Is Kraft Heinz Poised for a Rebound After 19% Drop and Brand Refresh in 2025?

Kraft Heinz Company KHC | 22.27 | -0.98% |

- Wondering if Kraft Heinz could be a hidden gem or a value trap? You are not alone, and there is a lot to unpack about where the stock stands today.

- Shares have dipped by 18.8% year-to-date, and the 1-year return sits at -14.6%. This suggests a reset in investor sentiment and some serious questions about future growth.

- Aside from recent price moves, Kraft Heinz has made headlines with strategic product innovations and new sustainability initiatives. The company is aiming to refresh its brand in a rapidly changing consumer landscape. These steps may influence the company's long-term prospects and have contributed to the fluctuations in its market value.

- Currently, Kraft Heinz scores a 4/6 on our valuation checks. This means it appears undervalued in the majority of fundamental areas we track. We will break down what this score means using standard techniques, and will reveal a smarter approach for assessing fair value by the end of the article.

Approach 1: Kraft Heinz Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company's value by projecting its future cash flows and then discounting them back to today. This process gives investors an idea of the intrinsic value of the stock. For Kraft Heinz, this model uses the 2 Stage Free Cash Flow to Equity approach.

Currently, Kraft Heinz produces $3.54 Billion in Free Cash Flow. Analysts have provided detailed forecasts through 2028. Beyond that, Simply Wall St extrapolates these numbers based on trends and reasonable assumptions. By 2035, Kraft Heinz's Free Cash Flow is projected to reach approximately $4.0 Billion.

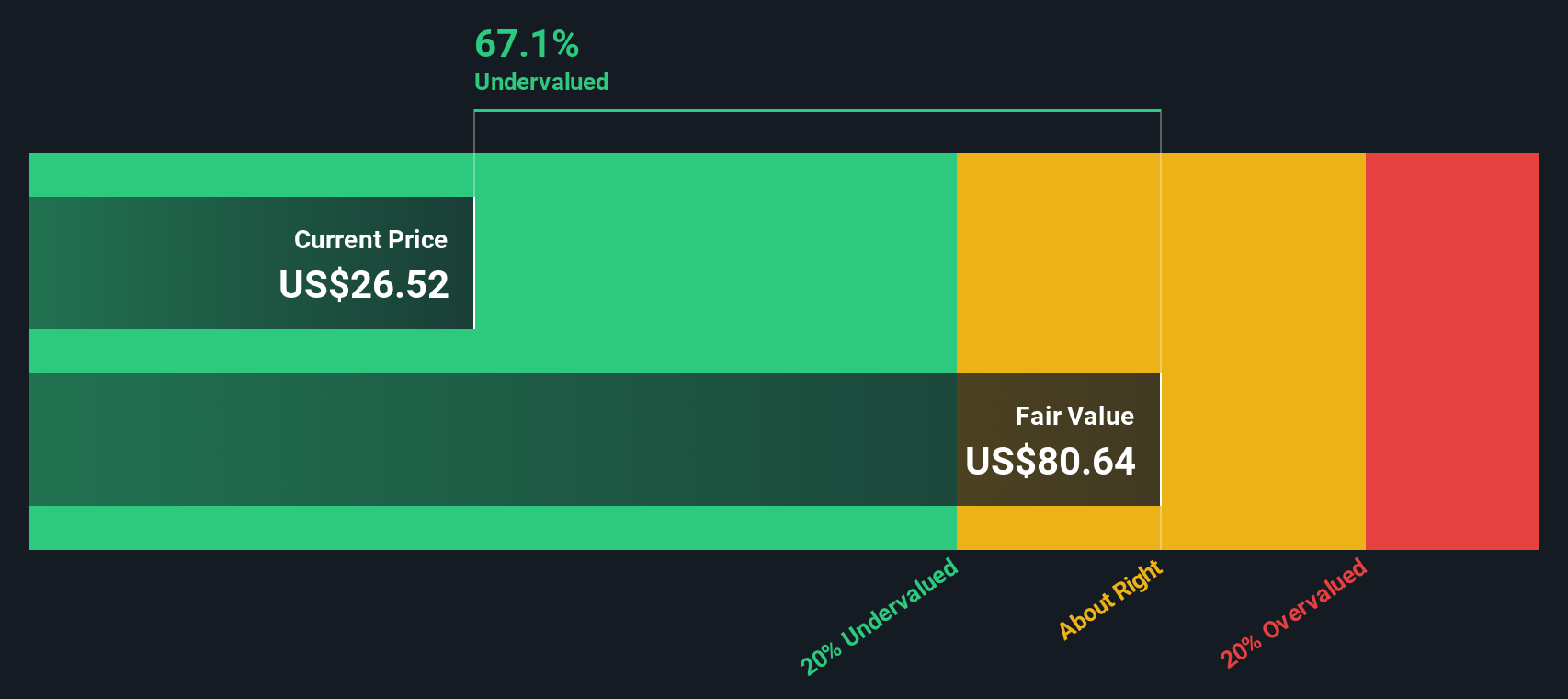

Based on these cash flow projections, the DCF model estimates the intrinsic fair value of Kraft Heinz at $68.79 per share. With the stock trading at a significant discount, the DCF calculation suggests Kraft Heinz is about 63.7% undervalued compared to its intrinsic value.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Kraft Heinz is undervalued by 63.7%. Track this in your watchlist or portfolio, or discover 901 more undervalued stocks based on cash flows.

