Is McCormick Ready for a Comeback After a 12% Slide in 2025?

McCormick & Company, Incorporated MKC | 48.38 47.80 | -4.08% -1.21% Pre |

If you’ve been watching McCormick, you’ve probably noticed it hasn't been the market's favorite flavor lately. After starting this year with some optimism, the stock has slipped by about 12% over the last twelve months, with a small rally in the past 30 days offering a glimmer of hope. At last close, shares stood at $66.85, down nearly 12% year-over-year and still showing a double-digit dip since January. These moves have prompted a lot of investors to ask the same question: is it time to spice up your portfolio with McCormick, or should you look elsewhere?

Part of the recent pressure on the stock ties back to mixed news throughout the packaged foods sector, including reports of rising input costs and shifting consumer preferences. Although McCormick faces long-term trends affecting grocery demand, recent headlines have highlighted the company's steady commitment to expanding its product lines and exploring new markets. Some of these strategic moves have captured analyst attention, hinting at growth potential even if the broader industry faces some headwinds.

Given all this, valuation is top of mind for many, especially since McCormick holds a value score of 2 out of 6 based on standard undervaluation checks. That’s not exactly a bargain rating, but it isn’t sky-high either. So, how does McCormick stack up when it comes to traditional valuation metrics, and is there a smarter way to weigh the opportunity here? Let’s break down the numbers using a few key valuation approaches, then explore one method that might offer even deeper insight.

McCormick scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: McCormick Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a stock’s intrinsic value by projecting its future cash flows and then discounting those projections back to today’s dollars. This approach is widely used to assess whether a company’s share price reflects its true long-term financial potential.

For McCormick, the latest reported Free Cash Flow stands at $617.8 million, serving as the base for future growth assumptions. Analysts have modeled the company’s cash flow out over several years, with projections from Simply Wall St indicating Free Cash Flow could climb to $1.15 billion by 2028 and potentially approach $1.6 billion per year by 2035. These growth rates reflect steady expansion over the next decade. Beyond 2028, forecasting relies more on extrapolation than on concrete analyst estimates.

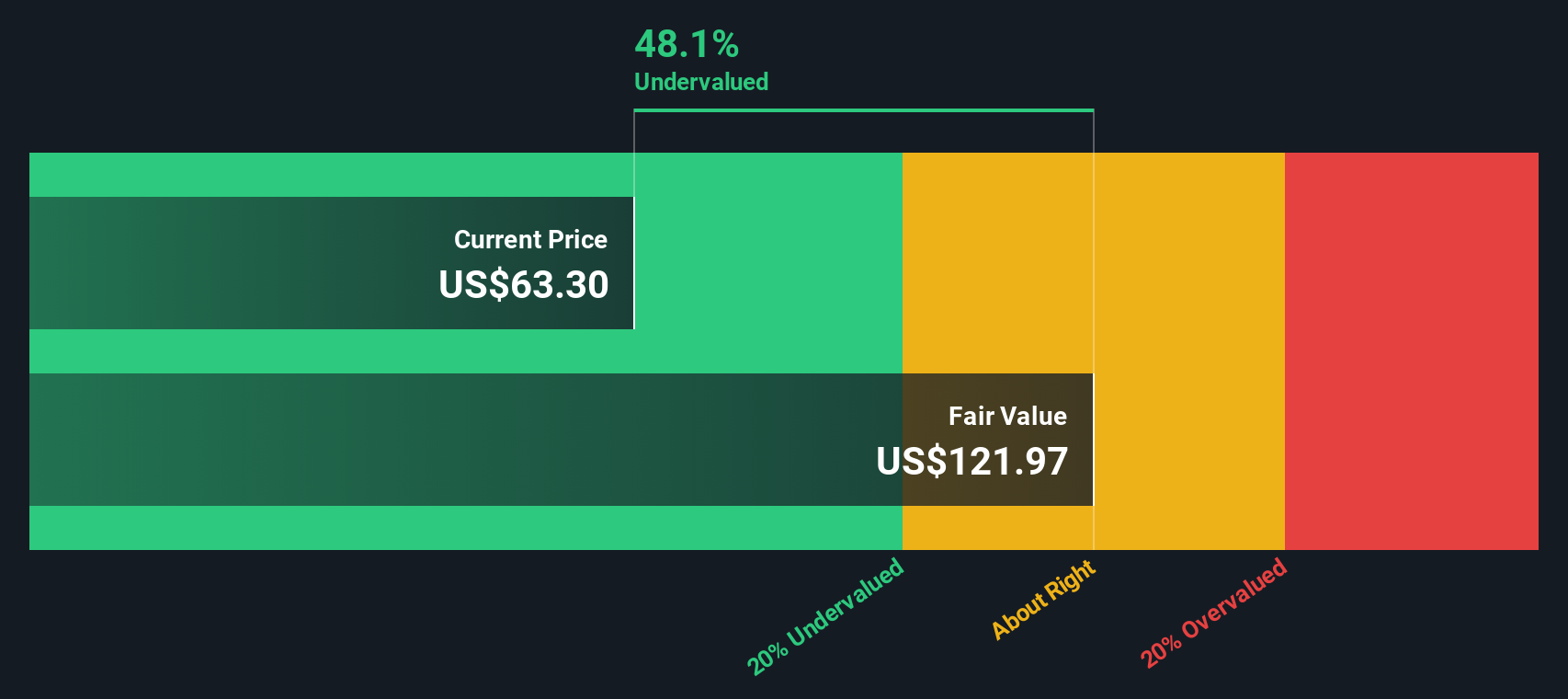

Considering these factors, the DCF model suggests an intrinsic fair value of $122.78 per share. With shares currently trading at $66.85, McCormick appears to be trading at a 45.6% discount to its calculated intrinsic value, suggesting significant undervaluation according to this model.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests McCormick is undervalued by 45.6%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

Approach 2: McCormick Price vs Earnings

Another popular way to assess whether a profitable company like McCormick is fairly valued is by using the Price-to-Earnings (PE) ratio. The PE ratio offers a quick snapshot of how much investors are willing to pay for each dollar of current earnings, making it especially relevant for established, consistently profitable companies.

