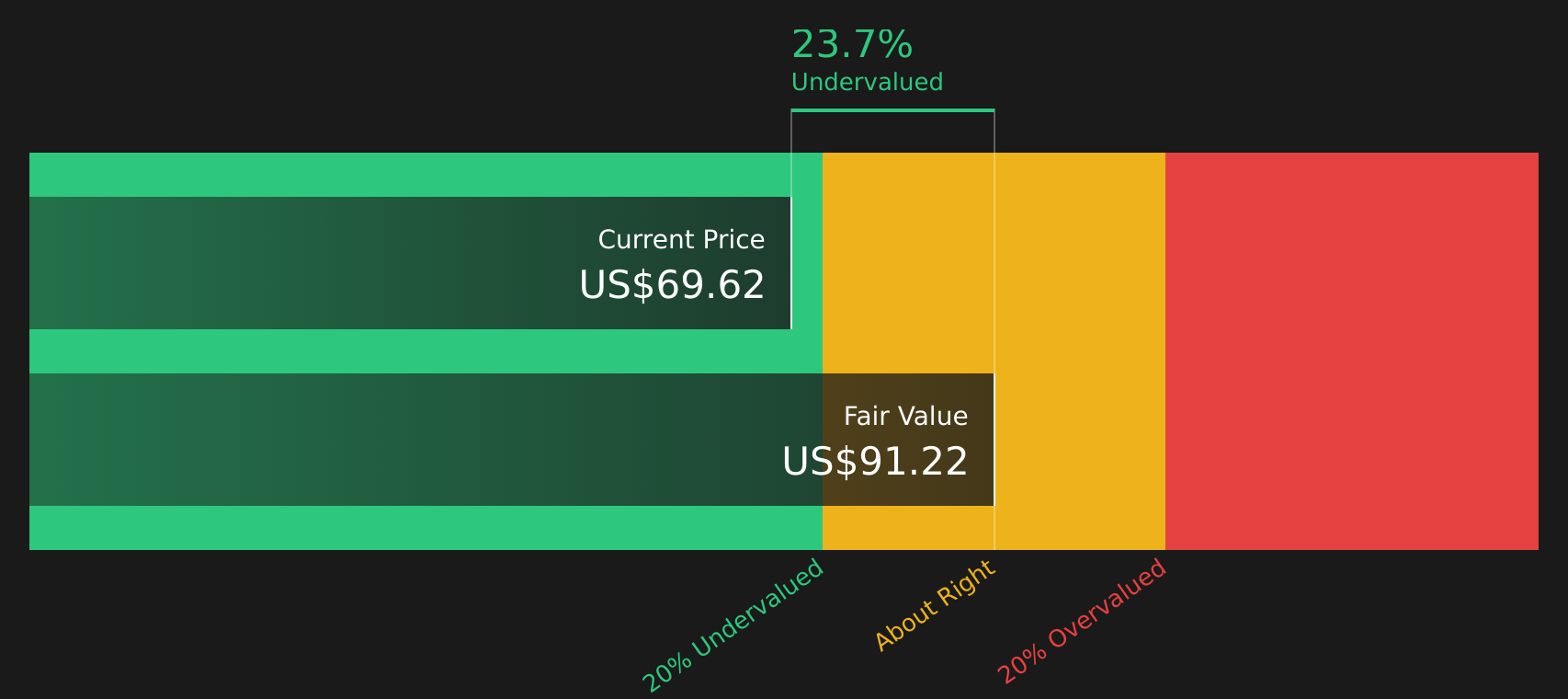

Adding up those discounted cash flows produces an estimated intrinsic value of $91.52 per share. Against a current share price of about $72.61, the model implies the stock trades at roughly a 20.7% discount to this intrinsic value. This suggests that Viasat appears undervalued on this DCF view.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Viasat is undervalued by 20.7%. Track this in your watchlist or portfolio, or discover 46 more high quality undervalued stocks.

Approach 2: Viasat Price vs Sales

For companies where profitability is limited or earnings are volatile, a Price to Sales, or P/S, multiple can be a more practical gauge than P/E because it anchors the valuation to revenue rather than earnings that may swing from profits to losses.

In general, higher growth expectations and lower perceived risk support a higher “normal” P/S ratio, while slower expected growth or higher risk usually point to a lower multiple. That is why comparing a stock’s P/S to context is important rather than treating any single number as good or bad.

Viasat’s current P/S ratio is 2.14x, compared with the Communications industry average of 2.64x and a broader peer group average of 15.05x. Simply Wall St’s “Fair Ratio” for Viasat is 2.97x. This Fair Ratio is a proprietary estimate of the multiple that could be reasonable given factors such as Viasat’s growth profile, profit margins, risks, industry and market cap.

Because it incorporates those company specific drivers, the Fair Ratio can be more informative than a simple comparison against peers or the industry average. With Viasat trading at 2.14x versus a Fair Ratio of 2.97x, the stock currently appears undervalued on this P/S approach.

Result: UNDERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Viasat Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives give you a clear story behind the numbers by linking your view on Viasat, such as how its satellite program, spectrum position or competition will play out, to a specific forecast for revenue, earnings and margins, then into a Fair Value that you can compare to today’s share price.

On Simply Wall St’s Community page, Narratives are easy to use and update automatically when fresh information arrives, such as new price targets, contract wins or earnings results, so the Fair Value in each Narrative keeps reflecting the latest data.

For Viasat, one investor might build a cautious Narrative that aligns with a Fair Value near US$48.00, focusing on capital intensity, competition from LEO satellites and regulatory risks. Another might choose a more optimistic Narrative closer to US$92.64 that leans on views about the company’s spectrum assets, ViaSat 3 progress and potential contract opportunities. By comparing each Fair Value to the current price, you can decide which story, if any, fits your own expectations.

For Viasat however, we will make it really easy for you with previews of two leading Viasat Narratives:

Fair Value: US$92.64 per share

Implied discount to this narrative: about 21.3% below its fair value

Revenue growth used in this view: 3.3% a year

- Expects Viasat's MSS spectrum position and ViaSat 3 rollout to open up new high value markets across mobility, government and global connectivity.

- Assumes a shift toward lower capital intensity and stronger free cash flow as shared infrastructure and multi orbit models take hold.

- Builds in higher future earnings and margins, with a Fair Value of US$92.64 sitting above the current consensus range.

Fair Value: US$51.14 per share

Implied premium to this narrative: about 42.0% above its fair value

Revenue growth used in this view: 3.3% a year

- Assumes that high capital expenditure, leverage and execution risks around ViaSat 3 and Inmarsat integration will keep pressure on free cash flow.

- Highlights subscriber declines, rising competition from LEO constellations and regulatory costs as ongoing headwinds for margins and growth.

- Anchors on a consensus Fair Value of US$51.14 that is below the current share price, implying limited upside if analyst assumptions prove accurate.

If you want to go beyond these previews and see how other investors are connecting Viasat's satellites, spectrum and balance sheet to different Fair Values, you can step through the full range of community views in one place using See what the community is saying about Viasat.

Do you think there's more to the story for Viasat? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.