Is Kimberly-Clark Attractive After a 10.6% Drop So Far in 2025?

Kimberly-Clark Corporation KMB | 96.13 | -1.48% |

Thinking about Kimberly-Clark stock? You are not alone, especially now, with the company's share price at $116.72 after recently sliding by 2.9% over the past week and down 4.8% in the last month. Year to date, shares have pulled back 10.6%, and they sit close to 10% below where they were a year ago. But taking a longer view, the stock has managed gains of 6.5% over three years and 3.3% in five years. This suggests it is still playing the long game in a market full of quick swings.

So, what is influencing these moves? Much of the recent activity ties back to shifts in global consumer demand and changing costs for materials and logistics. These are big levers for Kimberly-Clark given its familiar lineup of personal care products. Earlier this quarter, industry reports pointed to both increased competition and innovation efforts in the sector, fueling speculation about who will win on margins and market share.

With all the recent action, you might wonder if Kimberly-Clark is an overlooked bargain or if broader market uncertainty just makes it look cheap. Here is where the numbers get interesting: our valuation analysis checks for six core signs a company is undervalued, and Kimberly-Clark scores a solid four out of six. That places it in an intriguing spot for investors trying to balance risk and reward.

Let’s break down the different ways analysts and savvy investors size up a stock like this. If you are after a more holistic approach that goes beyond the usual metrics, stick around for an even smarter way to assess value at the end.

Approach 1: Kimberly-Clark Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model works by estimating a company’s future free cash flows and then discounting them back to their present value. This approach captures not just near-term performance but also the company’s long-term earning power, which is useful for investors seeking a holistic look at intrinsic value.

For Kimberly-Clark, analysts report that the company generated free cash flow of $2.1 billion over the last twelve months. Looking ahead, analysts expect free cash flows to remain in the range of $2.05 billion to $2.2 billion over the next several years. Projections for 2035, as extrapolated by Simply Wall St, reach $2.14 billion. This stable cash generation underpins the company’s value in the marketplace.

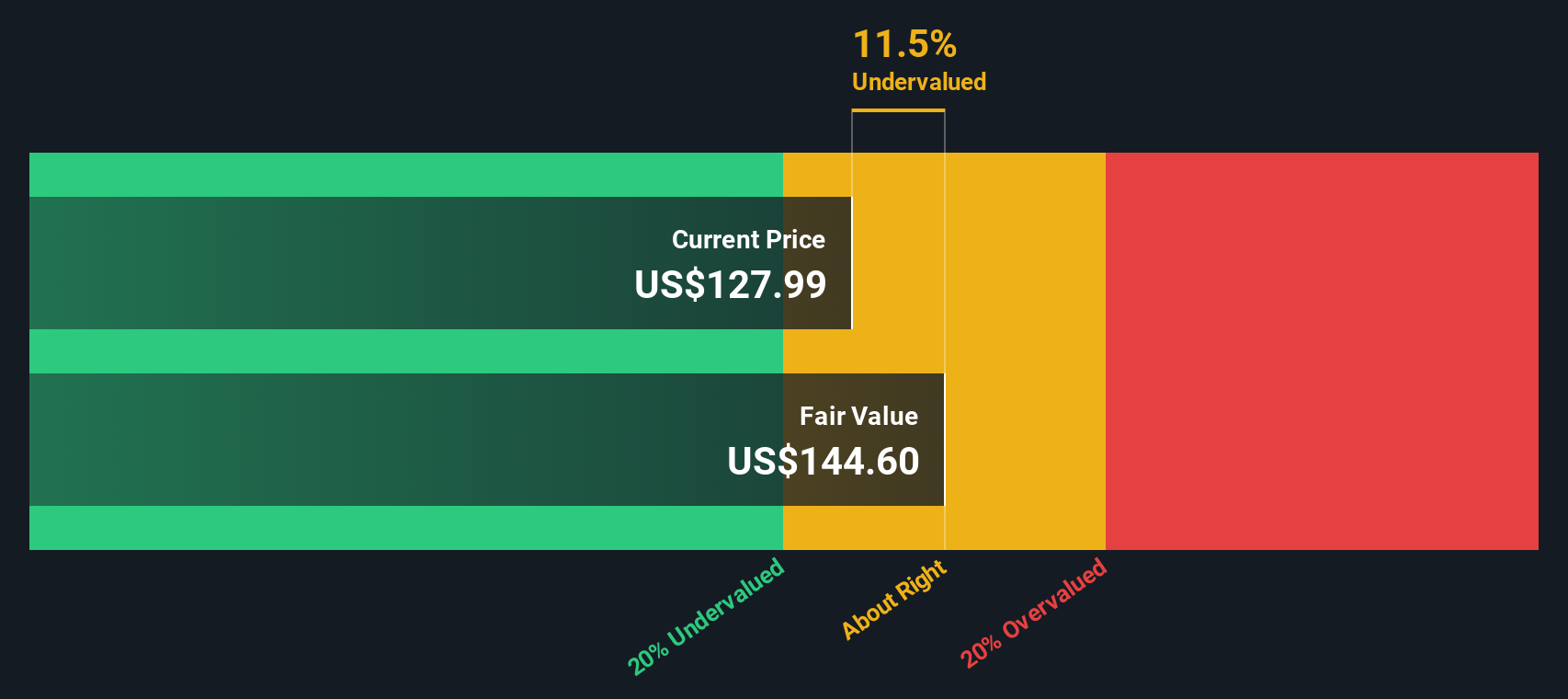

Based on these cash flow projections and the 2 Stage Free Cash Flow to Equity model, the estimated intrinsic value for Kimberly-Clark stands at $137.05 per share. With the current market price at $116.72, this DCF-based analysis suggests that the stock is trading at a 14.8 percent discount to its intrinsic value, indicating it may be undervalued at current levels.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Kimberly-Clark is undervalued by 14.8%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

Approach 2: Kimberly-Clark Price vs Earnings

The Price-to-Earnings (PE) ratio is a popular valuation metric for profitable companies like Kimberly-Clark because it allows investors to quickly assess how much they are paying for each dollar of earnings. A lower PE can signal potential undervaluation, while a higher PE may reflect higher growth expectations or, in some cases, increased risk.

