Is It Too Late To Reassess EchoStar (SATS) After Its Huge One Year Share Price Jump?

EchoStar Corporation Class A SATS | 0.00 |

- For readers wondering whether EchoStar's recent share price places it in bargain or stretched territory, this article breaks down what the numbers indicate about value.

- At a last close of US$123.70, EchoStar has recorded returns of 1.1% over 7 days, 10.2% over 30 days, 10.3% year to date and a 1 year gain of 450.3%, with a 3 year return of 661.2% and a 5 year return of 427.1%.

- Recent headlines around EchoStar have focused on its sharp share price move and what that implies for expectations around the business. Together with renewed investor attention, this context helps explain why many are reassessing whether the current price still reflects reasonable value or growing risk.

- EchoStar currently has a valuation score of 3 out of 6. The next sections walk through traditional valuation approaches and then finish with a broader framework that can help you judge the stock's value in a more complete way.

Approach 1: EchoStar Discounted Cash Flow (DCF) Analysis

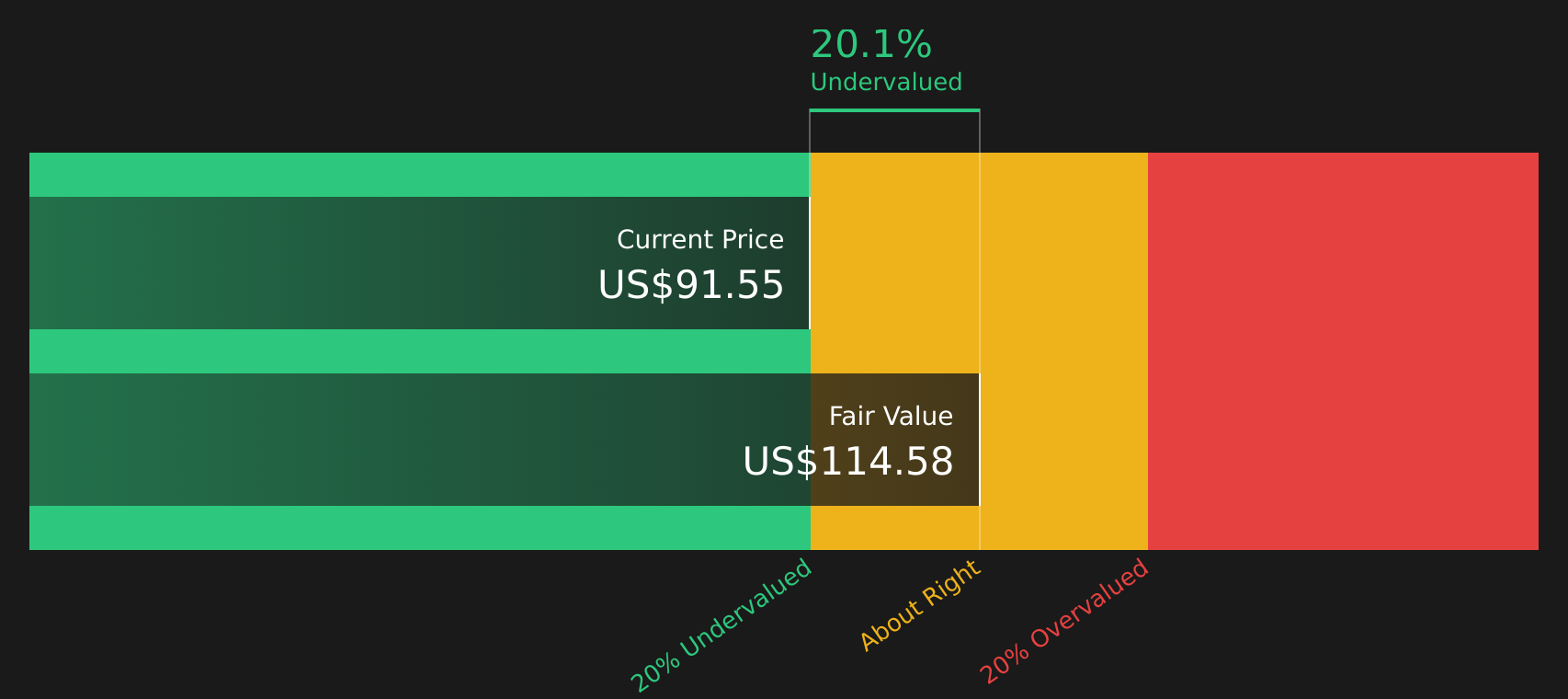

A Discounted Cash Flow model estimates what a company might be worth by projecting its future cash flows and then discounting those back to today, using the idea that money expected in the future is worth less than money in hand now.

