Is Madison Investments’ Valuation-Driven Entry Altering The Investment Case For Moelis (MC)?

Moelis & Co. Class A MC | 0.00 |

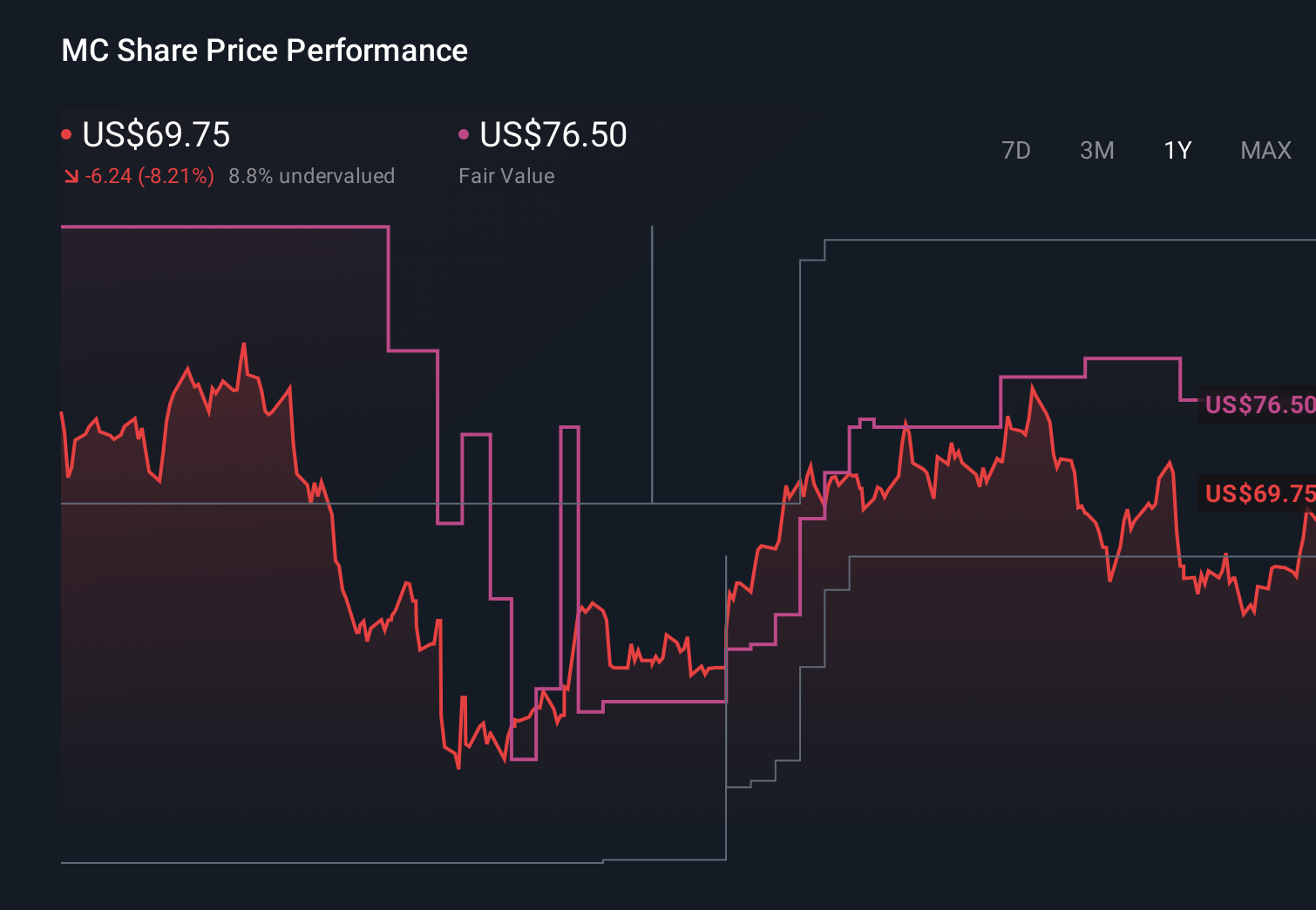

- In recent weeks, Madison Investments added Moelis & Company to its Madison Mid Cap Fund, citing an attractive valuation after the stock weakened amid concerns that private credit market conditions could weigh on M&A volumes.

- The move highlights how some institutional investors view Moelis as a high-quality, underappreciated advisory business positioned to benefit as market conditions and deal activity evolve.

- We’ll now explore how Madison Investments’ valuation-driven entry into Moelis shapes the firm’s existing investment narrative around expansion and earnings quality.

Uncover the next big thing with 21 elite penny stocks that balance risk and reward.

Moelis Investment Narrative Recap

To own Moelis, you need to believe in the long term relevance of independent advice in M&A and capital raising, despite cyclical swings in deal activity. The Madison Mid Cap Fund’s recent purchase after a pullback underlines that some investors see current pressure from private credit and softer M&A volumes as more sentiment than structural change. For now, this news does not materially alter the key near term catalyst, which is a sustained recovery in advisory activity, or the main risk of elevated cost pressure from ongoing expansion.

The company’s recent decision to authorize up to US$300,000,000 in additional share repurchases is particularly relevant here, as it intersects directly with the valuation debate highlighted by Madison’s entry. Buybacks have already retired more than 4,000,000 shares since 2019, and if advisory volumes improve, this capital return program could amplify any recovery in per share earnings. Conversely, if deal activity remains subdued, ongoing repurchases could sit uncomfortably alongside margin pressure and a softer earnings trajectory.

Yet beneath this apparently supportive backdrop, the concentration of revenues in inherently cyclical, transaction driven advisory work is something investors should be acutely aware of...

Moelis' narrative projects $2.4 billion revenue and $351.6 million earnings by 2029.

Uncover how Moelis' forecasts yield a $71.00 fair value, a 7% upside to its current price.

Exploring Other Perspectives

Some of the lowest rated analysts paint a far more cautious picture than the consensus, even before this news, assuming Moelis must earn about US$463,000,000 by 2029 to justify a lower US$58.00 target while facing structural threats from digital disintermediation and fee pressure, so it is worth comparing that view with the more optimistic expansion story and deciding which risk profile you are most comfortable with.

Explore 3 other fair value estimates on Moelis - why the stock might be worth just $71.00!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Moelis research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Moelis research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Moelis' overall financial health at a glance.

Want Some Alternatives?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.