Is MannKind (MNKD) Now An Opportunity After A 39% Year To Date Share Price Decline?

MannKind Corporation MNKD | 0.00 |

- If you are wondering whether MannKind at around US$3.40 is a bargain or a value trap, the key question is how its current price compares with what the business might be worth.

- The stock has had a weak run recently, with the share price down about 9.8% over the last week, 3.4% over the past month, and 39.3% year to date, contributing to a 22.4% decline over the last year and a 16.0% fall over five years.

- Recent coverage has focused on MannKind's position within the broader Biotechs industry and how ongoing product and pipeline developments are shaping sentiment. This helps explain why the stock has been under pressure. This context is important because news around approvals, partnerships, or financing often shifts how investors view both risk and potential for companies in this space.

- In that context, MannKind currently scores 5 out of 6 on Simply Wall St's valuation checks, as shown by its valuation score. The next step is to break down what different valuation approaches say about the stock today and then look at an even deeper way to think about value at the end of this article.

Approach 1: MannKind Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth by projecting the company’s future cash flows and discounting them back to today using a required rate of return. It focuses on the cash the business might return to shareholders over time, not just current earnings.

For MannKind, the model used is a 2 Stage Free Cash Flow to Equity framework built on free cash flow projections. The latest twelve month free cash flow is a loss of about $1.27 million. Looking ahead, analysts and extrapolated estimates point to free cash flow of $42 million in 2026, rising through the projection period to $80 million by 2030, with additional estimated figures extending out to 2035 in the tens of millions of dollars each year.

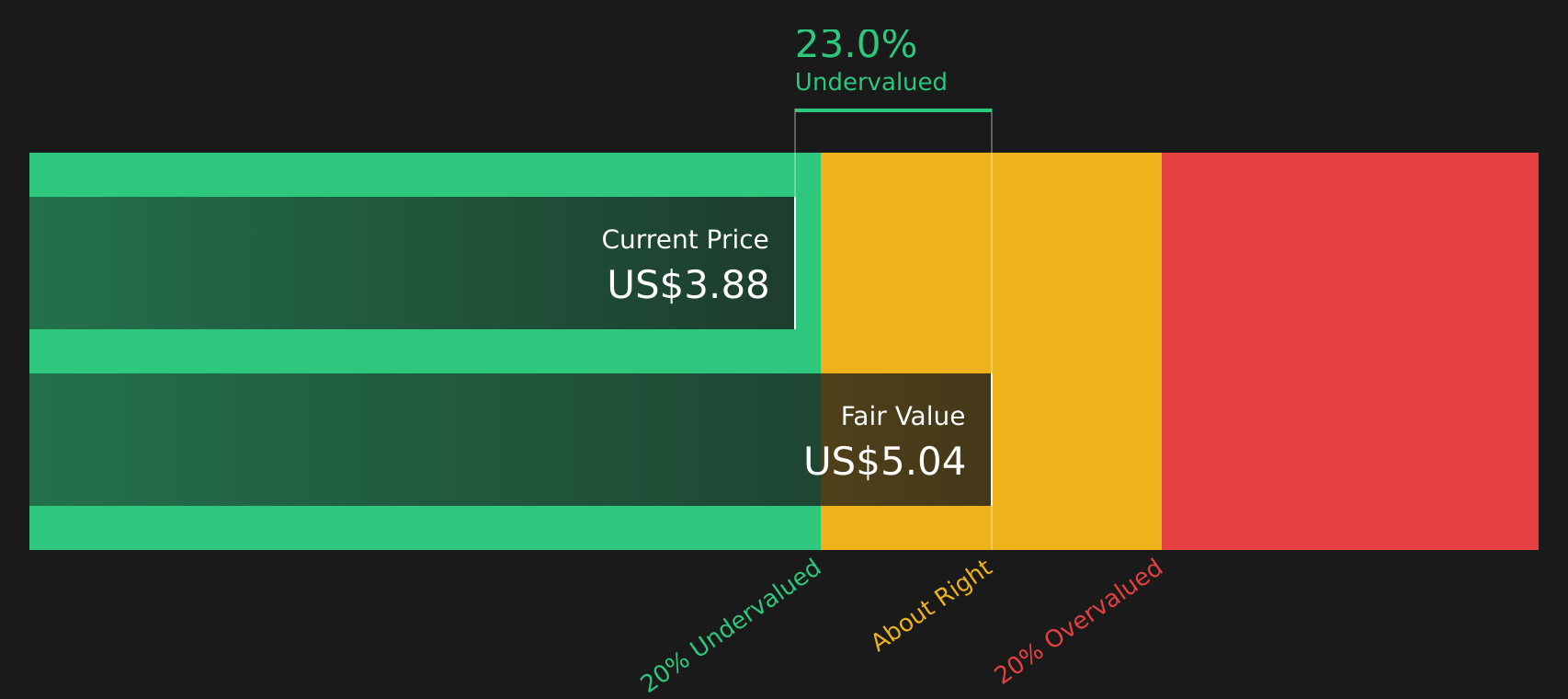

When these projected cash flows are discounted back, Simply Wall St’s model arrives at an estimated intrinsic value of about $4.83 per share. Compared with the recent share price of around $3.40, this implies MannKind trades at roughly a 29.6% discount. On this DCF view, the stock appears to be undervalued.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests MannKind is undervalued by 29.6%. Track this in your watchlist or portfolio, or discover 49 more high quality undervalued stocks.

Approach 2: MannKind Price vs Sales

For companies in biotechs where earnings can be volatile or losses are common, the P/S ratio is often more useful than P/E or P/B because it compares the stock price with current revenue rather than accounting profits or book value.

What counts as a “normal” P/S ratio usually reflects how quickly revenue is expected to grow and how risky the business is. Higher growth and lower perceived risk can justify a higher multiple, while slower growth or higher risk tend to support a lower one.

MannKind currently trades on a P/S of about 2.91x. This sits below the wider Biotechs industry average P/S of around 10.05x and also below the peer group average of roughly 4.09x. Simply Wall St’s Fair Ratio for MannKind is 4.75x, which represents the P/S level suggested by its model based on factors such as earnings growth, margins, industry, market cap and risk profile.

Because the Fair Ratio adjusts for these company specific factors, it can be more informative than a simple comparison with industry or peer averages. With MannKind’s actual P/S ratio of 2.91x sitting below the Fair Ratio of 4.75x, this approach points to the stock trading at a discount.

Result: UNDERVALUED

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Upgrade Your Decision Making: Choose your MannKind Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives put a story behind the numbers by letting you connect your view on MannKind’s future revenue, earnings and margins to a forecast and a Fair Value. You can then compare that Fair Value to the current price to help you decide whether to act, and see that view update automatically on Simply Wall St’s Community page as new news or earnings arrive. Whether you lean toward a higher Fair Value of about US$11.00 with revenue reaching US$649.6 million and earnings of US$168.9 million by 2029, or a lower Fair Value of about US$4.75 with revenue at US$447.0 million and earnings of US$4.7 million by 2029, Narratives help you connect these scenarios to your decision making process.

Do you think there's more to the story for MannKind? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.