For EchoStar, the model used here is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections in US$. The latest twelve month free cash flow is a loss of about US$2.74b, so the story starts from a weak cash flow position. Analysts provide explicit free cash flow estimates out to 2029, and figures for 2030 to 2035 are extended using Simply Wall St assumptions, with projected free cash flow of US$3.16b in 2030. All of these future cash flows are then discounted back to a single present value.

This process produces an estimated intrinsic value of US$184.51 per share, compared with the recent share price of US$123.70. On this model, the stock appears to trade at a discount of about 33.0% to this estimate of intrinsic value.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests EchoStar is undervalued by 33.0%. Track this in your watchlist or portfolio, or discover 53 more high quality undervalued stocks.

Approach 2: EchoStar Price vs Sales

For companies where earnings are less useful because profits are volatile or negative, the P/S ratio often gives a clearer sense of how the market values each dollar of revenue. Investors usually accept a higher or lower P/S depending on what they expect for future growth and how risky those expectations appear, so there is no single "right" number that fits every business.

EchoStar currently trades on a P/S of 2.38x. That sits above the Media industry average of 1.17x and slightly below the peer group average of 2.84x. On the surface, that suggests the market is pricing EchoStar’s sales at a premium to the broader industry but not at the top of its closer peer set.

Simply Wall St’s Fair Ratio for EchoStar is 1.33x. This is a proprietary estimate of what EchoStar’s P/S might be given factors such as its earnings growth profile, industry, profit margins, market cap and stock specific risks. Because it blends these fundamentals, the Fair Ratio can offer a more tailored anchor than simple comparisons with industry or peers. Set against the current 2.38x P/S, the Fair Ratio points to EchoStar trading above that implied level, which suggests the shares screen as overvalued on this metric.

Result: OVERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Upgrade Your Decision Making: Choose your EchoStar Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives let you attach a clear story about a company to your own numbers by linking a view of its future revenue, earnings and margins to a forecast and then to a fair value you can compare with the current share price.

On Simply Wall St’s Community page, Narratives are an accessible tool used by millions of investors that update automatically when fresh information such as earnings, regulatory news or index changes is added. This means your fair value view can move with the facts rather than staying fixed.

For EchoStar, one investor might build a more optimistic Narrative that lines up with a Fair Value of about US$147.00, while another might lean on a more cautious Narrative closer to US$120.00. Each investor can then decide whether the current price around US$123.70 looks high or low relative to their own story driven estimate rather than relying only on headline multiples.

For EchoStar however we will make it really easy for you with previews of two leading EchoStar Narratives:

Each one ties a clear story about the business to a specific fair value, so you can quickly see which version of the EchoStar story feels closer to your own view.

Fair value in this bullish Narrative: US$124.29 per share.

Implied discount to this fair value at the last close of US$123.70: about 0.5% undervalued using the Narrative model.

Revenue trend assumed in this Narrative: 1.22% annual decline.

- Focuses on EchoStar’s plan to blend satellite and terrestrial 5G connectivity to serve carriers, enterprises and governments with wider coverage and potentially higher margin services.

- Highlights how spectrum assets, regulatory support for wider internet access and long term contracts could support earnings and help fund the direct to device LEO constellation.

- Flags key risks including regulatory reviews, large upcoming debt maturities, heavy capital needs for the LEO build out and strong competition from other satellite and terrestrial players.

Fair value in this more cautious Narrative: US$43.91 per share.

Implied premium to this fair value at the last close of US$123.70: about 182% overvalued using the Narrative model.

Revenue trend assumed in this Narrative: 2.30% annual decline.

- Centres on EchoStar’s legacy financial track record, past cash burn and earlier weak mobile operations, with concerns that the recent shift in story may be running ahead of fundamentals.

- Frames the reallocation of spectrum into exposure to a larger space ecosystem as bold but also points out that EchoStar still faces all the usual execution and capital allocation questions.

- Treats EchoStar’s role in the broader space supply chain as interesting but stresses that outcomes around external partners, index inclusion and future space economy growth remain uncertain.

These two Narratives sit at opposite ends of the current Community view, and your own stance on EchoStar’s risks, capital needs and role in future connectivity will likely place you somewhere along that spectrum.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for EchoStar on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for EchoStar? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.