Is Lincoln Educational Services (LINC) Still Attractive After A 108% Year To Date Surge?

Lincoln Educational Services Corporation LINC | 0.00 |

- If you are wondering whether Lincoln Educational Services at US$48.40 still offers value after a strong run, the key is to separate price excitement from underlying worth.

- The stock has eased around 1.4% over the past week, but sits up 23.8% over the past month, 107.6% year to date, and 119.8% over the past year, with a very large gain over three years that is more than 7x. This naturally raises questions about what is already priced in.

- Recent coverage has focused on Lincoln Educational Services as an education provider in the Consumer Services sector, drawing attention to how investors are reacting to its positioning and prospects. This coverage helps explain why the share price has seen strong multi year returns, as investors reassess both the opportunities and the risks around the business.

- Even with those returns, Lincoln Educational Services holds a valuation score of 1/6. Next, you will see how different valuation methods judge the stock, and then finish with a more holistic way to think about value that goes beyond any single model.

Lincoln Educational Services scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Lincoln Educational Services Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model looks at the cash Lincoln Educational Services is expected to generate in the future and discounts those projections back to today, aiming to estimate what the stock could be worth right now.

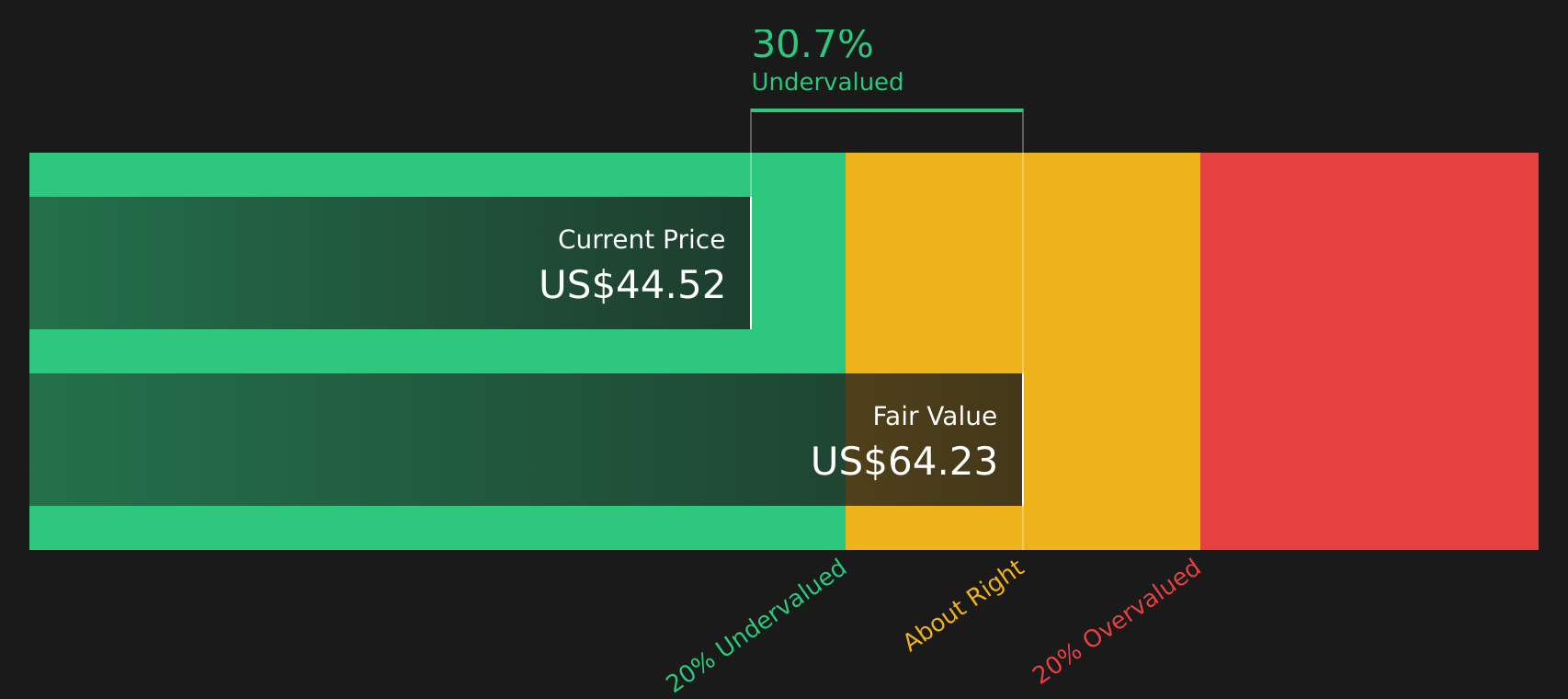

For Lincoln Educational Services, the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow shows an outflow of about $4.22 million, but analysts and extrapolated estimates point to positive free cash flows ahead. For example, projected free cash flow for 2026 is $5.74 million and for 2030 it is $50.00 million, all in $. Simply Wall St extrapolates cash flows beyond the analyst horizon out to 2035, then discounts each year back to today.

Pooling those discounted figures together results in an estimated intrinsic value of about $60.02 per share. Compared with the recent share price of $48.40, the model suggests the stock trades at roughly a 19.4% discount, indicating it appears undervalued under this method alone.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Lincoln Educational Services is undervalued by 19.4%. Track this in your watchlist or portfolio, or discover 49 more high quality undervalued stocks.

Approach 2: Lincoln Educational Services Price vs Earnings

For profitable companies, the P/E ratio is a useful way to think about value because it links what you pay for the stock to the earnings the company is already generating. A higher or lower P/E often reflects what the market expects for future growth and how much risk investors see in those earnings.

If investors expect stronger growth or lower risk, they may be willing to pay a higher P/E, while slower expected growth or higher risk usually lines up with a lower, more cautious multiple. What counts as a “normal” P/E therefore depends on both outlook and risk level for that specific business.

Lincoln Educational Services currently trades on a P/E of 68.51x. That sits above the Consumer Services industry average of 16.25x and the peer average of 56.76x. Simply Wall St’s Fair Ratio for Lincoln Educational Services is 26.07x, which is a proprietary estimate of what the P/E might be given factors such as earnings growth, profit margins, market cap, risk profile and industry. This tailored Fair Ratio can be more informative than a simple comparison with peers or the broad industry because it is specific to the company’s characteristics. With the current P/E of 68.51x versus a Fair Ratio of 26.07x, the stock screens as expensive on this measure.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Lincoln Educational Services Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives let you set out your story for Lincoln Educational Services, link that story to a forecast for revenue, earnings and margins, turn those assumptions into a Fair Value, and then compare it with the current share price to see whether you personally see room to buy or sell. All of this happens within Simply Wall St’s Community page, where Narratives are refreshed when new earnings or news arrive. One investor might build a Narrative that leans toward the analyst consensus Fair Value of US$44.80, while another might input more cautious or more optimistic assumptions for enrollment, margins or future P/E, leading to a very different Fair Value and a different decision on what to do next.

Do you think there's more to the story for Lincoln Educational Services? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.