Is It Too Late To Reassess VF (VFC) After A 53% One-Year Rally?

V.F. Corporation VFC | 0.00 |

- Wondering if V.F at around US$18.32 is still offering value after a volatile few years, or if the easy gains are already behind it.

- The stock is up 53.5% over the last year, alongside a 0.9% year to date return, an 8.6% gain over 30 days and a 2.1% decline over the last week. This suggests shifting views on both its recovery potential and risk.

- Recent headlines around V.F have focused on the company reshaping its portfolio and responding to changing consumer demand. Investors are closely watching how these moves affect brand strength and profitability. At the same time, there has been ongoing discussion about how management is handling leverage and capital allocation, which feeds into how the market is pricing the stock today.

- Right now V.F scores a 3 out of 6 valuation checks. The stock screens as undervalued on half of the methods that will be covered next, and there is an even richer way to think about valuation waiting at the end of this article.

Approach 1: V.F Discounted Cash Flow (DCF) Analysis

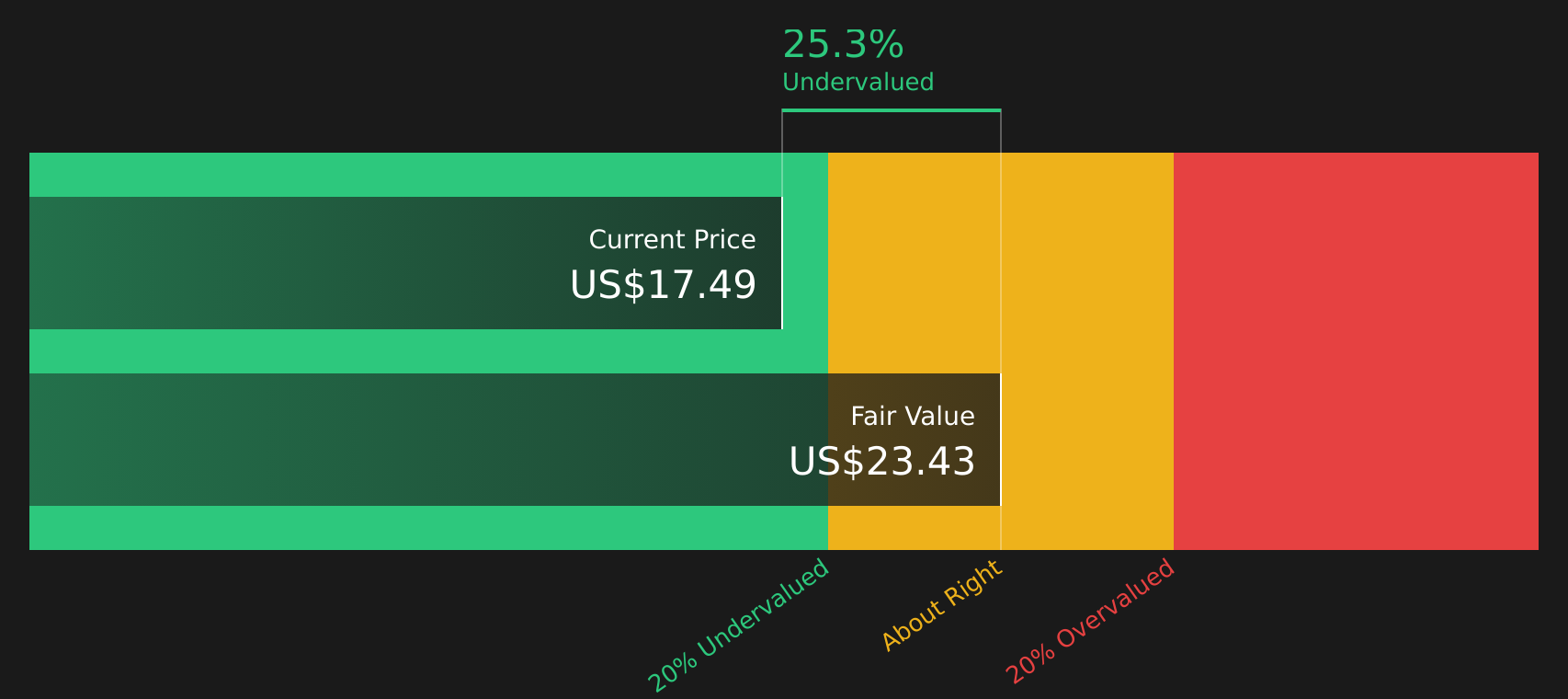

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth by projecting the cash the company may generate in the future and discounting those amounts back to today.

