Is Lumentum Holdings (LITE) Pricing In Too Much After Recent Volatility?

Lumentum Holdings, Inc. LITE | 0.00 |

- If you are wondering whether Lumentum Holdings still offers good value after its recent strong performance, or if the price has already moved ahead of the underlying story, this article walks through what the current share price might be implying.

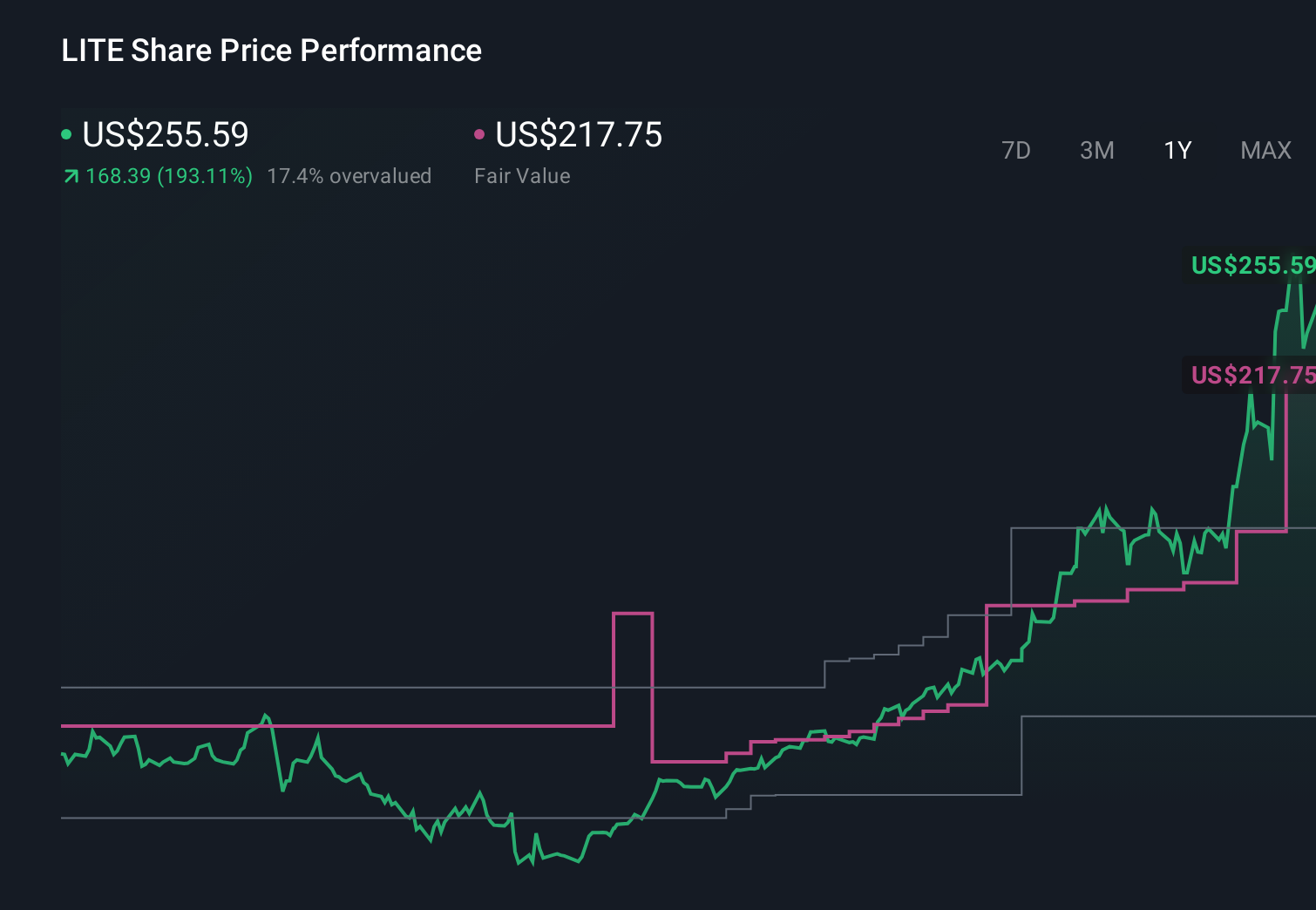

- The stock has pulled back recently, with a 5.5% decline over the last week and a 3.3% decline over the last month. It still shows a 9.8% decline year to date, alongside very large 1 year and multi year returns that may catch your eye.

- Recent coverage has focused on Lumentum's position in optical and photonics technology markets and how investors are reacting to that profile, which has attracted attention after the share price move. This context around sentiment and business focus helps frame why the stock has been so volatile recently.

- Lumentum currently has a valuation score of 0 out of 6. Next we will look at what different valuation methods say about the current price, and then consider a broader way to think about valuation that can add extra context to the numbers.

