Is Marathon Petroleum (MPC) Still Attractively Priced After Its Strong 2024 Share Price Rally

Marathon Petroleum Corporation MPC | 0.00 |

- Wondering whether Marathon Petroleum at US$251.99 still offers value, or if most of the upside is already in the price? This article walks through what the current share price could be implying.

- The stock has been strong over multiple periods, with a decline of 3.3% over the last week, a 13.2% gain over the last month, a 52.6% return year to date and a 58.1% return over the past year. The three year return sits at 150.1%, and the five year return is a very large gain.

- Recent coverage has focused on Marathon Petroleum's position among US refiners and the broader energy sector, including how investors weigh refining margins, capital returns and investment plans against the current share price. This context helps explain why sentiment around the stock can shift quickly even without company specific announcements dominating the headlines.

- Marathon Petroleum currently scores 3 out of 6 on Simply Wall St's valuation checks. The next sections compare different valuation approaches, and later circle back to an even deeper way of thinking about what the stock might be worth.

Approach 1: Marathon Petroleum Discounted Cash Flow (DCF) Analysis

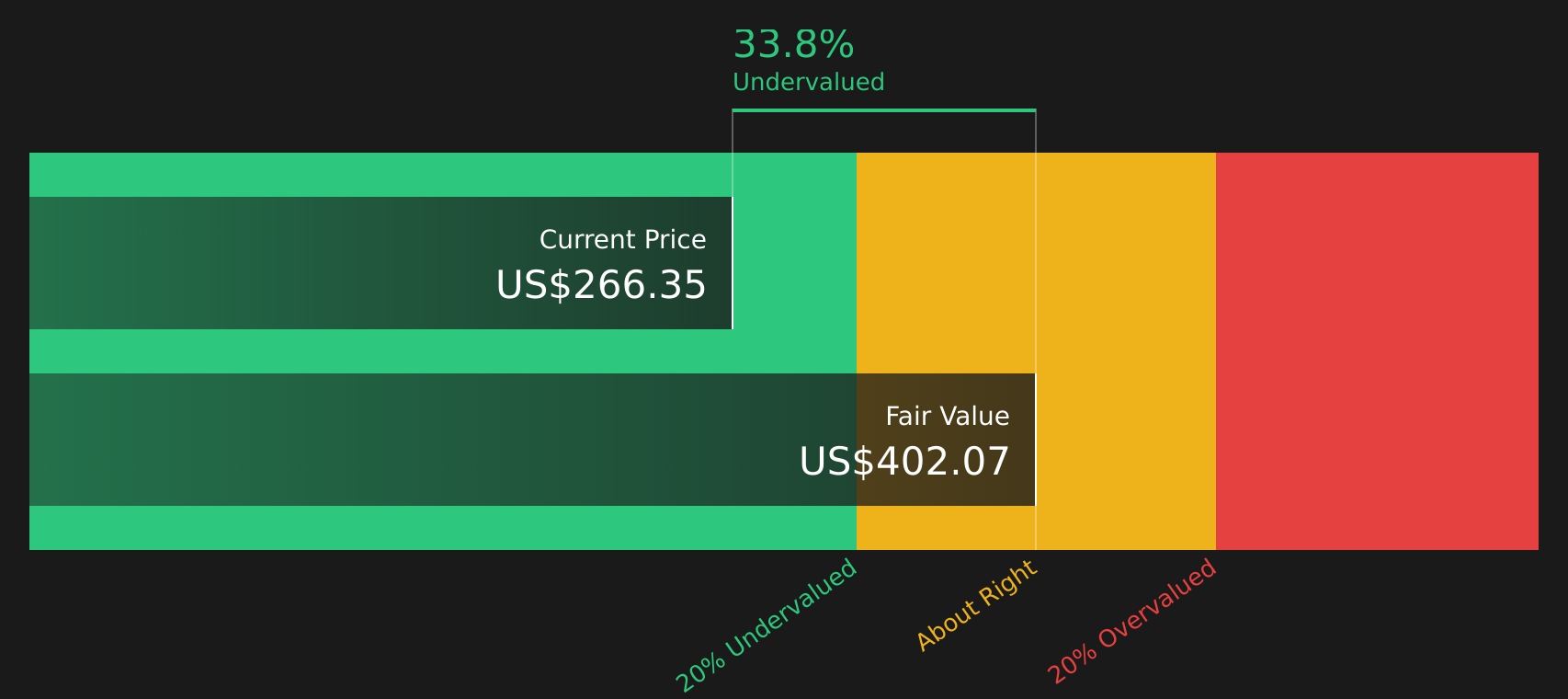

A Discounted Cash Flow model projects a company’s future cash flows and then discounts them back to today’s value to estimate what the business could be worth right now.