For V.F, the model used is a 2 Stage Free Cash Flow to Equity approach, based on current Free Cash Flow of about $303.7 million. Analyst estimates feed into the early years, and from 2026 to 2035 the projections range from $467.1 million to $1.35 billion in Free Cash Flow, all in dollar terms. These later years combine analyst inputs and extrapolations by Simply Wall St to build a 10 year view of potential cash generation.

When all those future cash flows are discounted back, the estimated intrinsic value comes out at about $32.06 per share. Against the recent share price of around $18.32, this implies the stock screens as about 42.9% undervalued according to this DCF model.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests V.F is undervalued by 42.9%. Track this in your watchlist or portfolio, or discover 51 more high quality undervalued stocks.

Approach 2: V.F Price vs Earnings

P/E is a common way to value profitable companies because it links what you pay for the stock to what the business earns per share. A higher or lower P/E often reflects what the market is factoring in around future growth and risk, so what counts as a “normal” P/E can vary a lot between companies and industries.

V.F currently trades on a P/E of 32.0x. That sits above the Luxury industry average of about 21.2x, and below the peer group average of 52.9x. Those comparisons are useful, but they do not adjust for V.F specific profile.

This is where Simply Wall St’s Fair Ratio comes in. It is a proprietary estimate of what V.F P/E might be given its earnings growth profile, profit margins, industry, market cap and risk factors. For V.F, the Fair Ratio is 27.7x, which is lower than the current 32.0x. On this basis, the stock screens as trading above the Fair Ratio using the P/E approach.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose Your V.F Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives are introduced, which let you set a story for V.F by linking your view on its brands, Vans recovery, execution and risks to specific forecasts for future revenue, earnings and margins, and then to a Fair Value that can be compared directly to today’s price.

On Simply Wall St’s Community page, Narratives are presented as easy-to-use templates that sit on top of the same type of numbers analysts use. This allows you to quickly see how a Fair Value that sits near US$39.50 or closer to US$14.00 might reflect very different expectations for V.F’s earnings power, balance sheet progress and brand health.

Because these Narratives are refreshed when new information arrives, such as earnings updates, brand commentary or changes to analyst assumptions, they give you a living view of how your V.F story translates into a Fair Value and whether that still lines up with the current share price.

For V.F however, here are previews of two leading V.F Narratives to make the analysis easier to follow:

First is a balanced, analyst-style take that treats V.F as roughly fairly priced around current levels, with the outcome heavily tied to how well Vans and overall execution improve from here.

Fair value in this narrative: US$20.70 per share.

At a last close of US$18.32, the stock sits about 11.5% below that fair value estimate.

Revenue growth assumption: 2.68% a year.

- The narrative expects modest revenue growth and a move in profit margins from 2.3% to 7.3% over 3 years, supported by premiumisation, digital channels and a tighter portfolio.

- Key swing factors include Vans brand repair, progress on supply chain and inventory, and the ability to manage leverage while still investing in product and marketing.

- Analysts in this camp cluster around a consensus fair value of US$20.70, with a wide spread between US$14.00 and US$39.50 that you are encouraged to sense check against your own assumptions.

The second narrative offers a cautious view that treats V.F as pricing in more optimism than some analysts are comfortable with, especially around brand health and future P/E.

Fair value in this narrative: US$14.00 per share.

At a last close of US$18.32, the stock screens as about 31.8% above that fair value estimate.

Revenue growth assumption: 2.23% a year.

- This narrative leans on concerns around structural pressure on legacy brands, ongoing discounting and higher environmental and regulatory costs that could weigh on long term earnings power.

- It assumes similar earnings growth to consensus in dollar terms, but pairs that with a much lower future P/E of 9.0x, which pulls the fair value estimate down to US$14.00.

- To align with this view, you would need to be comfortable that by 2029, V.F earns US$847.2m yet still trades on that lower multiple, reflecting a market that prices in continued brand and execution risk.

Taken together, these two Narratives provide a structured way to frame the current price against a fair value range from about US$14.00 to US$39.50 and to decide which assumptions on Vans, margins, leverage and consumer demand align best with your own view of the stock.

Do you think there's more to the story for V.F? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.