Is Main Street Capital (MAIN) Undervalued Or Fairly Priced Today?

Main Street Capital Corporation MAIN | 0.00 |

Main Street Capital stock has delivered a strong 89.9% total return over the past five years, yet today its intrinsic value estimate from the Excess Returns model suggests around 25.6% upside from the current market price, while earnings based multiples look roughly in line with peers. That split leaves investors weighing a potential discount on the intrinsic value side against a more neutral read from traditional market multiples.

- Over five years, Main Street Capital has returned 89.9%, which puts recent share price weakness into a longer term context of solid compounding.

- The recent analysis highlighting a sizeable operating cost advantage and portfolio gains can support the intrinsic value case, while higher refinancing costs on US$500 million of debt may pressure earnings and limit how quickly any valuation gap closes.

- Main Street Capital scores 4 out of 6 on the broader valuation checks at this link, which points to a mixed picture rather than a clear bargain or clear overvaluation.

For investors, the debate is whether Main Street Capital's current price already reflects its cost advantages and income profile, or if the intrinsic value estimate signals a margin of safety that the market has yet to fully recognize.

Is Main Street Capital a Bargain on Excess Returns?

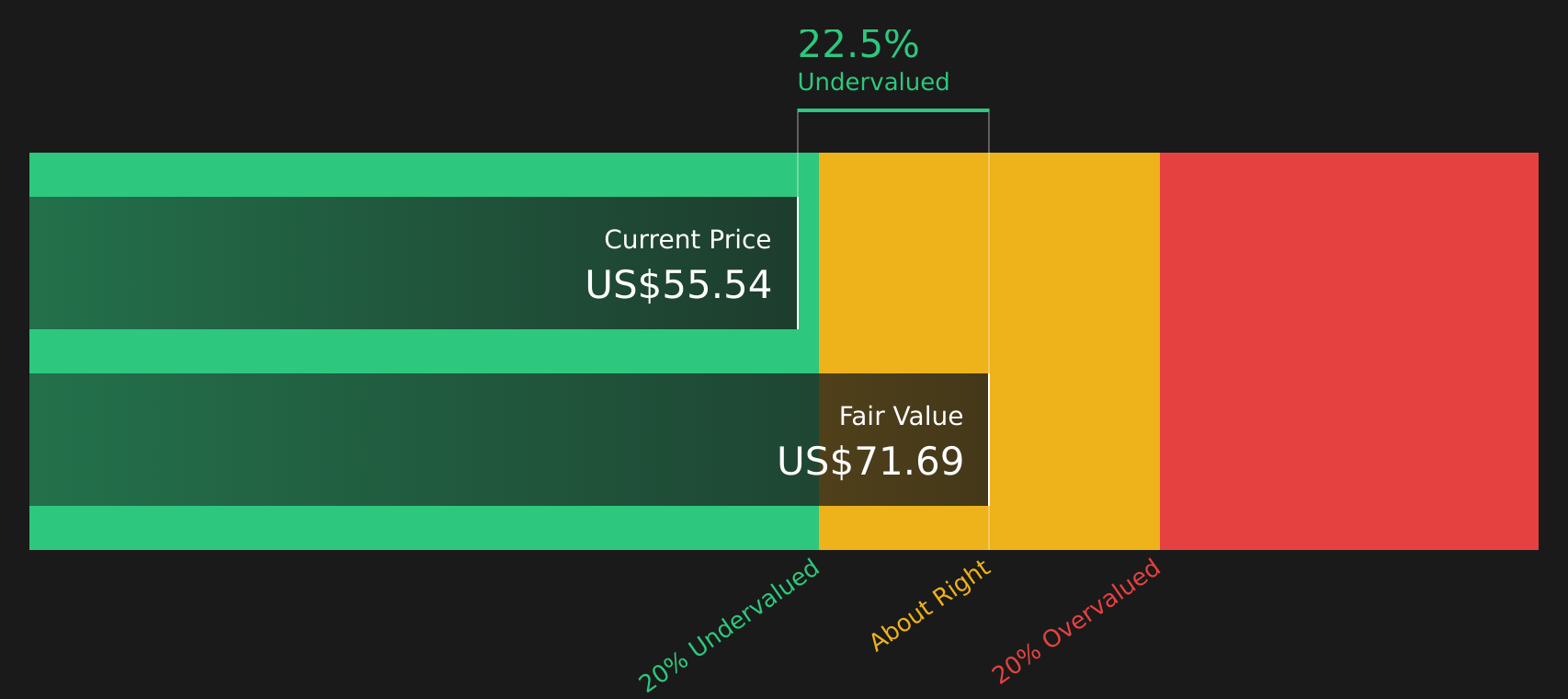

The Excess Returns model looks at how efficiently Main Street Capital turns its equity base into profits above the cost of capital. Here, the company is modeled with book value of $33.46 per share and stable EPS of $5.18 per share, implying an average return on equity of 16.94% versus a cost of equity of $2.83 per share. That gap produces excess return of $2.35 per share on a stable book value of $30.57 per share, which supports an intrinsic value estimate of about $71.79 per share.

Set against the current share price, that implies the stock screens around 25.6% undervalued. The Excess Returns framework points to a business still earning returns on equity above its modeled cost of capital, even after building in more conservative long run assumptions. The recent focus on refinancing US$500 million of low cost debt at higher rates helps explain why the price may sit below this intrinsic value estimate, as investors weigh higher interest expense against the company’s return profile.

On this Excess Returns view, Main Street Capital stock currently looks undervalued relative to the cash returns it is modeled to generate on its equity base.

Our Excess Returns analysis suggests Main Street Capital is undervalued by 25.6%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Is Main Street Capital Fairly Priced on Earnings?

