Is Mueller Industries (MLI) A Bargain Following Its Stock Split And Record Q1?

Mueller Industries, Inc. MLI | 0.00 |

Mueller Industries (MLI) has drawn fresh attention after a 2-for-1 stock split took effect on July 1, following record Q1 results, strong cash reserves, and a balance sheet reported with no debt.

The stock split and index removal came after a strong run, with the 1 year total shareholder return at 38.19% and the 5 year total shareholder return approaching 5x. This comes even as the 30 day share price return has declined 14.77% and short term momentum has cooled.

If Mueller Industries has your attention after its split and long run of value creation, this can be a good moment to broaden your search with the 35 power grid technology and infrastructure stocks

After a sharp multi year run, a recent 15% pullback, and signals that some valuation models see Mueller Industries as trading above intrinsic value, the key question now is whether there is still a buying opportunity or whether markets are already pricing in future growth.

Price-to-Earnings of 14.8x: Is it justified?

Even after a long run, Mueller Industries is trading on a P/E of 14.8x, which screens as good value relative to the broader US market and its Machinery peers.

The P/E multiple compares the current share price to the company’s earnings and is a quick way to see how much investors are paying for each dollar of profit. For a manufacturer like Mueller Industries, with a long operating history and established end markets in piping systems, industrial metals, and climate products, this is a commonly used benchmark.

Recent data shows earnings growth of 35.8% over the past year and 13.5% per year over the past 5 years, with current net profit margins at 19.4% compared with 15.9% last year. Against that backdrop, the stock’s P/E of 14.8x sits below the US market average of 19.2x and below the US Machinery industry average of 27.9x, which suggests investors are paying less for each dollar of Mueller Industries earnings than they are for many peers.

On top of that, the estimated fair P/E of 24.5x is well above the current 14.8x. This implies a level the market could move toward if sentiment and earnings expectations align more closely with that fair ratio.

Result: Price-to-Earnings of 14.8x (UNDERVALUED)

However, Mueller Industries still faces risks if revenue growth of 8.5% and net income growth of 6.5% slow, or if recent share price weakness deepens.

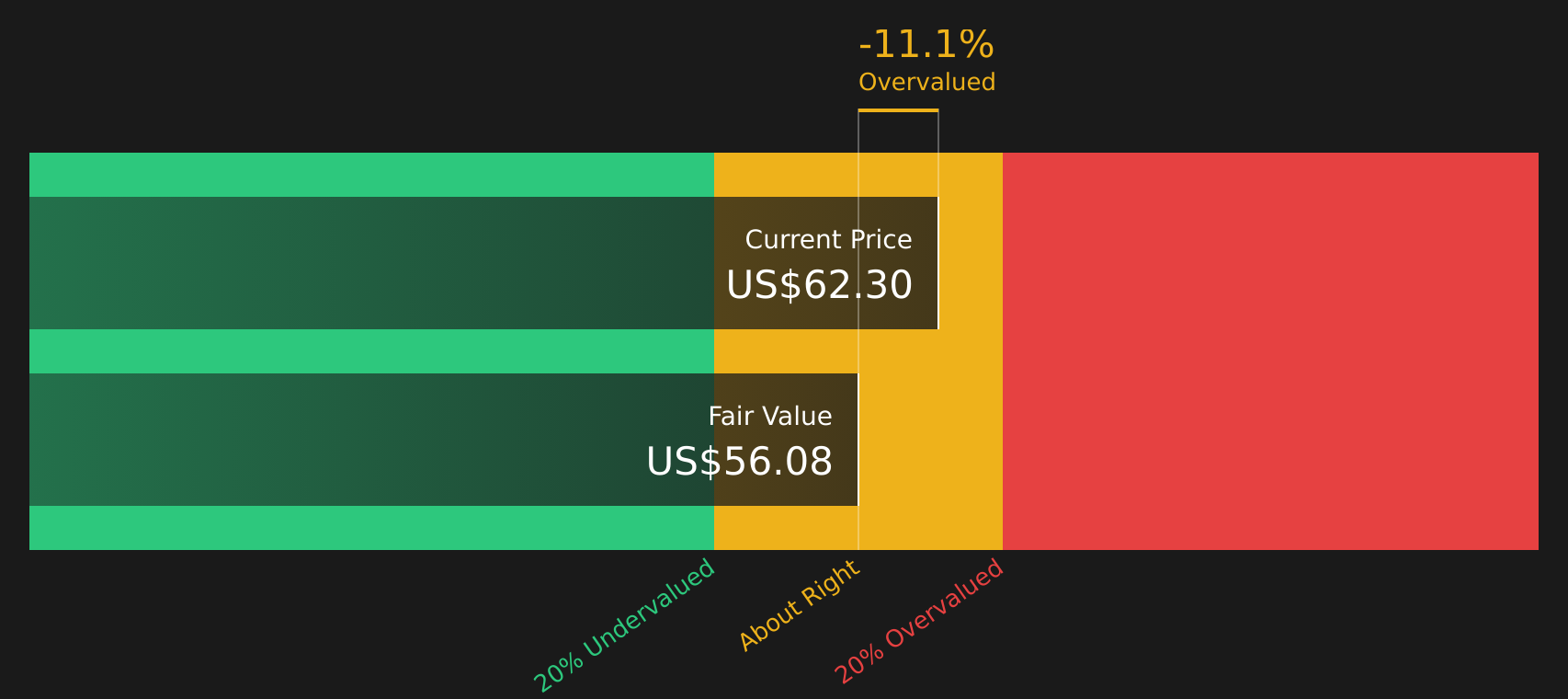

Another View: What the SWS DCF Model Says About Mueller Industries

While the P/E comparison points to good value for Mueller Industries, the SWS DCF model comes out slightly differently. With the stock at $56.50 and the model’s future cash flow value at $55.57, this approach suggests the shares are modestly overvalued rather than cheap. For you as an investor, that kind of narrow gap raises a practical question: is there enough margin of safety here, or are expectations already baked in?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Mueller Industries for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With a mixed picture around valuation and recent price moves, it helps to move quickly from headlines to hard data. Take a closer look at the balance of potential upside and downside by reviewing the 4 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Mueller Industries?

If Mueller Industries has sharpened your focus on quality and valuation, do not stop here. The next strong opportunity for your portfolio could be one step away.

- Target opportunities with both value and resilience by checking out the 44 high quality undervalued stocks.

- Strengthen your income stream by reviewing the 7 dividend fortresses.

- Protect your downside potential by scanning the 74 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.