Is It Too Late To Reassess American Eagle Outfitters (AEO) After Its 92% One Year Surge?

American Eagle Outfitters, Inc. AEO | 0.00 |

- If you are trying to figure out whether American Eagle Outfitters is still good value after its recent run, you are not alone. This article is built to help you frame that question clearly.

- The stock trades at US$22.24, with returns of 92.5% over 1 year and 77.8% over 3 years. However, the 7 day, 30 day and year to date returns of 6.4%, 4.6% and 15.6% declines might make the recent performance feel a bit shaky.

- Recent headlines around American Eagle Outfitters have focused on its position in the US retail sector and how investors are reacting to changing expectations for the business and its peers. This context helps explain why the share price has seen strong gains over the past year while also experiencing some shorter term pullbacks.

- Our valuation work gives American Eagle Outfitters a score of 4 out of 6. Next, we will look at what different valuation methods say about that number and then finish by showing you an even more complete way to think about what the stock is worth.

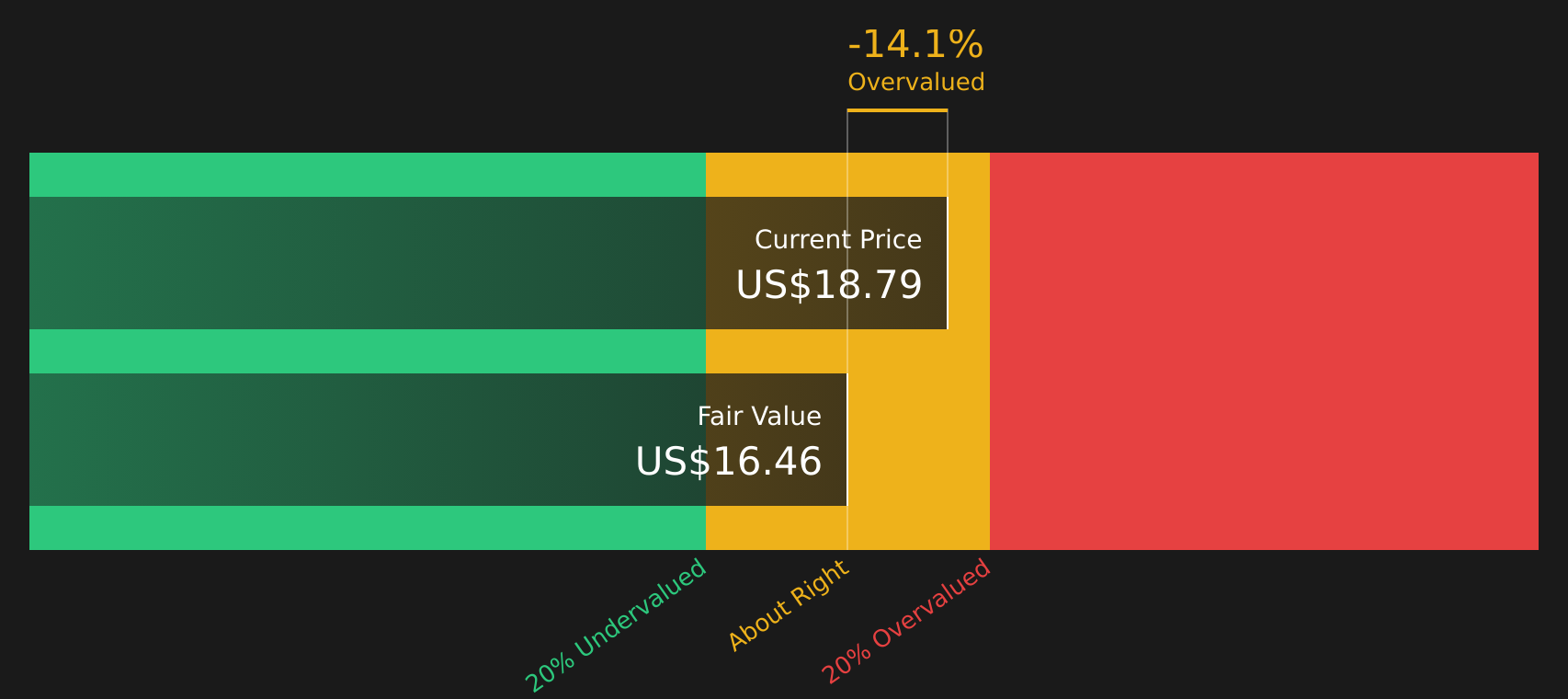

Approach 1: American Eagle Outfitters Discounted Cash Flow (DCF) Analysis

Approach 1: American Eagle Outfitters Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes the cash a business is expected to generate in the future and discounts those amounts back to what they are worth today, then sums them to estimate an intrinsic value per share.

