Is McDonald's (MCD) Stock Pricing In Long Term Strength After Recent Share Price Weakness

McDonald's Corporation MCD | 0.00 |

- If you are wondering whether McDonald's stock is priced for long term strength or if you are simply paying up for a famous brand, this article walks through key signals that can help you judge value for yourself.

- The stock last closed at US$280.92, with returns roughly flat over 7 days at 0.2%, down 3.2% over 30 days and down 7.4% year to date, while the 1 year return is down 8.1% and the 3 and 5 year returns are 5.6% and 33.9% respectively.

- Recent headlines around McDonald's have focused on its role as a global consumer services giant and how its scale and brand recognition position it in a highly competitive quick service restaurant industry. These themes help frame how investors think about both the risks and the potential resilience that could sit behind recent price moves.

- Simply Wall St currently gives McDonald's a value score of 2 out of 6, based on how many valuation checks suggest the stock may be undervalued. Next up is a closer look at those methods, followed by an even broader way of thinking about what fair value really means for this company.

McDonald's scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

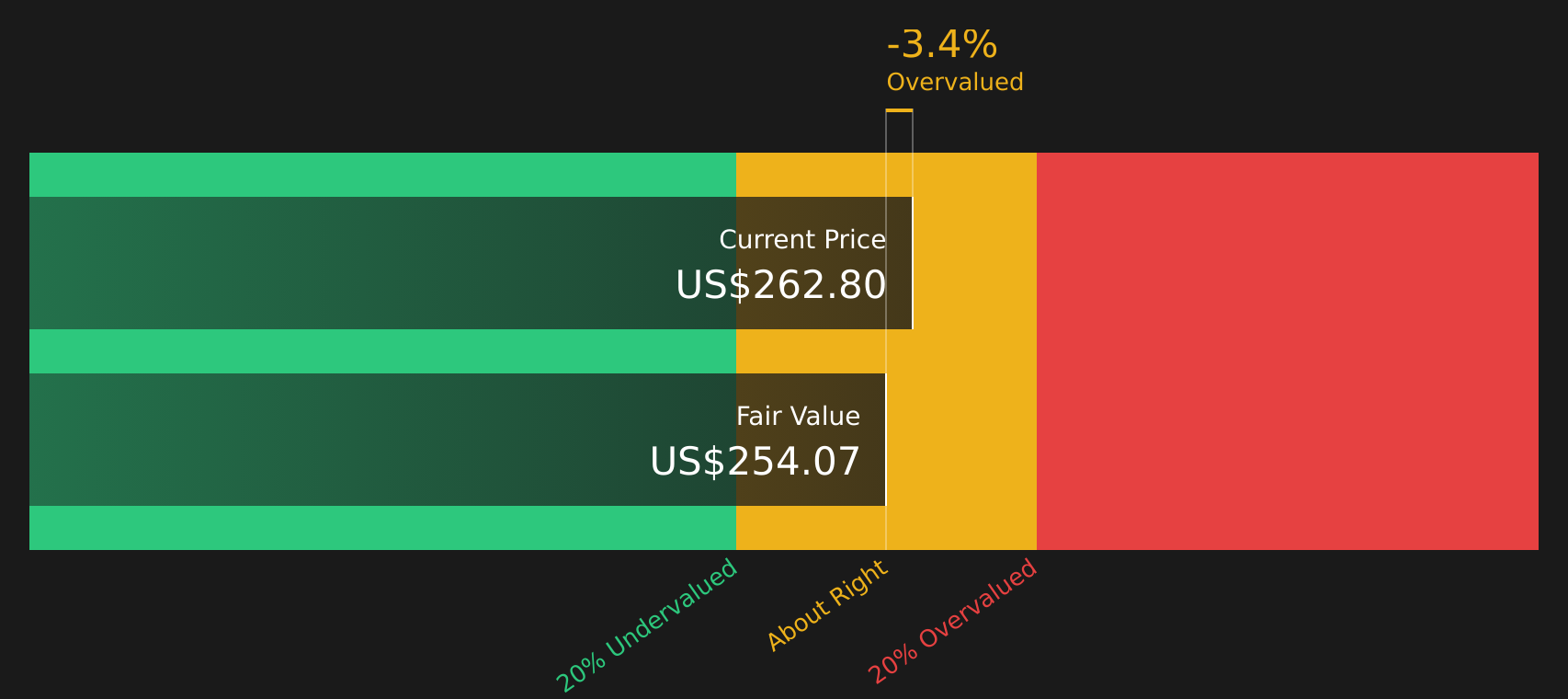

Approach 1: McDonald's Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth by projecting the cash the business may generate in the future and then discounting those cash flows back to today. It is essentially asking what McDonald's future cash generation is worth in today's dollars.

