Is Life Time (LTH) Turning Its Gyms Into a Defensible Wellness Ecosystem or a Costly Experiment?

Life Time Group Holdings, Inc. LTH | 0.00 |

- In recent coverage, Life Time Group Holdings has been highlighted for reshaping its traditional gym model into a broader wellness and lifestyle platform spanning physical clubs, nutrition, digital tools, and preventive care services.

- This repositioning toward an integrated, higher-touch health offering sets Life Time apart from conventional fitness operators and may influence how investors assess its long-term business mix and resilience.

- We’ll now examine how Life Time’s evolution into a comprehensive wellness brand might influence its existing investment narrative and growth assumptions.

Rare earth metals are the new gold rush. Find out which 30 stocks are leading the charge.

Life Time Group Holdings Investment Narrative Recap

To own Life Time Group Holdings, you need to believe its shift from gyms to a full-service wellness platform can keep attracting higher-value members and support club expansion, despite high capital needs and debt. The recent coverage of Life Time’s outperformance in the Consumer Discretionary sector is encouraging but does not materially change the near term catalyst, which remains execution on new clubs and wellness offerings, or the key risk around funding that growth efficiently.

Among recent developments, the launch of Dynamic Nutrition Coaching in May 2026 looks most relevant. It reinforces Life Time’s push into integrated, higher margin services that can increase revenue per member and support the wellness-platform thesis behind the stock, while also tying into digital tools and in-club programming. How successfully Life Time scales offerings like this, alongside its expanding club footprint, will be central to whether current growth expectations hold up.

Yet behind the wellness story, investors should be aware of how Life Time’s capital intensive club growth and sale leaseback reliance could...

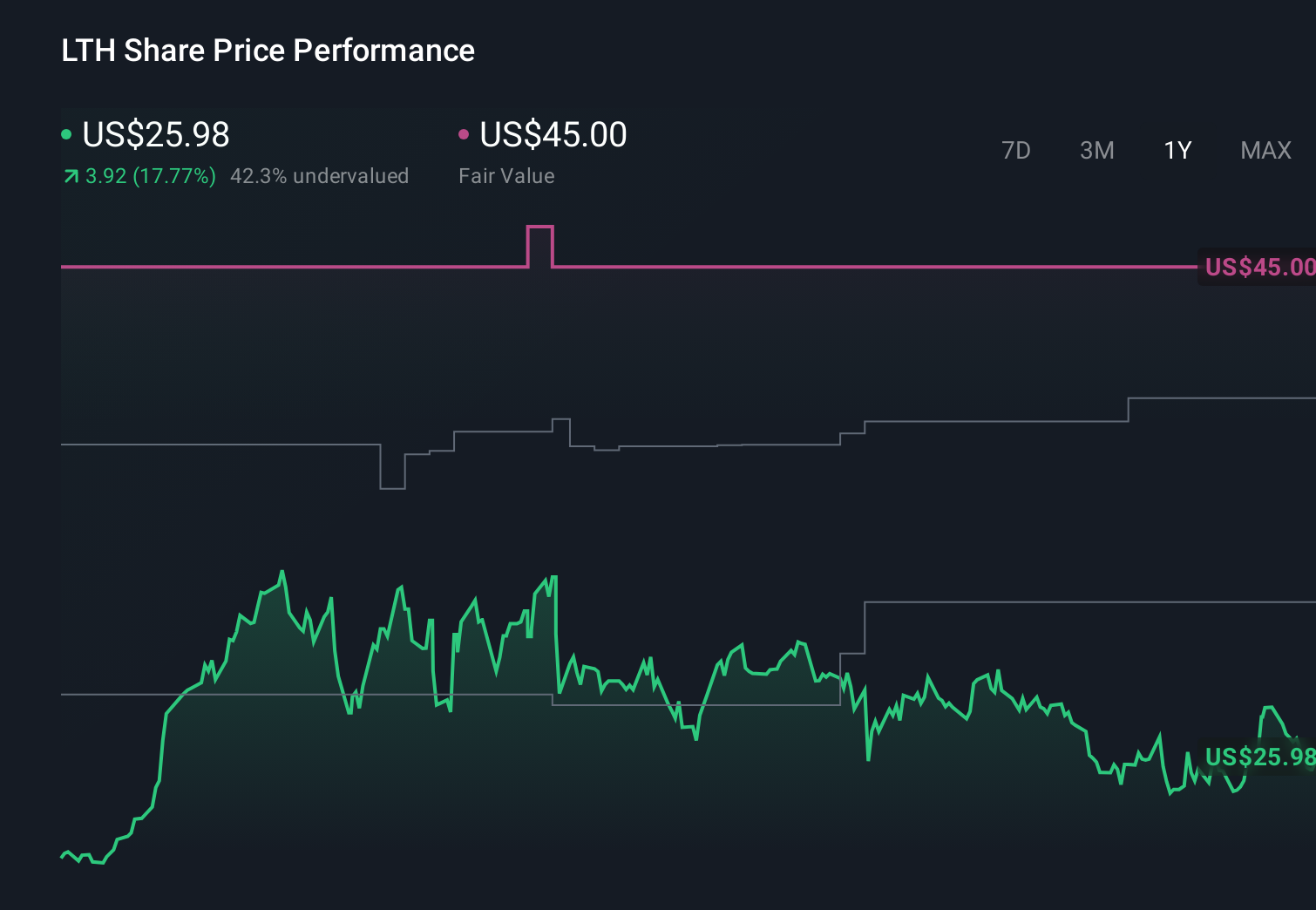

Life Time Group Holdings' narrative projects $4.2 billion revenue and $434.5 million earnings by 2029.

Uncover how Life Time Group Holdings' forecasts yield a $41.00 fair value, a 19% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already projecting 9.8 percent annual revenue growth to about US$4.1 billion by 2029, yet compared with the concern that aggressive expansion could strain sale leasebacks and cash flow, this is a far more cautious story than the consensus, and it may shift again as the latest wellness and performance headlines are fully reflected in new assumptions.

Explore 2 other fair value estimates on Life Time Group Holdings - why the stock might be worth as much as 19% more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Life Time Group Holdings research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Life Time Group Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Life Time Group Holdings' overall financial health at a glance.

No Opportunity In Life Time Group Holdings?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.