The P/E multiple fits Main Street Capital because many investors focus on its earnings and dividend stream. Main Street Capital currently trades on a P/E of about 11.7x, compared with an industry average around 40.0x and a peer average near 18.4x in the wider capital markets group.

The model based fair P/E for Main Street Capital is about 10.9x, which is close to where the stock sits today. This suggests the market price is broadly aligned with the company’s earnings profile once factors like size, risk and profitability are taken into account. While the headline gap to the higher industry multiple might catch the eye, that sector figure includes businesses with very different business models and risk profiles, so the more tailored fair ratio is a clearer yardstick here.

On the P/E lens, Main Street Capital stock currently looks roughly fairly valued relative to what the model suggests investors might typically pay for these earnings.

The Main Street Capital Narrative: What Would Justify Today's Price?

For Main Street Capital, Simply Wall St Narratives pick up where this valuation split leaves off by spelling out which paths for growth, margins and earnings would make the stock worth materially more or less than today’s price. Each narrative ties its conclusion to a clear view on how Main Street Capital's growth, profitability and risks might evolve, giving you something specific to revisit as fresh information comes through on the Community page.

If you have a number driven view on whether Main Street Capital's cost advantage and rising refinancing costs ultimately support today's price, add your Narrative on the Community page and set out the case in your own words. It is a chance to be one of the first voices in the Simply Wall St community to put a clear thesis on Main Street Capital and see how it holds up as new results and portfolio updates come through.

Do you think there's more to the story for Main Street Capital? Head over to our Community to see what others are saying!

The Bottom Line

For Main Street Capital, the Excess Returns intrinsic value estimate points to meaningful upside, while the P/E work suggests the stock is priced close to what investors typically pay for its earnings profile. That split reflects how the intrinsic view leans on the company’s ability to keep earning solid returns on equity after refinancing, while the multiple view is more about how the market rates its growth and risk next to peers. With broader valuation checks looking mixed, the key question now is whether Main Street Capital’s cost advantage and income profile are strong enough to justify a higher valuation, or if the current discount is justified by funding pressures.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.