For Marathon Petroleum, the model uses a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month Free Cash Flow is about $6.7b. Analysts provide forecasts out to 2030, with Simply Wall St extrapolating further. The ten year projections show Free Cash Flow assumptions generally in the $5.2b to $8.8b range, with 2030 set at $5.9b. All of these future figures are discounted back to today in dollars using the DCF framework.

Adding up those discounted cash flows gives an estimated intrinsic value of about $425.89 per share, compared with the current share price of $251.99. That implies the stock trades at roughly a 40.8% discount to this DCF estimate, which points to the shares looking undervalued on this model.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Marathon Petroleum is undervalued by 40.8%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

Approach 2: Marathon Petroleum Price vs Earnings

P/E is a common way to look at profitable companies because it links what you pay for the stock to what the company is currently earning per share. Investors usually accept a higher or lower P/E depending on what they expect for future earnings and how much risk they see in the business, so there is no single “right” P/E that fits every stock.

Marathon Petroleum trades on a P/E of 15.90x, compared with the Oil and Gas industry average of about 14.44x and a peer average of 15.67x. Simply Wall St also calculates a proprietary “Fair Ratio” of 21.77x for Marathon Petroleum. This Fair Ratio reflects factors such as earnings growth expectations, the company’s industry, profit margins, market cap and risk profile.

Because the Fair Ratio is tailored to Marathon Petroleum, it can be more informative than a simple comparison to broad industry or peer averages that may mix companies with very different growth and risk profiles. With the Fair Ratio of 21.77x sitting above the current P/E of 15.90x, the stock screens as undervalued on this multiple based approach.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Marathon Petroleum Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives bring this to life by letting you attach a clear story about Marathon Petroleum to specific assumptions for future revenue, earnings and margins, then connect that story to a Fair Value you can compare with today’s price.

On Simply Wall St’s Community page, Narratives are an easy tool used by millions of investors to spell out how they see the company, link that view to a forecast and Fair Value, and then see in one place whether the stock looks expensive or cheap versus that Fair Value. This can help you decide if it might be a buy, a sell or a hold for your portfolio.

Because Narratives update when fresh information arrives, such as new buyback announcements or analyst targets, your view stays current rather than frozen in time. You can also see how other investors differ, for example with one Marathon Petroleum Narrative anchoring on a Fair Value around US$318.81 and a more cautious one closer to US$163.00, both built from very different assumptions about future earnings, margins and P/E.

For Marathon Petroleum, here are previews of two leading Marathon Petroleum Narratives:

Fair value in this bullish Narrative framework: US$256.83 per share.

At the last close of US$251.99, the price sits about 1.9% below this Narrative fair value.

Revenue growth assumption in this view: revenue is expected to decline about 4.8% a year.

- Focuses on strong product demand, tight refining capacity and portfolio moves in refining and midstream as the key drivers of earnings and cash flows.

- Assumes profit margins rise from 3.4% to 4.3% over three years and that share buybacks steadily reduce the share count, supporting earnings per share.

- Anchors on analyst consensus expectations, with a fair value close to US$256.83 and a future P/E of about 13.6x, while highlighting environmental and energy transition risks that could challenge the thesis.

Fair value in this bearish Narrative framework: US$163.00 per share.

At the last close of US$251.99, the price sits about 54.5% above this Narrative fair value.

Revenue growth assumption in this view: revenue is expected to decline about 2.2% a year.

- Highlights the risk that recent refining projects and sour crude exposure do not fully pay off if product markets loosen or crude differentials move against the company.

- Builds in falling margins and earnings by 2029 and assumes only modest benefit from share count reduction, pointing to lower long term profitability than the bullish camp expects.

- Arrives at a fair value of US$163.00, implying a large gap to the current price if weaker demand, midstream project underperformance and tighter cash generation play out.

Together, these Narratives bracket a range of possible futures for Marathon Petroleum. The bullish view leans on resilient product demand, disciplined capital returns and margin support, while the bearish view leans on softer utilization, thinner spreads and less supportive midstream economics. Using them side by side helps you stress test your own expectations and decide where your assumptions sit within that spectrum.

Do you think there's more to the story for Marathon Petroleum? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.