Approach 2: Kraft Heinz Price vs Sales Multiple

For companies like Kraft Heinz with stable revenue streams and established operations, the Price-to-Sales (P/S) ratio is a useful valuation tool. This multiple is especially relevant when net income may be affected by non-cash items, one-off events, or unusually high expenses. Growth expectations and risks factor into what investors view as a “fair” P/S ratio. Higher growth and strong margins typically warrant a higher ratio, while slow growth and heightened risks drive it lower.

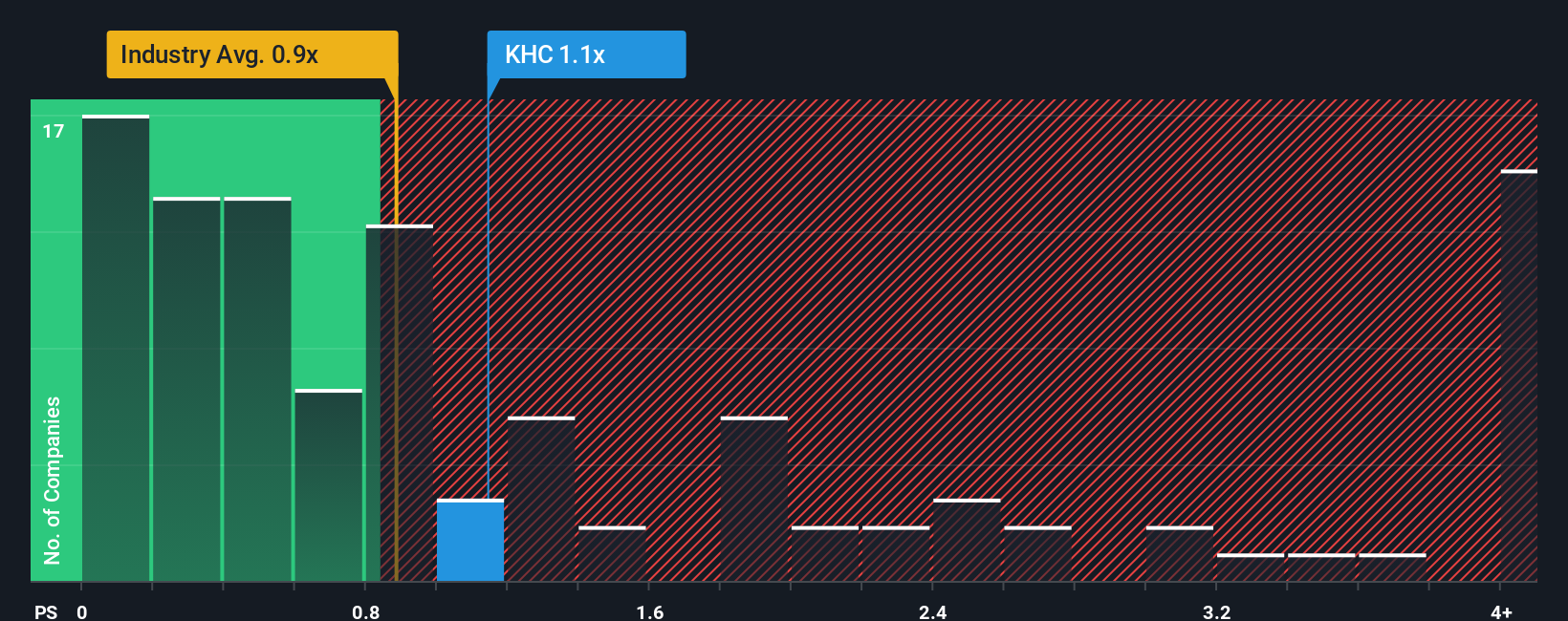

Currently, Kraft Heinz trades at a P/S ratio of 1.17x. This compares to a peer average of 1.80x and an industry average of 0.79x. These benchmarks give a sense of the valuation range, but they do not account for the company’s specific risks, growth outlook, profit margins, or overall market cap.

That is where Simply Wall St's Fair Ratio comes in. The Fair Ratio for Kraft Heinz is calculated as 1.36x, which incorporates the company’s future earnings growth, industry position, profitability and unique risk profile. Unlike a straight comparison to the industry or peers, the Fair Ratio reflects a much more personalized assessment of what the multiple should be for Kraft Heinz right now.

Since Kraft Heinz’s current P/S multiple is below the Fair Ratio, the stock appears undervalued on this measure.

Result: UNDERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1412 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Kraft Heinz Narrative

Earlier, we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. A Narrative is a simple yet powerful tool that helps you define your own story behind a company like Kraft Heinz by connecting your expectations for its future (such as projected revenue, earnings, and margins) directly to a calculated fair value. Unlike traditional models, Narratives let you see, adjust, and explain the assumptions driving your view. This makes your investment decisions more personal and transparent.

Narratives essentially link a company’s journey to a clear financial forecast and a tailored fair value. On Simply Wall St’s Community page, millions of investors can create, share, and compare these Narratives. This makes them an accessible solution for beginners and experts alike. As you monitor Kraft Heinz, you can track how different Narratives suggest when it makes sense to buy or sell by comparing fair value estimates to live prices.

What makes Narratives especially useful is that they update automatically whenever new financials, news, or company announcements are released, so your story always reflects reality. For Kraft Heinz, you might see a bullish investor justify a fair value of $51.00 based on expectations of robust revenue and margin growth, while a more bearish analyst sees fair value closer to $27.00. This highlights the diversity of perspectives and the power of building your own Narrative.

Do you think there's more to the story for Kraft Heinz? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.