Lumentum Holdings scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

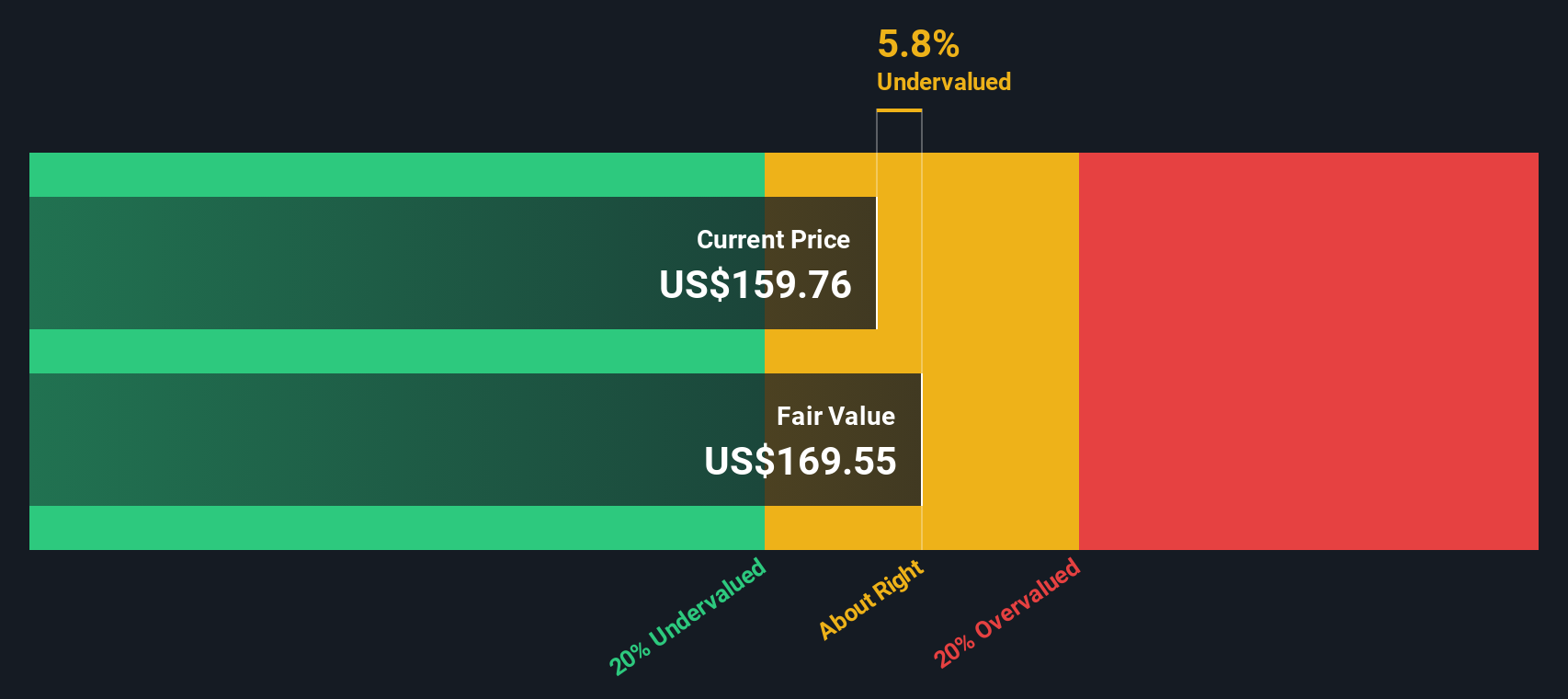

Approach 1: Lumentum Holdings Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes projected future cash flows and discounts them back to today to estimate what the entire business might be worth in dollars right now.

For Lumentum Holdings, the model used is a 2 stage Free Cash Flow to Equity approach. The latest twelve month free cash flow is a loss of about $64.1 million, so the model leans heavily on expectations for future free cash flow rather than current cash generation.

Analyst inputs and extrapolations point to free cash flow of $241.6 million in 2026 and $488.9 million in 2027, reaching $647.7 million by 2028, with further projected increases into the early 2030s. Simply Wall St extrapolates beyond the analyst horizon to build a ten year path of cash flows, then discounts each year back to today using its own assumptions.

On this basis, the DCF model arrives at an estimated intrinsic value of about $235.57 per share. Compared with the current share price, the implied intrinsic discount suggests the stock is about 47.8% overvalued according to this single framework.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Lumentum Holdings may be overvalued by 47.8%. Discover 878 undervalued stocks or create your own screener to find better value opportunities.

