Is LyondellBasell a Bargain After a 44% Drop in 2025?

LyondellBasell Industries NV LYB | 79.60 | +3.77% |

If you’re watching LyondellBasell Industries lately, you’re probably wondering if this is a chance to pick up a quality name at a bargain or if recent declines are a red flag. This is a moment when investors are really asking themselves what comes next. After all, the stock has slid by 2.2% in just the past week and is now down 44.7% over the last year. Even longer-term holders have felt the pain, with returns underwhelming over three and five year periods as well.

Many of these moves are connected to recent market jitters and industry-specific headlines, especially the growing debate around global demand for plastics and chemicals. Regulatory concerns, shifting environmental policies, and changing consumer habits are all factors investors have had to weigh. While LyondellBasell has navigated challenges before, the current environment has introduced a fresh layer of uncertainty. Some traders have started pricing in higher risks, yet others see growth potential if the company pivots or innovates.

Currently, with a value score of 2 out of 6 checks for undervaluation, LyondellBasell is not considered a clear undervalued pick, but it also does not sit at the high end of the market. That low score will raise some eyebrows, but it does not tell the whole story. Let’s dig into the major valuation approaches that shape this score, and stay tuned for a look at value that goes beyond simple checklists because there are additional factors to consider.

LyondellBasell Industries scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: LyondellBasell Industries Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model is a classic valuation tool that estimates a company's intrinsic value by projecting its future free cash flows and then discounting them back to today's dollars. This approach helps investors get an idea of what a business might truly be worth, beyond just the current stock price.

For LyondellBasell Industries, the model starts with a current Free Cash Flow (FCF) of $637 Million. While analyst estimates extend to 2027, projecting FCF to $1.82 Billion by the end of that year, subsequent projections out to 2035 are calculated by extrapolating expected growth trends. Over the coming decade, FCF is expected to rise consistently, eventually reaching more than $4.1 Billion in 2035, according to Simply Wall St's ongoing estimates.

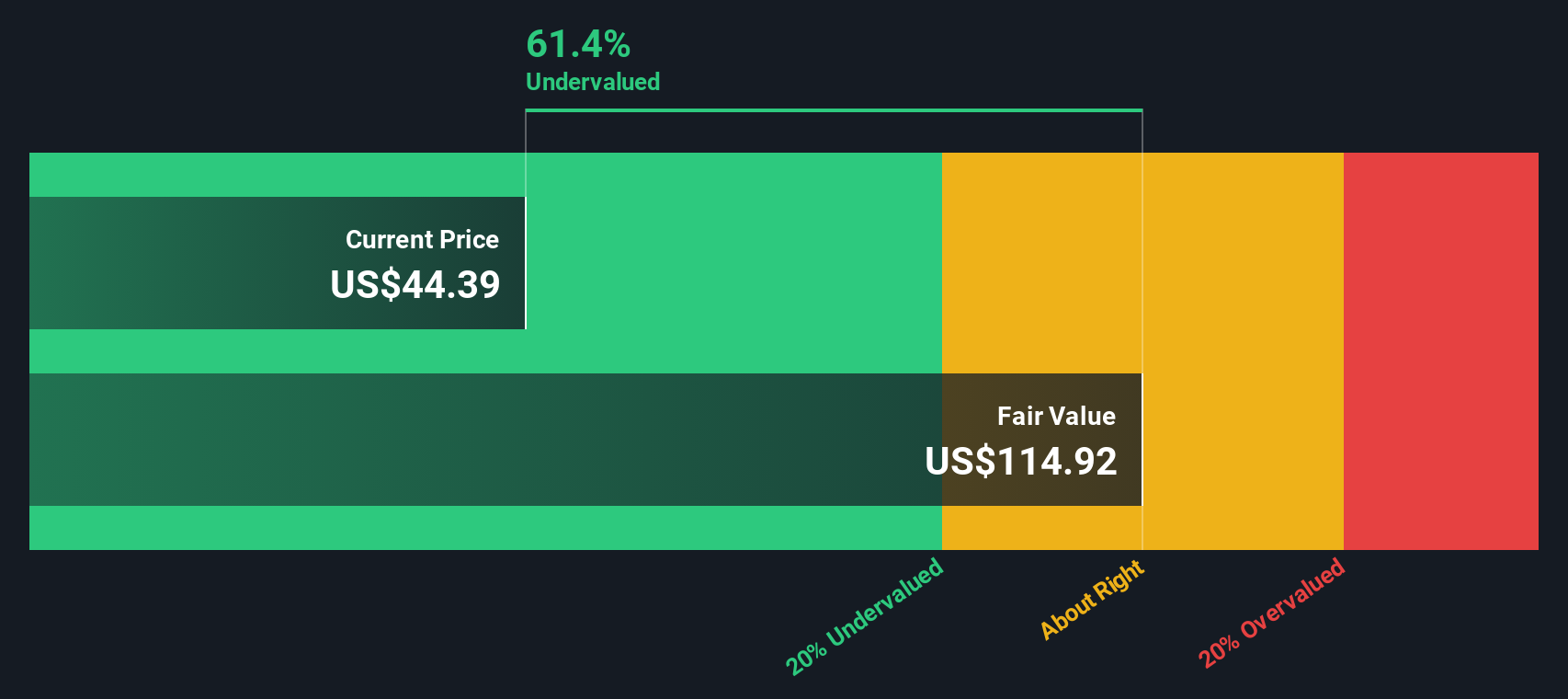

Pulling these future cash flows into today's terms, the DCF model concludes that LyondellBasell’s fair value stands at $144.23 per share. With the current price trading at a steep 68.4 percent discount to this calculated fair value, the model implies the stock is substantially undervalued relative to its future cash-generating potential.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests LyondellBasell Industries is undervalued by 68.4%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

Approach 2: LyondellBasell Industries Price vs Earnings

For companies that are profitable, the price-to-earnings (PE) ratio is often a preferred metric for assessing valuation. It quickly tells investors how much they are paying for each dollar of earnings, offering a practical way to compare companies across a sector. Growth expectations and risk both play a role in what a “normal” or “fair” PE ratio should be. A high-growth or low-risk company typically commands a higher multiple, while slower growth or greater risk means a lower one.

