Is It Too Late to Consider W. P. Carey After 27% Share Price Surge?

W. P. Carey Inc. WPC | 70.25 | +1.24% |

- Wondering if W. P. Carey is still a bargain or if its recent run means you might be late to the party? You're not alone. Knowing whether to buy, hold, or move on all starts with nailing down what the stock is really worth.

- After a solid 27.2% gain over the last year and a jump of 23.2% year-to-date, W. P. Carey's stock clearly hasn't gone unnoticed, with buyers and risk-takers eyeing the momentum.

- Some of the recent uptick can be traced to sector-wide moves in commercial real estate and positive headlines about W. P. Carey's portfolio adjustments, including asset sales aimed at strengthening its balance sheet. Major financial outlets have also highlighted renewed investor enthusiasm for high-yield REITs like W. P. Carey as market uncertainty lingers.

- But is all of this already priced in? W. P. Carey currently scores a 3 out of 6 on our undervaluation checks, so it's worth taking a closer look at how traditional valuation methods stack up. Stick around to find out what method might actually reveal the best opportunities at the end of this article.

Approach 1: W. P. Carey Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates what a company is worth by forecasting its future cash flows and then discounting those back to today’s dollars. For W. P. Carey, this approach uses adjusted funds from operations to provide a clearer picture of underlying cash generation.

Currently, W. P. Carey generates Free Cash Flow of $1.04 billion. Analysts expect this to grow, and by 2028 projections show Free Cash Flow reaching $1.41 billion. Only five years of forward estimates are compiled from analyst sources. After that, Simply Wall St extrapolates further by forecasting steady growth out to 2035.

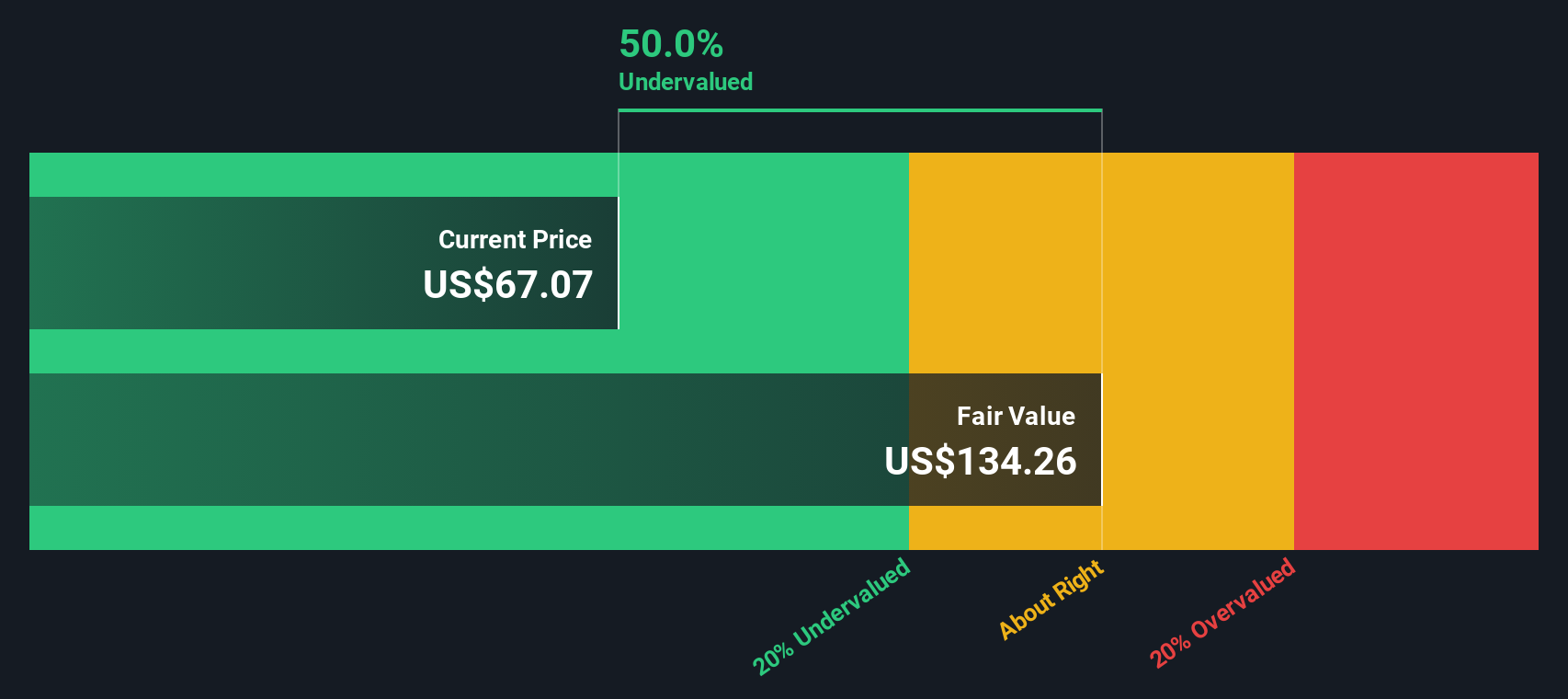

Taking all these future cash flows and discounting them to reflect their present value, the DCF model estimates W. P. Carey’s intrinsic value at $158.08 per share. That is a 57.7% discount to where the shares currently trade, suggesting the stock is significantly undervalued based on these assumptions.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests W. P. Carey is undervalued by 57.7%. Track this in your watchlist or portfolio, or discover 865 more undervalued stocks based on cash flows.