However, it's important to remember that what counts as a "normal" PE ratio depends on various factors, including a company's expected earnings growth and the perceived risks in its business model. Companies with stronger growth prospects often justify a higher PE, while those with greater risk or slower growth tend to trade at lower multiples.

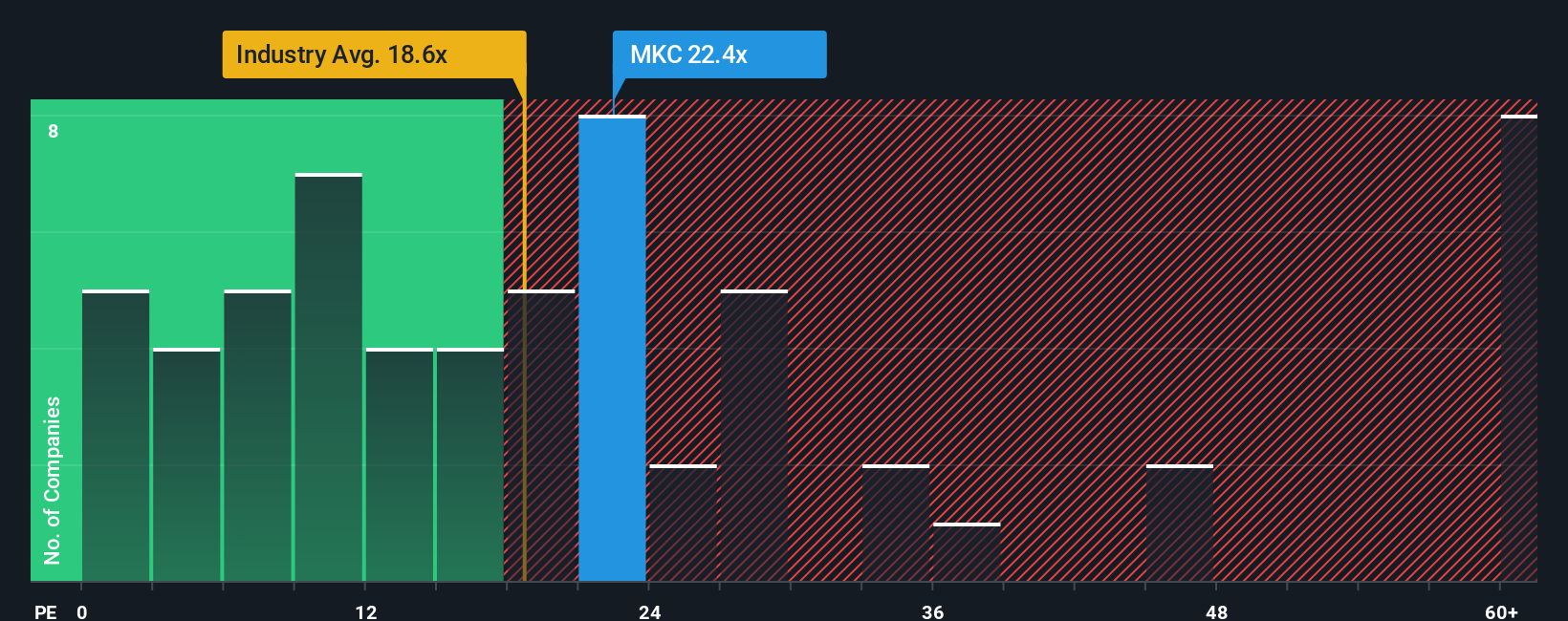

McCormick currently trades at a PE ratio of 23.1x. This is notably higher than the Food industry average of 18.4x and ahead of the peer average, which sits at 13.9x. At first glance, McCormick seems a bit pricey relative to these benchmarks.

This is where Simply Wall St's proprietary “Fair Ratio” comes in. The Fair Ratio, currently set at 18.6x for McCormick, suggests a PE multiple that reflects the company's unique mix of earnings growth, industry position, profit margins, market size, and risk profile. Unlike the blunt tool of straight peer or industry comparisons, the Fair Ratio customizes expectations based on what really drives value for the business.

Comparing McCormick’s actual PE ratio (23.1x) to its Fair Ratio (18.6x), the stock appears to be trading above its optimal level. This points to McCormick being somewhat overvalued according to this metric.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your McCormick Narrative

Earlier we mentioned that there’s an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative lets you define your own view of McCormick by combining your perspective on the story behind the numbers with your assumptions for future sales, earnings, and profit margins.

Simply put, Narratives connect what you believe about the business with a clear financial forecast and an estimated fair value, so you can see how your view compares with market prices. Narratives are easy to use and available right on Simply Wall St’s platform within the Community page, helping millions of investors create, compare, and update their investment ideas in real time.

By building your own Narrative, you can check if McCormick’s price today is above or below what you think it’s worth, which can make a Buy or Sell decision much clearer. As new data, news, or earnings emerge, Narratives update automatically, keeping your view current and actionable.

For example, when analysts set their highest McCormick price target at $102 and the lowest at $67, these reflect different Narratives. One expects robust global expansion and margin gains, while the other sees continued cost and competition risks. Your Narrative and fair value might fall anywhere between, based on your unique outlook.

Do you think there's more to the story for McCormick? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.