For American Eagle Outfitters, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month Free Cash Flow is about $201.7 million, and analysts provide explicit forecasts out to 2028, where projected Free Cash Flow is $262.5 million. Beyond those analyst years, Simply Wall St extrapolates additional annual Free Cash Flow projections out to 2035, all kept in the same dollar terms.

When those projected cash flows are discounted back and combined with a terminal value, the DCF model arrives at an estimated intrinsic value of about $26.78 per share. Compared with the current share price of $22.24, this implies the stock is around 17.0% undervalued based on these assumptions.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests American Eagle Outfitters is undervalued by 17.0%. Track this in your watchlist or portfolio, or discover 49 more high quality undervalued stocks.

Approach 2: American Eagle Outfitters Price vs Earnings

For a profitable company like American Eagle Outfitters, the P/E ratio is a useful shorthand for what the market is currently willing to pay for each dollar of earnings. Higher P/E ratios often reflect higher market expectations or lower perceived risk, while lower P/E ratios can point to more muted expectations or higher perceived risk.

Growth forecasts and risk levels both influence what might be viewed as a “normal” or “fair” P/E range for a stock. American Eagle Outfitters currently trades on a P/E of 18.1x. That sits below the Specialty Retail industry average of about 20.1x and also below the peer average of 19.2x, suggesting the market is pricing the shares at a discount compared with many similar businesses.

Simply Wall St’s Fair Ratio for American Eagle Outfitters is 21.2x. This is a proprietary estimate of what the P/E could be given the company’s earnings growth profile, industry, profit margins, market capitalization and specific risk factors. Because it is tailored to the company’s fundamentals, the Fair Ratio can offer a more targeted reference point than a simple comparison with industry or peer averages. With the current P/E of 18.1x below the Fair Ratio of 21.2x, the shares screen as undervalued on this metric.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Upgrade Your Decision Making: Choose your American Eagle Outfitters Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. Narratives let you spell out your story for American Eagle Outfitters, link that story to specific assumptions for future revenue, earnings and margins, turn those into a Fair Value, and then compare that Fair Value to the current share price, all within Simply Wall St’s Community page. Narratives update automatically as new news or earnings arrive. For example, one investor might build a cautious American Eagle Outfitters view around a US$10.00 Fair Value, while another builds a more optimistic story that supports a Fair Value closer to US$25.78, giving you clear, side by side perspectives on when the stock looks expensive or cheap based on the story you actually believe.

For American Eagle Outfitters however, we will make it really easy for you with previews of two leading American Eagle Outfitters Narratives:

Each one takes the same business and valuation building blocks you have seen so far and turns them into a clear story with numbers behind it. Your job is simply to decide which story, or mix of stories, feels closer to how you see the company.

Fair value in this bullish narrative: US$25.78 per share

Gap to that fair value versus the last close of US$22.24: about 13.7% below the narrative fair value

Revenue growth assumption used in this narrative: 3.97% a year

- The bullish story focuses on execution around Aerie, OFFLINE, digital investment and store optimisation, with the idea that better inventory control and supply chain efficiency can support higher net margins.

- Analysts in this camp outline gradual revenue and earnings growth, margin improvement from 3.7% to roughly mid single digits, and support from ongoing share repurchases reducing the share count.

- They still flag risks, including consumer uncertainty, tariffs, currency moves and markdown pressure, but describe these as manageable within a framework that supports the US$25.78 fair value if assumptions on growth, margins and the discount rate hold together.

Fair value in this bearish narrative: US$20.00 per share

Gap to that fair value versus the last close of US$22.24: about 11.2% above the narrative fair value

Revenue growth assumption used in this narrative: 3.62% a year

- The bearish story highlights pressure from e commerce giants, softer mall traffic and a relatively narrow brand set, with concerns that this combination could cap comparable sales and keep the core American Eagle brand trailing peers.

- In this view, analysts still include earnings and margin improvements, but they pair those with a much lower future P/E, effectively arguing that even with better profits the market might not be willing to pay a higher multiple for the stock.

- Upside risks to this view include stronger than expected benefits from celebrity campaigns, Aerie growth, supply chain work and digital improvements, which could challenge the US$20.00 fair value if they prove more powerful or more durable than this narrative assumes.

If you want to go beyond these previews and see how other investors are joining the dots between growth, margins, risks and valuation for American Eagle Outfitters, Curious how numbers become stories that shape markets? Explore Community Narratives.

Do you think there's more to the story for American Eagle Outfitters? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.