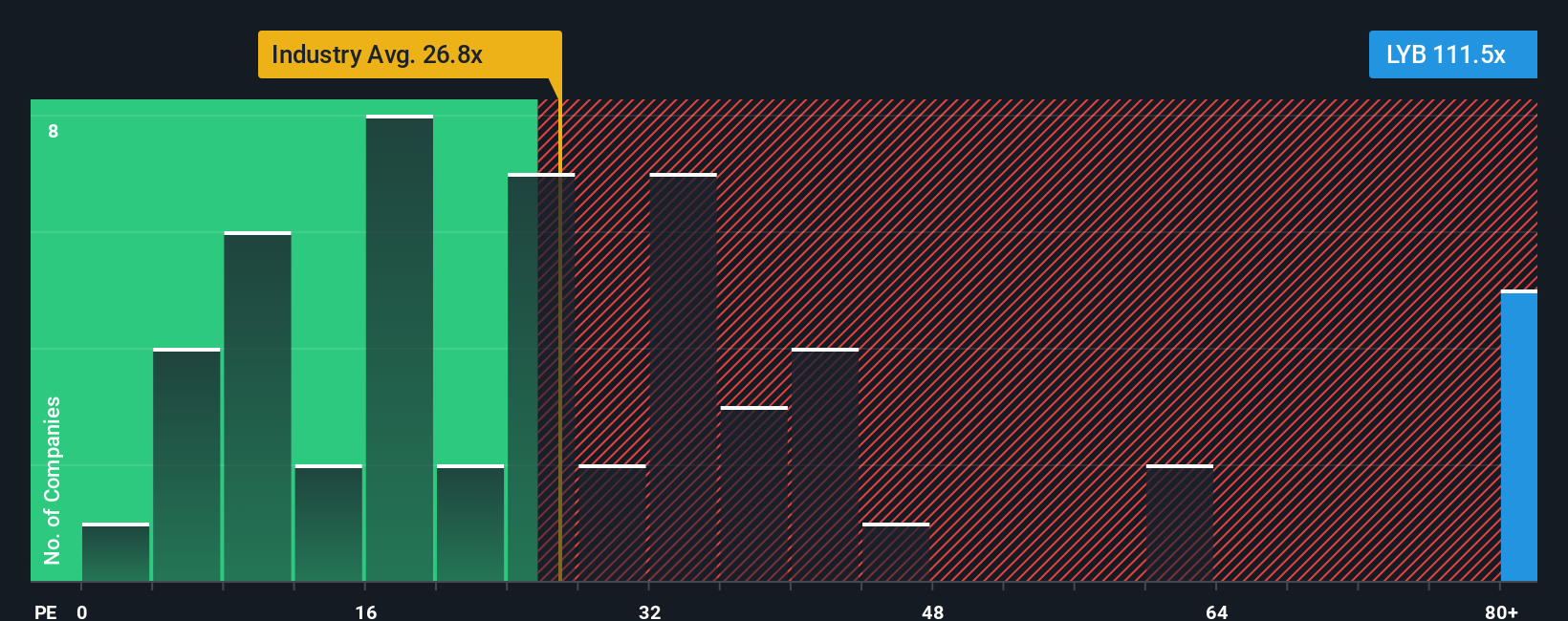

LyondellBasell Industries currently trades at a PE ratio of 97.82x, which stands out compared to the chemicals industry average of 26.29x and a peer average of 17.30x. On the surface, this suggests the stock may be richly valued relative to peers and the broader industry.

To address the nuances that simple comparisons can miss, Simply Wall St uses a proprietary “Fair Ratio.” This metric adjusts for factors like the company's earnings growth, profit margins, size, industry profile, and specific business risks. Because of this holistic view, the Fair Ratio (38.78x for LyondellBasell) often provides a more precise benchmark than just looking at peers or sector norms.

Comparing LyondellBasell’s actual PE ratio (97.82x) with its Fair Ratio (38.78x), the stock appears to be meaningfully overvalued according to this model.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your LyondellBasell Industries Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives. A Narrative is a straightforward, yet powerful, tool that allows you to tie your own story about a company, built from insights, assumptions, and expectations, directly to your forecasts for its revenue, earnings, and margins, leading to a specific fair value.

This means you can connect what you believe about LyondellBasell Industries’ industry position, growth prospects, or risks directly to a financial outcome, rather than relying solely on standard ratios or analyst targets. Available to millions of investors on Simply Wall St’s Community page, Narratives make it easy for anyone to turn their research and opinions into actionable, dynamic valuation models.

By comparing your Narrative-driven fair value with the current market price, you get a clear signal on when it might be time to buy or sell based on your unique perspective, not just market consensus. Narratives are also automatically refreshed as new earnings releases or major news impact the company's outlook, giving you an up-to-date framework for your decision making.

For example, one investor might set a high fair value for LyondellBasell based on confidence in its leadership in recycling technology and growth in low-cost regions. Another may have a much lower estimate if they foresee persistent regulatory headwinds and weak earnings ahead.

Do you think there's more to the story for LyondellBasell Industries? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.