Is It Too Late To Consider Watts Water Technologies (WTS) After 44% One-Year Gain?

Watts Water Technologies, Inc. Class A WTS | 0.00 |

- Investors may be wondering if Watts Water Technologies at around US$300 a share still offers value, or if most of the opportunity is already reflected in the price.

- The stock last closed at US$300.16, with returns of 3.4% over 30 days, 7.7% year to date, and 43.6% over 1 year, which may signal that the market view on the company has shifted compared to the past.

- Recent interest in water infrastructure, regulation, and efficiency solutions has kept attention on companies that supply plumbing, heating, and water quality products. Watts Water Technologies, with its focus on these areas, has been part of that broader conversation around how capital is being allocated to essential systems.

- Even with a value score of 2 out of 6, which suggests only a couple of traditional checks point to undervaluation, different valuation approaches can lead to very different conclusions. The end of this article will walk through a way of tying those methods together into a clearer picture.

Watts Water Technologies scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Watts Water Technologies Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model projects a company’s future cash flows and then discounts those projections back to today’s dollars to estimate what the business might be worth right now.

For Watts Water Technologies, the model uses last twelve months free cash flow of about $362 million and a 2 Stage Free Cash Flow to Equity approach. Analysts provide specific free cash flow estimates out to 2029, with Simply Wall St extrapolating further years. By 2035, the projection used in the model is $714 million in free cash flow, all stated in US$ and discounted back to today using the selected cost of equity assumptions.

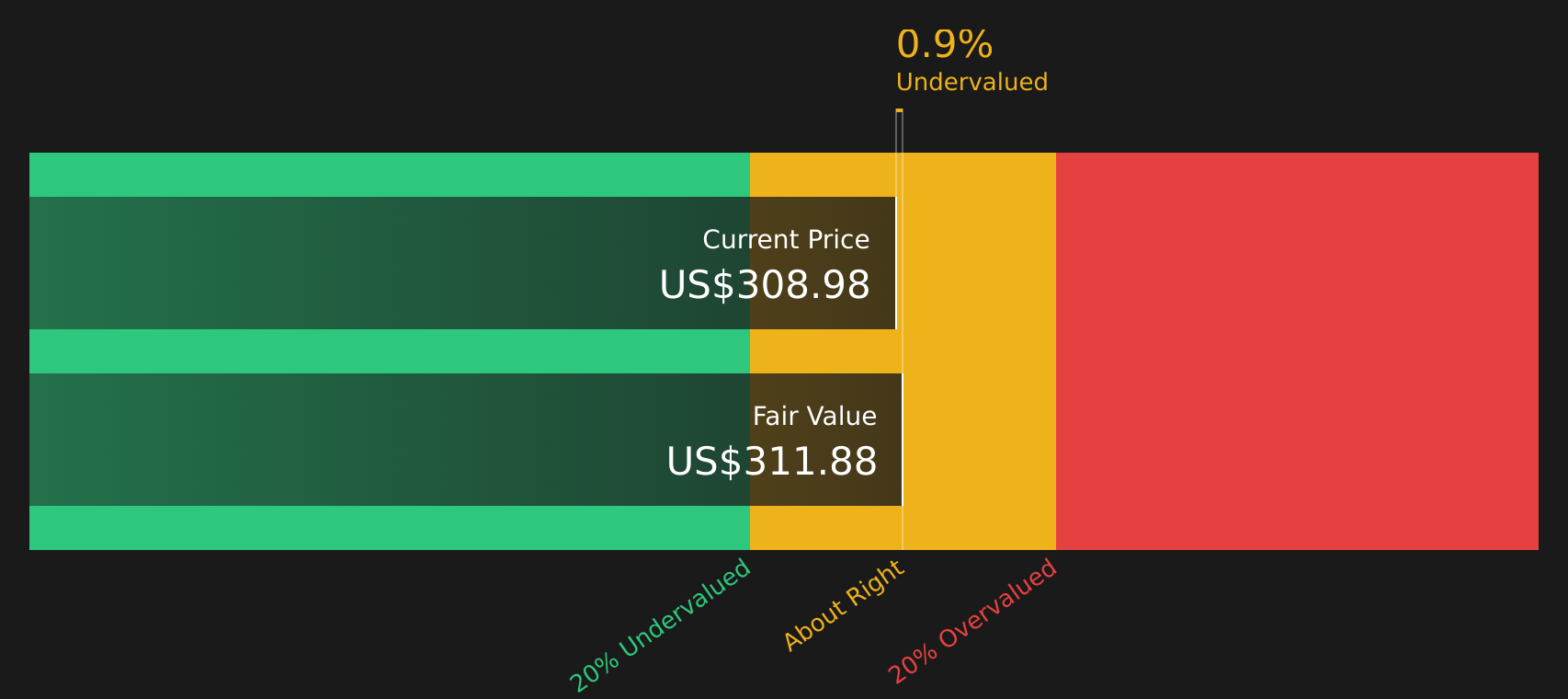

Pulling all those discounted cash flows together, the DCF output suggests an intrinsic value of about $309.20 per share, compared with a recent share price of around $300.16. That implies the stock is roughly 2.9% below the model’s estimate of fair value, which sits within a normal margin of error for this kind of analysis.