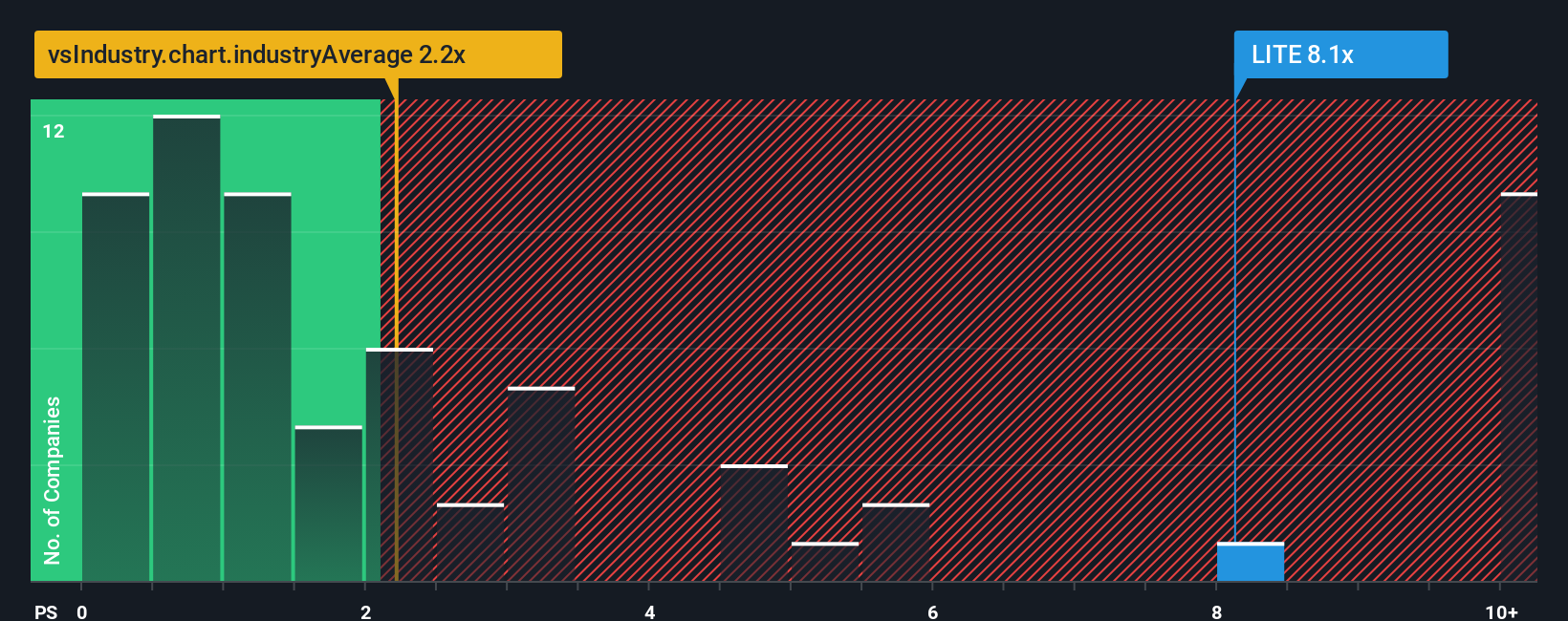

Approach 2: Lumentum Holdings Price vs Sales

For companies where profitability may be uneven or where earnings can be distorted, the P/S ratio is often a useful way to compare what investors are paying for each dollar of revenue. It sidesteps accounting swings in earnings and focuses on the top line instead.

In general, higher growth expectations or lower perceived risk can support a higher P/S multiple, while slower growth or higher risk usually line up with a lower multiple. Lumentum Holdings currently trades on a P/S of 13.41x. That sits well above the Communications industry average of 2.02x and also above the peer group average of 7.35x.

Simply Wall St’s Fair Ratio for Lumentum, at 5.48x, is its estimate of what a balanced P/S might look like once factors such as growth outlook, profit margins, industry, market cap and risk profile are taken into account. This makes it more tailored than a simple comparison with peers or the broader industry, which do not adjust for those company specific traits. With the current 13.41x P/S sitting meaningfully above the 5.48x Fair Ratio, the multiple implies the shares are pricing in a richer revenue valuation than this framework suggests.

Result: OVERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1443 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Lumentum Holdings Narrative

Earlier we mentioned that there is an even better way to understand valuation. On Simply Wall St you can use Narratives to connect your view of Lumentum Holdings' story with a set of revenue, earnings and margin forecasts, translate that into a Fair Value, then compare it with the current price to help you decide what action makes sense for you. All of this is within an easy tool on the Community page that updates automatically when new earnings or news arrive. For example, one investor might build a Narrative that leans into strong AI and cloud optics demand with a Fair Value near US$255 per share, while another focuses on customer concentration and margin risk and lands closer to US$83, and both can clearly see how their story, numbers and price line up.

Do you think there's more to the story for Lumentum Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.