Is Lakeland Financial (LKFN) Stock Stretched Or Still Reasonable?

Lakeland Financial Corporation LKFN | 0.00 |

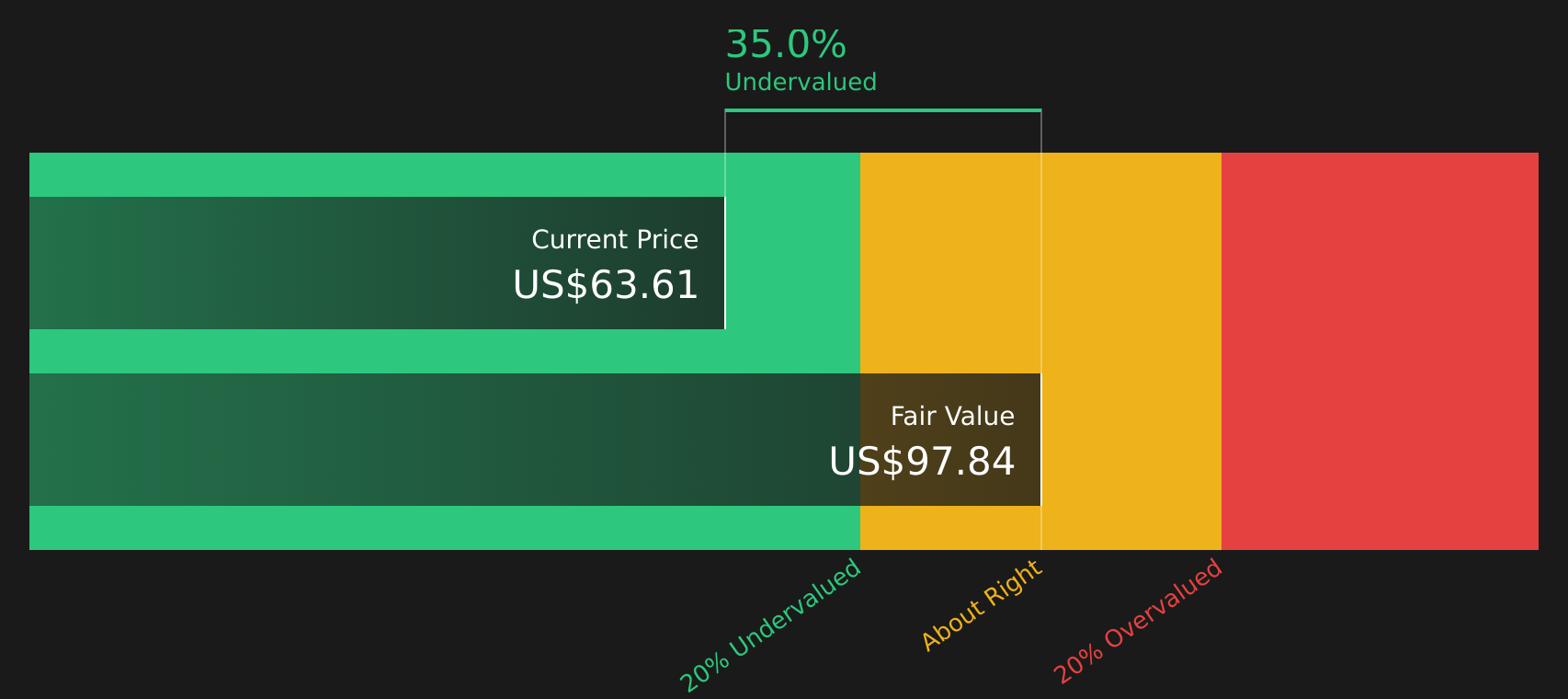

Lakeland Financial stock has delivered a 22.3% total return over the past three years, yet its current valuation signals are split, with the Excess Returns intrinsic value estimate pointing to meaningful upside while earnings based multiples suggest the shares are on the expensive side. That tension leaves investors weighing a stock that screens as 37.0% undervalued on one model but overvalued on traditional ratios, with a mixed overall value score.