Approach 2: W. P. Carey Price vs Earnings

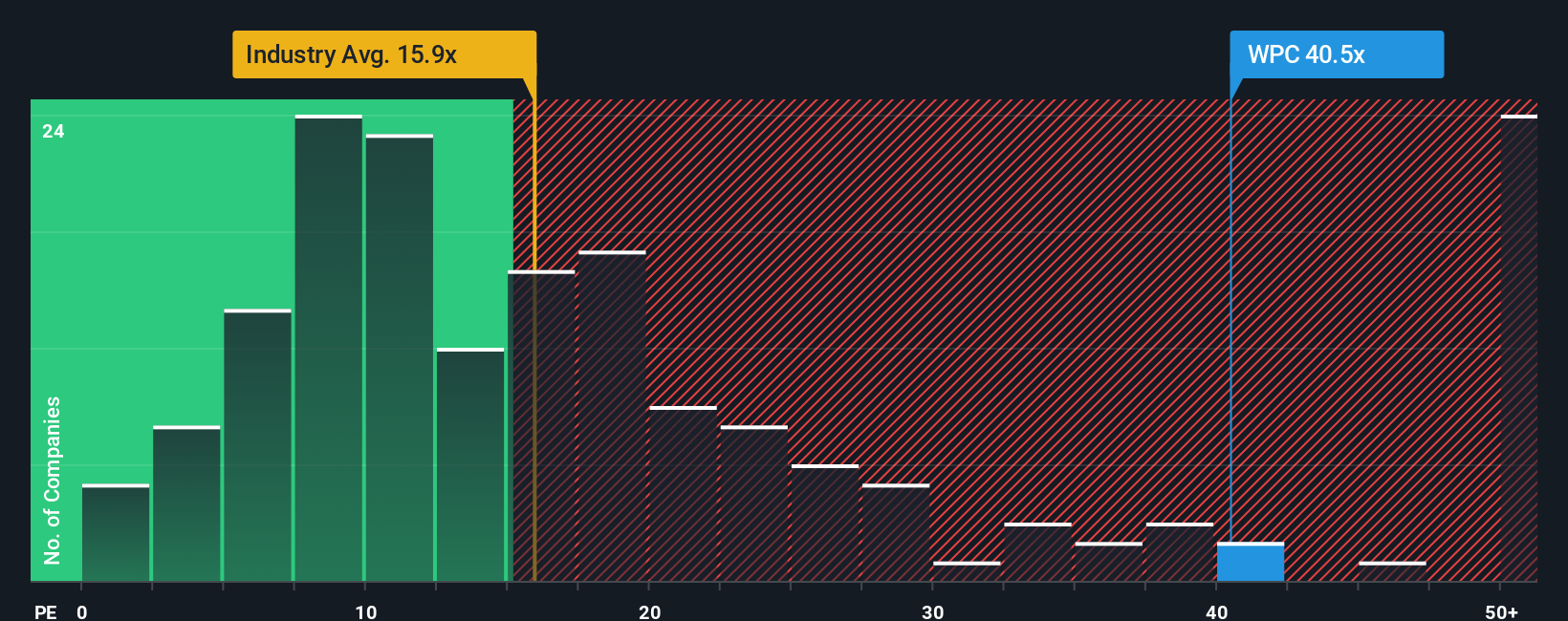

The Price-to-Earnings (PE) ratio is a classic valuation tool for analyzing profitable companies like W. P. Carey. It gives investors a quick read on how much they are paying for every dollar of earnings, offering a direct link between price, profits, and market sentiment.

Growth prospects and company risk play a big role in what counts as a "normal" PE ratio. Higher growth or lower risk can justify a higher PE, while uncertainties or slower expected growth tend to bring it down. This is why context is key when using the PE ratio for a stock like W. P. Carey.

At the moment, W. P. Carey trades at a PE ratio of 40.14x. That is notably higher than the industry average of 15.11x and also above the peer group average of 28.43x. By comparison, Simply Wall St’s proprietary "Fair Ratio" for W. P. Carey, which factors in its growth outlook, risk profile, profit margins, market cap, and position in the REITs sector, lands at 40.40x.

The Fair Ratio does a better job at capturing a company’s full picture than simple comparisons to industry or peers. It tailors the valuation to W. P. Carey’s unique qualities and outlook, so investors can spot more realistic value, not just market sentiment.

With the actual PE ratio just a hair below the Fair Ratio, W. P. Carey's valuation is right in line with what its fundamentals would suggest.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1402 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your W. P. Carey Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is a simple, easy-to-use framework that lets you articulate your perspective on a company by connecting your story and assumptions about W. P. Carey's future (like revenue, earnings, and profit margins) directly to a forecast and a calculated fair value. Narratives live at the heart of Simply Wall St’s Community page, allowing you to quickly build a personal valuation and see how your outlook compares to millions of other investors. Because Narratives update dynamically whenever the latest news or earnings drop, you can easily track whether your investment thesis still stacks up as events unfold. For example, one investor’s Narrative for W. P. Carey might see strong rent growth and international expansion supporting a price target as high as $75.00, while another highlights riskier tenant exposure and expects a value closer to $60.00. By comparing Narratives, you gain richer insight and can confidently decide when to buy, hold, or move on, knowing exactly how the numbers line up with the story you believe.

Do you think there's more to the story for W. P. Carey? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.