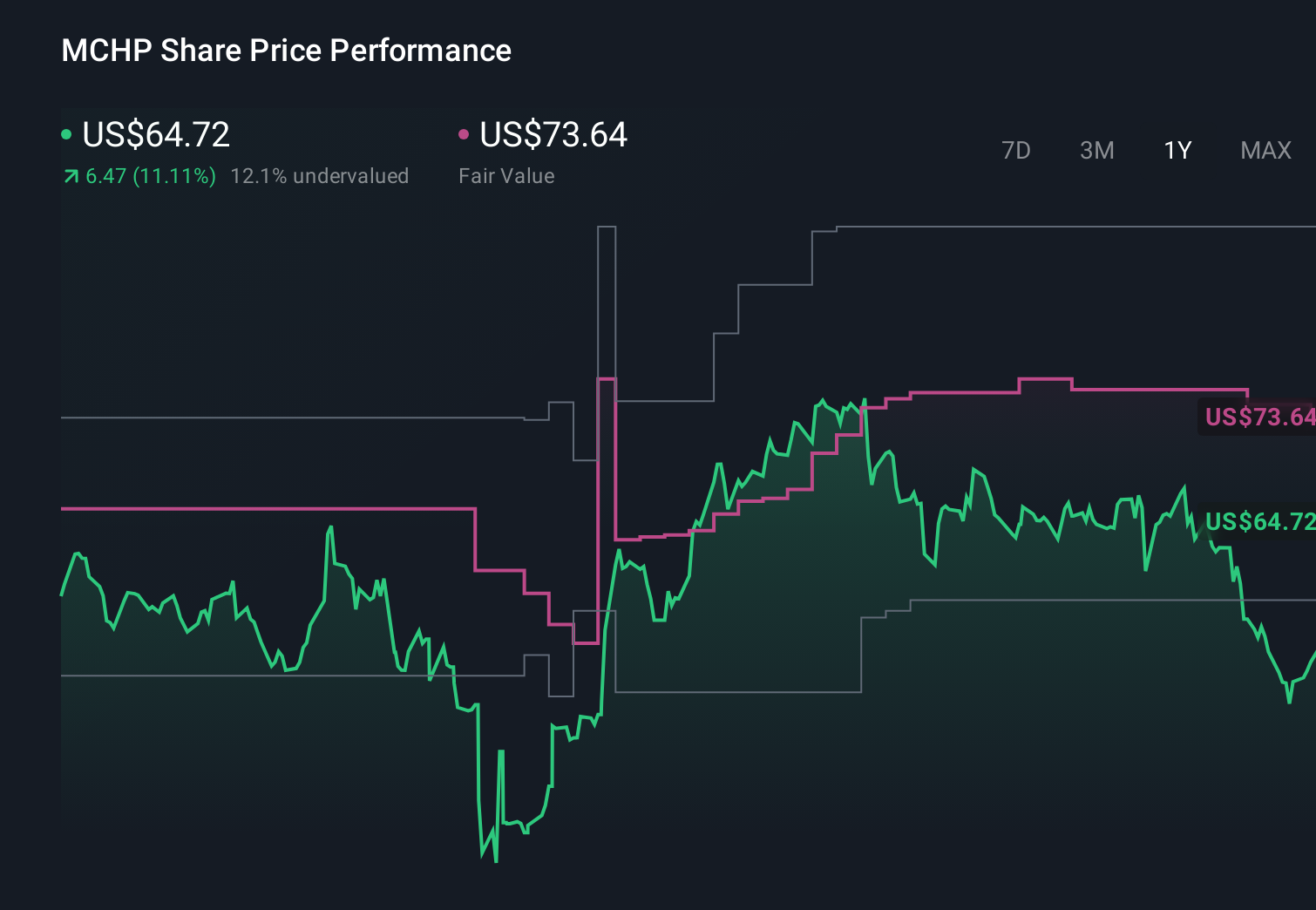

Is Microchip Technology’s (MCHP) New AI Retimers Quietly Reframing Its Core Infrastructure Narrative?

Microchip Technology Incorporated MCHP | 0.00 |

- In recent days, Microchip Technology announced U.S. export-license approval for advanced FPGA development in Armenia, alongside new AI-focused PCIe 6.0 and CXL 3.1 retimers and 3.3 kV SiC power modules aimed at data-center and high-voltage applications. These developments expand Microchip’s role in AI infrastructure and global engineering while adding cost-focused dsPIC33CK controllers and a new independent board member.

- Together, the export-license clearance and AI/data-center product launches highlight Microchip’s push deeper into critical cloud, power and embedded control technologies that underpin modern computing and industrial systems.

- We’ll now examine how Microchip’s new AI infrastructure retimers and related updates may influence its existing investment narrative and outlook.

This technology could replace computers: discover 30 stocks that are working to make quantum computing a reality.

Microchip Technology Investment Narrative Recap

To own Microchip, you need to believe its embedded, analog and FPGA portfolio can convert AI, data center and industrial demand into improving margins while it works down elevated inventories and sizable debt. The Armenia export license and new AI power and connectivity products support that thesis but do not, on their own, resolve near term risks around inventory normalization, interest costs and whether recent data center strength can offset softer areas like automotive.

Among the recent announcements, the XpressConnect PCIe 6.0 and CXL 3.1 retimers look most relevant, because they sit at the heart of AI data center build outs and tie directly to Microchip’s Data Center Solutions unit, which delivered US$302.7 million in 2025 revenue. How effectively this portfolio scales, and at what margin, could be an important counterweight to inventory and leverage concerns if end market demand stays supportive.

But while the AI data center story is appealing, investors should also be aware that...

Microchip Technology's narrative projects $7.3 billion revenue and $1.9 billion earnings by 2029. This requires 18.5% yearly revenue growth and about a $2.1 billion earnings increase from -$154.4 million today.

Uncover how Microchip Technology's forecasts yield a $86.67 fair value, in line with its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already modeling revenue of about US$8.1 billion and earnings near US$2.3 billion by 2029, so when you weigh this new AI and export control news against their expectations about tougher geopolitics and regulation, it highlights how differently you and other investors might view Microchip’s future and why it is worth comparing several narratives before deciding what you believe.

Explore 5 other fair value estimates on Microchip Technology - why the stock might be worth as much as 53% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Microchip Technology research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Microchip Technology research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Microchip Technology's overall financial health at a glance.

No Opportunity In Microchip Technology?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Find 49 companies with promising cash flow potential yet trading below their fair value.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 13 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.