- Over the past three years, Lakeland Financial has returned 22.3%, which suggests the stock has already rewarded patient holders even as opinions differ on whether it is still attractively priced.

- Future valuation may be supported if Lakeland Financial can continue to convert earnings into steady cash generation, while any erosion in asset quality or capital strength could pressure both its intrinsic value estimate and market multiples.

- The company scores 3 of 6 on our valuation checks, which is a mixed picture rather than a clear bargain or clear overvaluation, with the scorecard available at 3.

The issue now is whether Lakeland Financial’s current share price around US$61.63 offers enough margin of safety when its intrinsic value estimate and market multiples are pointing in opposite directions.

Is Lakeland Financial Still Cheap on Excess Returns?

The Excess Returns model looks at how efficiently Lakeland Financial converts its equity base into earnings above the cost of that equity. For Lakeland Financial, the inputs point to a bank with solid but not extreme profitability, which helps explain why this approach suggests more upside than basic trading multiples do.

The model uses a Book Value of $30.04 per share and a Stable EPS of $4.67 per share, based on weighted future Return on Equity estimates from 4 analysts. With an Average Return on Equity of 14.00% and a Cost of Equity of $2.37 per share, the implied Excess Return of $2.30 per share supports a Stable Book Value of $33.37 per share from the same analyst set. Putting these together gives an intrinsic value estimate of $97.84 per share, which is above the current share price around $61.63 and implies the stock is 37.0% undervalued under this method.

On this Excess Returns view, Lakeland Financial stock currently screens as undervalued versus its estimated intrinsic worth.

Our Excess Returns analysis suggests Lakeland Financial is undervalued by 37.0%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Does Lakeland Financial Look Pricey on Earnings?

P/E is often the cleanest starting point for a bank like Lakeland Financial because earnings are a key lens on how effectively it is using its balance sheet. On this measure, Lakeland Financial trades at about 14.0x earnings, compared with an industry average of roughly 12.3x and a peer group average of 15.3x, so it sits between the broader sector and closer banking peers.

The fair P/E ratio implied by the model is 11.1x, which is lower than Lakeland Financial’s current 14.0x. That gap suggests the stock is pricing in more optimistic conditions than the fair multiple would indicate, even if it is not at a large premium to peers. For investors, that means the P/E signal contrasts with the earlier intrinsic value estimate, pointing to a stock that does not obviously screen as a bargain on earnings alone.

On the P/E yardstick, Lakeland Financial stock currently appears expensive relative to the fair multiple implied by its fundamentals.

The Lakeland Financial Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Lakeland Financial pick up where this valuation split leaves off, spelling out which combinations of Lakeland Financial's future growth, margins and earnings would need to hold for the stock to be worth materially more or less than today. Each Narrative treats fair value as a thesis about how the business might develop over time. This allows you to see how that view holds up as new information comes through, all on Simply Wall St's Community page.

If you have a number driven view on where Lakeland Financial's growth, margins and execution go from here, share a Narrative in the Simply Wall St community and set out the case in a way others can test against the data. It is a chance to add your voice, set a clear thesis on Lakeland Financial's stock and see how it stands up as future results come through.

Do you think there's more to the story for Lakeland Financial? Head over to our Community to see what others are saying!

The Bottom Line

For Lakeland Financial, the intrinsic value work, including the Excess Returns view, points to the stock as undervalued, while the earnings multiple suggests it is overvalued relative to a fair P/E. That split reflects two different lenses: one focused on how efficiently equity is turned into excess returns over time, and the other on what the market is currently willing to pay for each dollar of earnings. With the broader valuation checks landing in mixed territory, the key factor from here is whether Lakeland Financial delivers the earnings and balance sheet outcomes that keep justifying a richer multiple than the intrinsic value models imply, or instead bring the market closer to those estimates.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.