What determines a “fair” PE ratio is partly shaped by a company’s growth outlook and risk profile. Strong earnings growth and stable prospects typically justify higher PE ratios, while slow growth or elevated risk tend to push them lower. For this reason, comparing PE ratios across companies or industries works best when growth and risk levels are similar.

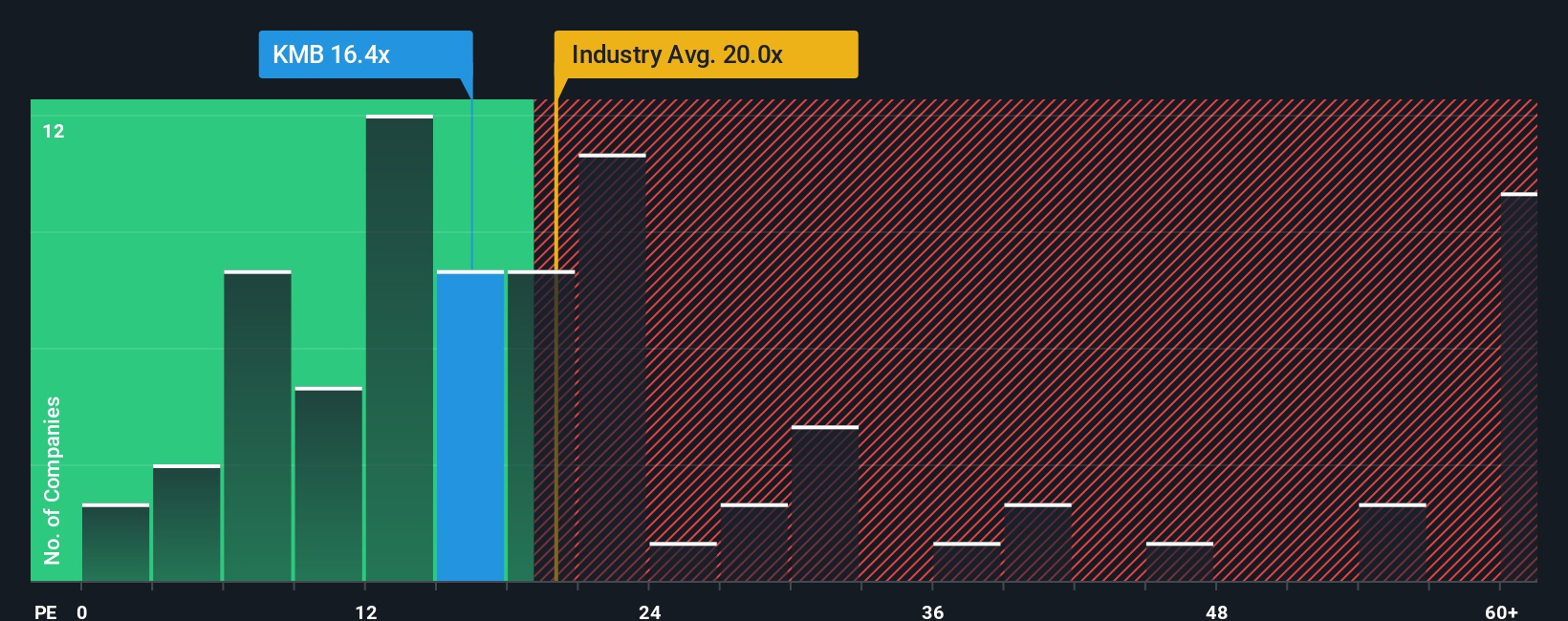

Currently, Kimberly-Clark trades at a PE ratio of 15.8x. This is noticeably below both the Household Products industry average of 18.7x and the peer average of 23.1x. Instead of stopping there, consider Simply Wall St’s proprietary “Fair Ratio.” This figure adjusts for not just profit growth and margin, but also market cap, industry trends, and risk factors unique to Kimberly-Clark. This makes it a stronger benchmark than peer or industry comparisons alone.

For Kimberly-Clark, the Fair Ratio is 21.2x. Compared to the company’s current multiple of 15.8x, this suggests the stock is attractively valued relative to its fundamental outlook and characteristics.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Kimberly-Clark Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let’s introduce you to Narratives. A Narrative is more than just a number or price target. It is a story you create that connects your view of a company, like Kimberly-Clark, to a specific financial forecast and ultimately to your estimate of fair value. Narratives help you clarify your assumptions about future revenues, margins, and risks, and allow you to see how your outlook compares with the current share price.

With Narratives, you do not need to be a financial expert to make informed decisions. On Simply Wall St’s Community page, millions of investors share and compare their Narratives, each reflecting a personal perspective on what drives a company’s outlook. Narratives automatically update when new news or results are released, keeping your view fresh and relevant.

This approach lets you easily see if your expectations for Kimberly-Clark’s future support the idea of buying, selling, or holding the stock by comparing your own Fair Value with the market price. For example, one investor’s Narrative based on long-term brand strength and premium product growth could justify a fair value of $162. Another, more cautious, Narrative focused on muted demand and stiffer competition might put fair value at just $118.

Do you think there's more to the story for Kimberly-Clark? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.