Is Lululemon (LULU) Balancing Brand Strain With Business Strength Amid CEO Transition Delays?

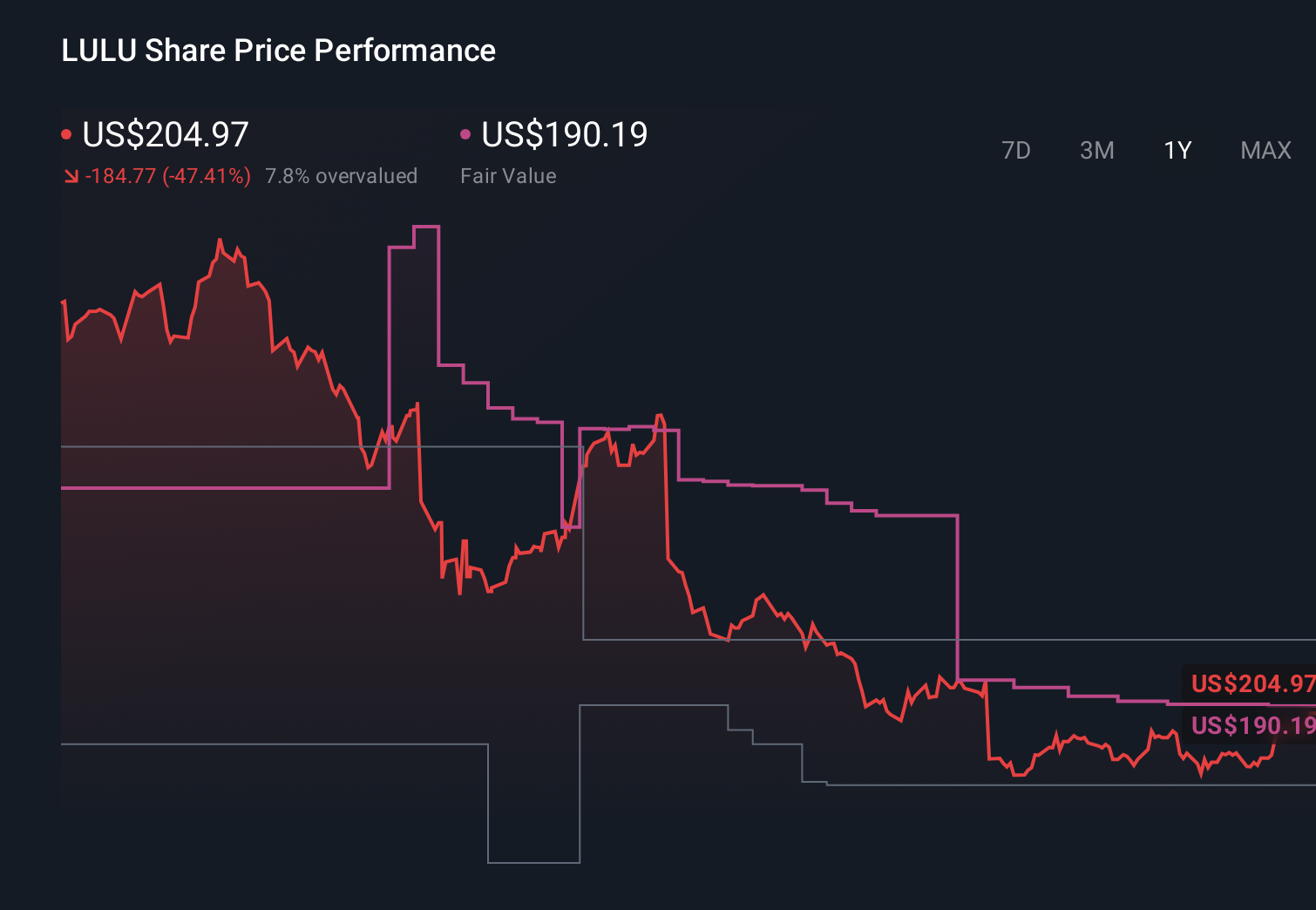

lululemon athletica inc. LULU | 0.00 |

- Lululemon athletica has recently endured leadership uncertainty from delays to incoming CEO Heidi O’Neill’s start date and reputational pressure following a culturally insensitive promotional event in China, compounding existing operational challenges.

- What stands out is that these setbacks are occurring while the company still maintains a strong operating model and growing store base, creating a tension between brand perception risks and underlying business strength.

- We’ll now explore how the CEO transition delays, alongside these reputational headwinds, may reshape Lululemon’s existing investment narrative.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

lululemon athletica Investment Narrative Recap

To own Lululemon today, you need to believe its product innovation, international expansion and margin profile can outlast near term brand and leadership noise. The CEO transition delay and the Great Wall backlash add uncertainty around brand perception, but they do not directly alter the core short term catalyst: whether new products and a reset assortment can re energize slowing North American demand. The biggest risk is that brand fatigue and softer U.S. trends deepen before that reset gains traction.

The most relevant recent development is the appointment of Heidi O’Neill as CEO, now pushed to September 2026, with interim co CEOs in place. This prolonged handover sits alongside activist driven board changes and cooperation with founder Chip Wilson, which together raise the stakes for execution on product, pricing and international growth. If governance changes support faster decisions and clearer accountability, they could help Lululemon respond more effectively to both the China controversy and its maturing core markets.

But despite these potential positives, investors should be aware of how prolonged brand pressure in China could still...

lululemon athletica's narrative projects $12.6 billion revenue and $1.6 billion earnings by 2029. This requires 4.3% yearly revenue growth and no change in earnings from $1.6 billion today.

Uncover how lululemon athletica's forecasts yield a $179.36 fair value, a 65% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already cautious, assuming revenue near US$10.9 billion and earnings around US$1.2 billion by 2029, and this new brand controversy plus CEO timing issues may reinforce that more pessimistic view compared with the more balanced baseline narrative, so it is worth thinking about which version of the story you find more realistic before you commit your own capital.

Explore 41 other fair value estimates on lululemon athletica - why the stock might be worth 28% less than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your lululemon athletica research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free lululemon athletica research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate lululemon athletica's overall financial health at a glance.

Want Some Alternatives?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Find 44 companies with promising cash flow potential yet trading below their fair value.

- We've uncovered the 7 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 29 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.