Is Microchip (MCHP) Quietly Repositioning Its Edge AI Moat With Post‑Quantum Automotive Controllers?

Microchip Technology Incorporated MCHP | 0.00 |

- In April 2026, Microchip Technology expanded its reach and product capabilities through new distribution, manufacturing and collaboration agreements, alongside launching its dsPIC33AK256MPS306 Digital Signal Controllers featuring post-quantum cryptography for automotive, industrial, data center and AI server applications.

- Together, these moves strengthen Microchip’s role in secure, high-reliability embedded systems across automotive ADAS, defense and aerospace, and intelligent power and motor control, potentially making its ecosystem more attractive to OEMs and developers that prioritize long-term supply assurance and certified design tools.

- We’ll now examine how Microchip’s post-quantum-ready dsPIC33AK256MPS306 launch may influence its investment narrative built around edge AI and automotive.

We've uncovered the 11 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Microchip Technology Investment Narrative Recap

To own Microchip today, you need to believe its embedded control portfolio can convert recovering demand in automotive, industrial and data center into sustainably higher margins despite high leverage and past revenue declines. The recent post quantum dsPIC33AK256MPS306 launch and new distribution and manufacturing agreements support the edge AI and secure embedded narrative, but they do not clearly change the key near term swing factors of inventory normalization and factory utilization.

Among the recent announcements, the Sunny Smartlead collaboration around ASA ML based ADAS camera modules feels most relevant. It reinforces Microchip’s attempt to deepen its role in software defined vehicles right as automotive recovery and content per vehicle are central to the bull case. If ASA ML gains traction, it could complement the dsPIC33AK256MPS306 in cars that need secure sensor fusion, although execution and customer adoption remain open questions.

Yet against this opportunity, investors should be aware that prolonged high inventory and underutilized fabs could still...

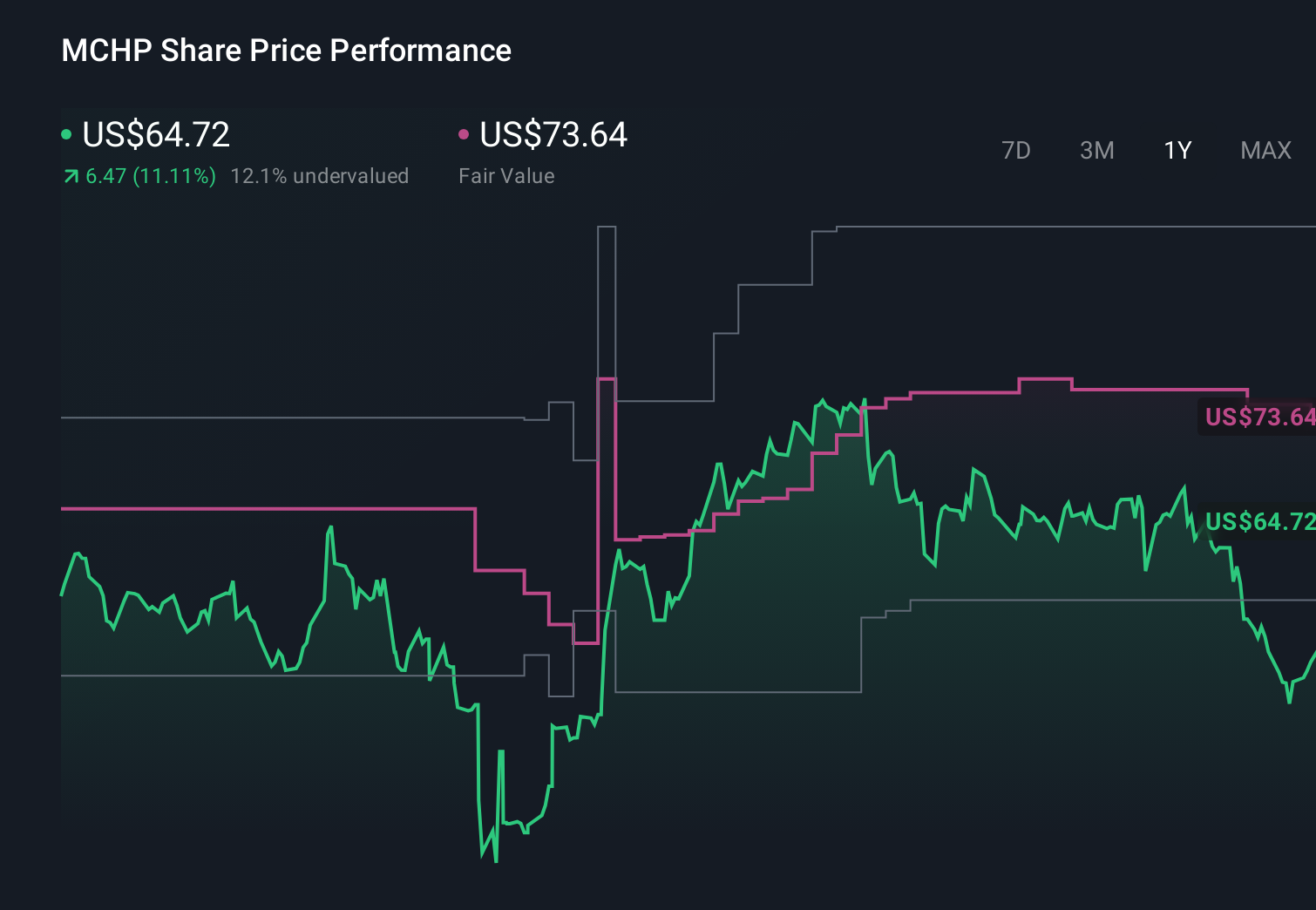

Microchip Technology's narrative projects $7.3 billion revenue and $1.9 billion earnings by 2029.

Uncover how Microchip Technology's forecasts yield a $86.67 fair value, a 13% upside to its current price.

Exploring Other Perspectives

While the baseline view focuses on gradual recovery and inventory risk, the most optimistic analysts were already assuming roughly US$8.4 billion of revenue and about US$2.1 billion of earnings by 2028, so this kind of product and ecosystem news could either reinforce or challenge those high expectations depending on how you think competitive and regulatory pressures ultimately play out.

Explore 5 other fair value estimates on Microchip Technology - why the stock might be worth as much as 42% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Microchip Technology research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

- Our free Microchip Technology research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Microchip Technology's overall financial health at a glance.

Want Some Alternatives?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

- AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Find 58 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.