Is It Too Late To Reassess QCR Holdings (QCRH) After Its Strong Multi‑Year Run?

QCR Holdings, Inc. QCRH | 91.00 91.00 | +0.40% 0.00% Pre |

- If you are wondering whether QCR Holdings is still reasonably priced after its recent run, this breakdown will help you see how the current share price lines up against the underlying business.

- The stock last closed at US$92.38, with returns of 8.4% over 30 days, 12.5% year to date, 19.8% over 1 year, 74.5% over 3 years and 127.6% over 5 years. This naturally raises questions about how much value is already reflected in the price.

- Recent price movements have come alongside ongoing attention on regional banks, with investors focusing on balance sheet resilience, credit quality and how local lending franchises are positioned within their markets. Taken together, this context matters for assessing whether QCR Holdings is being treated as a relatively resilient bank or one that carries higher perceived risk.

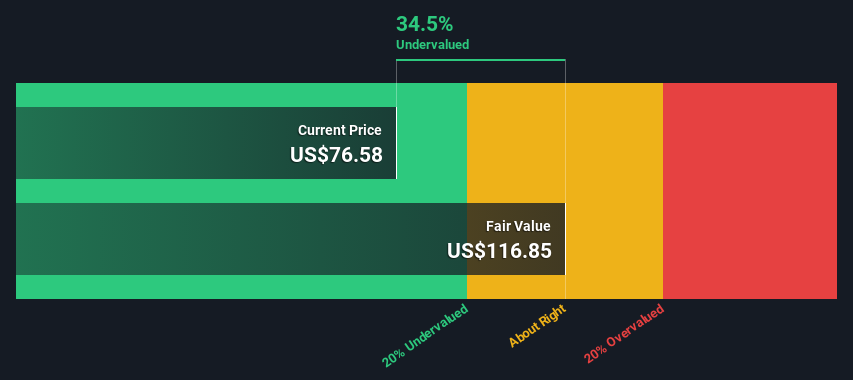

- On Simply Wall St's valuation checks, QCR Holdings has a value score of 3/6, which suggests the stock screens as undervalued on half of the metrics used. Next, we will look at what standard valuation approaches say about that score, and then finish with a more holistic way of thinking about valuation that goes beyond a single number.

Approach 1: QCR Holdings Excess Returns Analysis

The Excess Returns model looks at how much profit a company is expected to generate above the return that shareholders require, and then links that to the value of its equity today.

For QCR Holdings, the starting point is its book value of $66.64 per share and a stable earnings figure of $8.84 per share, based on weighted future Return on Equity estimates from 4 analysts. The average Return on Equity used in the model is 11.31%, compared with a cost of equity of $5.62 per share. That gap translates into an estimated excess return of $3.22 per share.

The model then projects a stable book value of $78.13 per share, sourced from weighted future book value estimates from 5 analysts, and applies the excess return stream to arrive at an intrinsic value of $163.33 per share using the Excess Returns framework.

Against the recent share price of roughly $92.38, this implies the stock is 43.4% undervalued according to this method.

Result: UNDERVALUED

Our Excess Returns analysis suggests QCR Holdings is undervalued by 43.4%. Track this in your watchlist or portfolio, or discover 53 more high quality undervalued stocks.