Result: ABOUT RIGHT

Watts Water Technologies is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: Watts Water Technologies Price vs Earnings

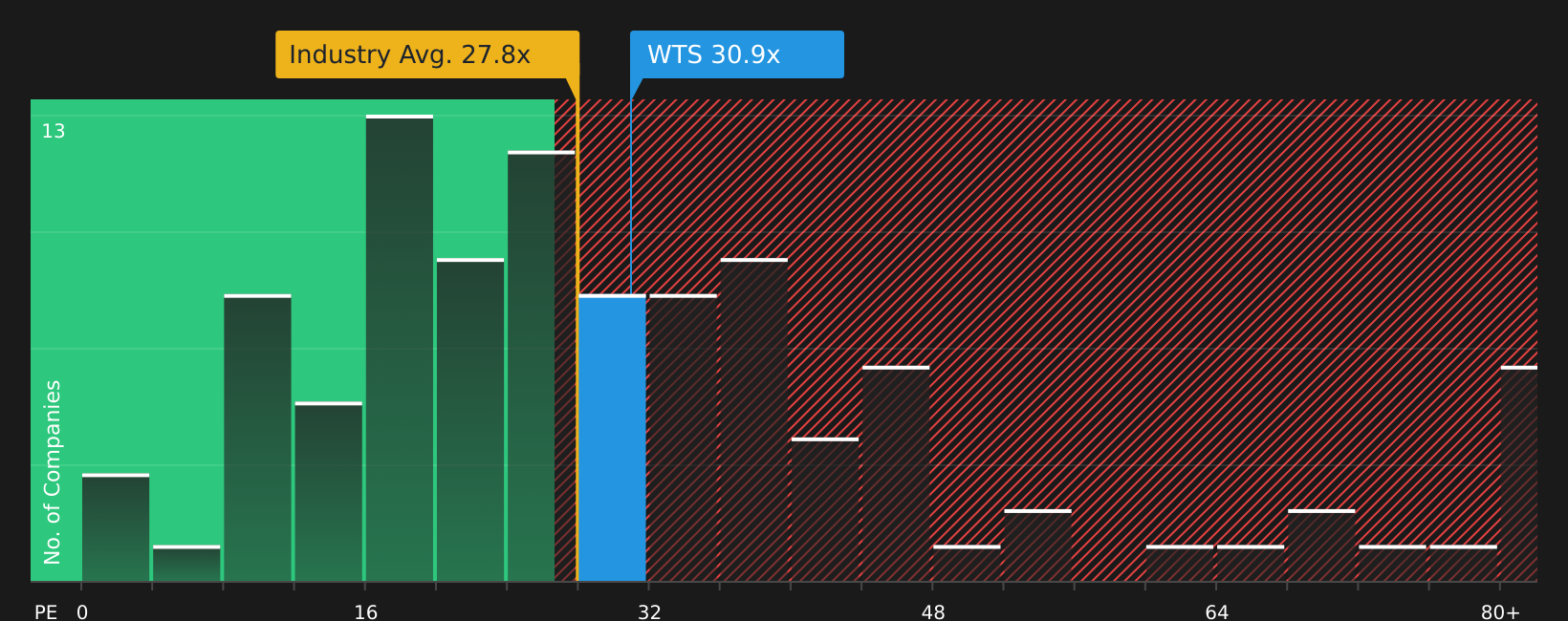

For a profitable business like Watts Water Technologies, the P/E ratio is a useful shorthand for how much you are paying for each dollar of earnings. It tends to sit higher when investors expect stronger growth or see lower risk, and lower when expectations are more muted or risks are higher.

Watts currently trades on a P/E of 29.4x. That is above the Machinery industry average P/E of about 27.8x, yet below the peer group average of 38.2x. To add more context, Simply Wall St also calculates a “Fair Ratio”, which is the P/E level it would expect for Watts given factors such as earnings characteristics, profit margins, industry, market cap, and risk profile. For Watts, that Fair Ratio is 22.4x.

This Fair Ratio is designed to be more tailored than a simple comparison with peers or the industry, because it ties the multiple back to company specific fundamentals rather than broad group averages. Setting the current 29.4x P/E against the 22.4x Fair Ratio suggests the shares are trading above what this framework would flag as a more typical level.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Upgrade Your Decision Making: Choose your Watts Water Technologies Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives on Simply Wall St’s Community page let you attach a clear story about Watts Water Technologies to concrete numbers like your assumed fair value, revenue, earnings and margin forecasts. You can then compare that fair value with the current price to help decide whether to act. Each Narrative updates automatically when new news or earnings arrive. One investor might align with a more cautious view around a Fair Value of about US$279.87, while another leans toward a higher Fair Value near US$340. You can quickly see how those different stories and assumptions translate into very different views on what the shares are worth today.

For Watts Water Technologies however we'll make it really easy for you with previews of two leading Watts Water Technologies Narratives:

Fair value in this bullish narrative: about US$336.11 per share.

Current price vs this fair value: roughly 10.7% below the narrative fair value.

Revenue growth assumption: 6.8% a year.

- Focuses on growth in intelligent water management platforms like Nexa, along with regulation driven demand for efficiency and compliance solutions.

- Emphasizes investments in automation, supply chain resilience, and acquisition integration that are expected to support margins and earnings.

- Highlights analyst expectations for higher earnings, slightly stronger margins, and a P/E in the high 20s by 2029, with a consensus fair value close to US$336.

Fair value in this cautious narrative: about US$279.87 per share.

Current price vs this fair value: roughly 7.2% above the narrative fair value.

Revenue growth assumption: 7.0% a year.

- Flags reliance on mature Western markets, potential pressure from new water efficient technologies, and competition from lower cost and IoT focused peers.

- Points to higher regulatory and compliance costs and the risk that infrastructure spending can be lumpy, which could make earnings less predictable.

- Assumes similar earnings growth but a lower future P/E in the mid 20s, anchoring a fair value closer to US$280 and implying less room for valuation stretch.

If you want to go beyond the previews and see how other investors are framing Watts Water Technologies with their own assumptions and fair values, you can review the full set of community narratives and compare them to your own expectations. See what the community is saying about Watts Water Technologies

Do you think there's more to the story for Watts Water Technologies? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.