For McDonald's, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flow projections. The latest twelve month free cash flow is about $7.52b. Analyst estimates and Simply Wall St extrapolations suggest projected free cash flows rising to around $13.63b by 2035, with interim projections such as $9.68b for 2028 included in the model. All cash flows are assessed in dollars and discounted back to present value.

On this basis, the DCF model arrives at an estimated intrinsic value of about $250.66 per share, compared with the recent share price of $280.92. That gap implies the stock is about 12.1% above the DCF estimate, which points to a market price that is richer than this particular cash flow model would suggest.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests McDonald's may be overvalued by 12.1%. Discover 47 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: McDonald's Price vs Earnings

For a profitable company like McDonald's, the P/E ratio is a useful way to think about what you are paying for each dollar of earnings. It ties the share price directly to current earnings, which is usually the anchor for how many investors think about value.

What counts as a “normal” or “fair” P/E ratio tends to reflect how fast earnings are expected to grow and how risky those earnings are perceived to be. Higher expected growth or lower perceived risk can justify a higher multiple, while slower growth or higher risk usually points to a lower one.

McDonald's currently trades on a P/E of 23.00x. That sits above the Hospitality industry average of about 20.08x and below the broader peer group average of 51.23x. Simply Wall St also calculates a “Fair Ratio” of 31.08x for McDonald's, which is the P/E that might be reasonable given factors like its earnings profile, industry, profit margins, market cap and key risks. This Fair Ratio can be more tailored than a simple comparison to peers or the industry because it considers company specific characteristics rather than broad group averages. With the current P/E at 23.00x versus a Fair Ratio of 31.08x, McDonald's stock screens as trading below that Fair Ratio.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your McDonald's Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Think of Narratives as your way to attach a clear story about McDonald's to the numbers you see, linking a view on its future revenue, earnings and margins to a financial forecast and then to a fair value that can be compared with the current share price.

On Simply Wall St's Community page, Narratives are an easy tool that investors use to set their own assumptions and fair value, then see at a glance whether that fair value sits above or below the current price, which can help decide whether the stock looks attractive or stretched on those specific assumptions.

Because Narratives update when new information such as earnings reports, analyst targets or news is added to the platform, you can keep a live view of how your thesis stacks up against the latest numbers and other investors' views.

For McDonald's, one investor might build a Narrative that lines up with the higher analyst fair value around US$330.0 based on expectations for revenue, margins and a P/E of 28.3x by 2029. Another might key off a lower fair value around US$238.97 that comes from more cautious DCF and multiple based assumptions. Narratives let you see and compare both stories in one place.

For McDonald's, however, we will make it really easy for you with previews of two leading McDonald's Narratives:

Start by asking which story feels closer to how you see the business, then compare that story's fair value with the current share price of US$280.92.

Fair value in this bullish Narrative: US$330.00 per share

Gap to this fair value: the current price sits about 15% below this Narrative's fair value estimate

Revenue growth assumption: 5.23% a year

- Focuses on expansion in emerging markets, digital ordering, loyalty programs and menu refreshes as drivers of higher guest counts and long term revenue growth, especially outside the U.S.

- Assumes efficiency gains from technology and an asset light franchise model help support profit margins around 33.0% and earnings of US$10.6b by 2029.

- Anchors the view on an analyst consensus fair value of US$330.00, with a future P/E of 28.3x, and encourages you to sense check those assumptions against your own expectations for revenue, margins and risk.

Fair value in this cautious Narrative: US$238.97 per share

Gap to this fair value: the current price sits about 18% above this Narrative's fair value estimate

Revenue growth assumption: 4.86% a year

- Highlights that while McDonald's has high historical returns on invested capital and a wide economic moat, projected revenue and EPS growth are moderate and tied to a mature business profile.

- Blends several methods, including DCF, EPS growth, historical P/E, EV/EBITDA, P/S, dividend models and yield history, many of which point to the stock trading above the levels suggested by long term averages and cash flow based estimates.

- Frames a weighted fair value of US$238.97 and suggests a personal buying zone below that level, while stressing that any fair value is an estimate and depends heavily on the assumptions you use.

Whichever Narrative feels closer to your own view, the key step is to check whether your expectations for McDonald's revenue growth, margins and valuation multiple look closer to the bullish or the cautious case, then decide how comfortable you are with the current price sitting between those two fair values.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for McDonald's on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for McDonald's? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.