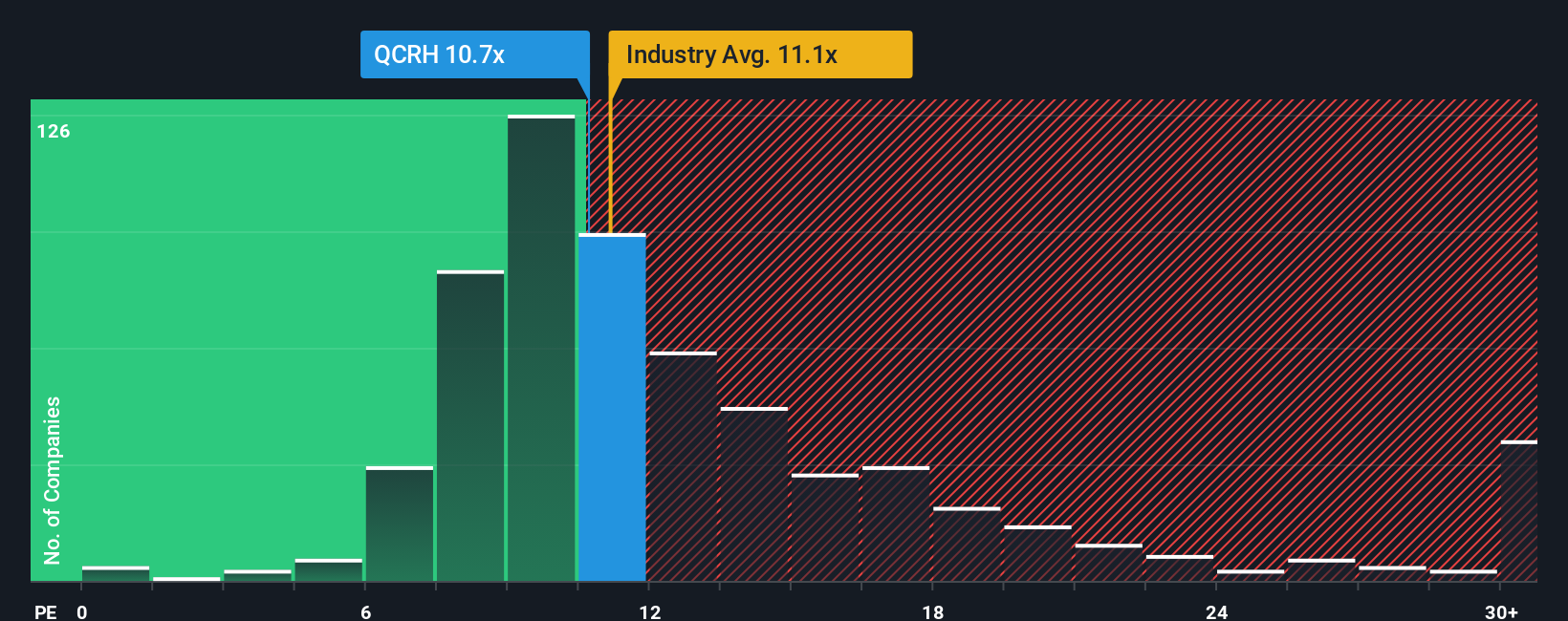

Approach 2: QCR Holdings Price vs Earnings

For a profitable bank like QCR Holdings, the P/E ratio is a useful shorthand for how much investors are paying for each dollar of earnings. It ties directly to what you see on the income statement and is widely used for comparing banks that have relatively steady profitability.

What counts as a “normal” P/E ratio often reflects what the market expects for earnings growth and how it views risk. Higher expected growth or lower perceived risk can support a higher multiple, while slower growth or higher risk can point to a lower one.

QCR Holdings currently trades on a P/E of 12.12x. That sits above the Banks industry average of 11.89x and below the peer group average of 14.65x. Simply Wall St’s Fair Ratio for QCR Holdings is 11.27x, which is its proprietary view of what the P/E “should” be after factoring in elements like earnings growth, profit margins, industry, market cap and company specific risks.

Compared with simple industry or peer averages, the Fair Ratio aims to be more tailored because it adjusts for those business fundamentals rather than relying on broad group comparisons alone. Since the current P/E is modestly above the Fair Ratio, this framework points to QCR Holdings being slightly overvalued on this metric.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 23 top founder-led companies.

Upgrade Your Decision Making: Choose your QCR Holdings Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which is Simply Wall St's way for you to set out your own story for QCR Holdings. You can link that story to a forecast for revenue, earnings and margins, and then see the fair value that follows from those assumptions, all in an easy tool on the Community page. Millions of investors already use this to compare their Fair Value to the current price, react quickly as Narratives update when new news or earnings arrive, and see how two investors can look at the same stock very differently. For example, one QCR Holdings Narrative might lean on expectations for digital transformation, affordable housing demand and wealth management growth that support a higher fair value of US$102.25 with a future P/E of 13.68x. A more cautious Narrative might focus on regulatory, credit and digital execution risks and anchor closer to the lower analyst target of US$89.30 at a future P/E of 13.8x. This gives you a clear, side by side view of how different stories translate into different numbers.

Do you think there's more to the story for QCR Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.