Is Netflix’s Warner Bros. Break Fee And Governance Shift Altering The Investment Case For Netflix (NFLX)?

Netflix NFLX | 0.00 |

- On 5 June 2026, Netflix reported the results of its 4 June annual shareholder meeting, where all four shareholder proposals on ESG ROI reporting, written consent rights, cumulative voting, and politicized brand misalignment were rejected, while the board confirmed Jay Hoag as chairman following Reed Hastings’ departure.

- At the same time, Netflix’s decision to walk away from a Warner Bros. Discovery acquisition, collect a US$2.80 billion break fee, and lean into its growing ad-supported tier and multi-format “Attention OS” underscores a focus on organic growth, capital returns, and refined governance rather than large-scale M&A.

- We’ll now examine how stepping back from the Warner Bros. Discovery deal while securing a multi-billion-dollar break fee influences Netflix’s investment narrative.

Outshine the giants: these 13 early-stage AI stocks could fund your retirement.

Netflix Investment Narrative Recap

To own Netflix, you need to believe it can keep converting its global audience and growing “Attention OS” into durable, multi-stream cash flows, even as streaming matures and competition bites. The key short term catalyst remains execution in ads and broader engagement monetization, while the biggest risk is that rising content and customer acquisition costs outpace that monetization. The Warner Bros. Discovery break fee and AGM outcomes do not materially change that near term equation.

The most relevant recent development here is Netflix’s decision to exit the Warner Bros. Discovery deal and collect a US$2.80 billion break fee. That one off gain, alongside an enlarged US$55,000 million buyback authorization and ongoing ad tier traction, reinforces a capital return and organic growth story rather than a consolidation one, which matters directly for how investors think about near term earnings quality, per share metrics, and the durability of the current catalyst set.

Yet, beneath this cleaner story, investors should still be alert to the growing risk that intensifying competition and content spending could eventually outpace...

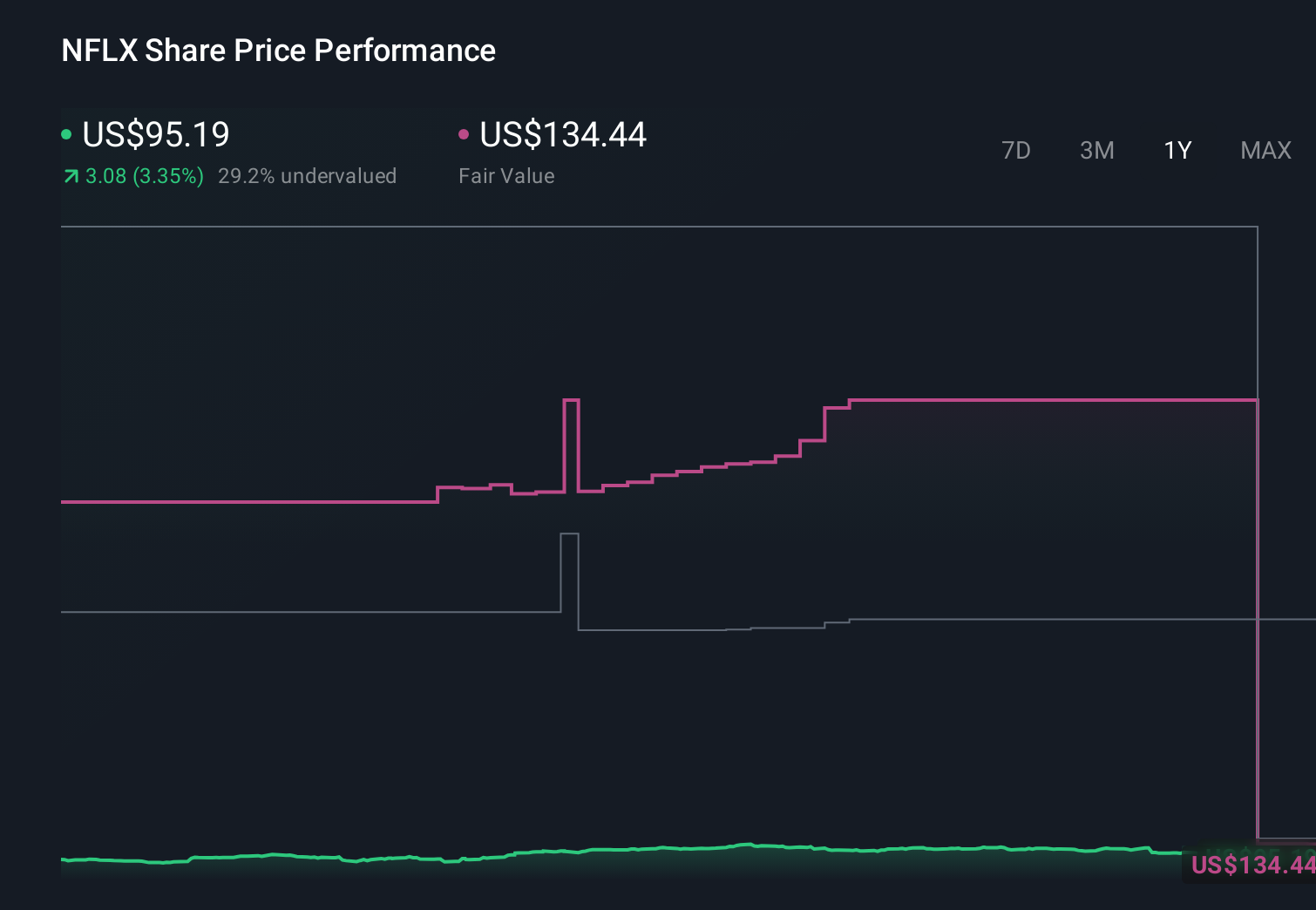

Netflix's narrative projects $64.7 billion revenue and $19.7 billion earnings by 2029. This requires 11.3% yearly revenue growth and about a $6.3 billion earnings increase from $13.4 billion today.

Uncover how Netflix's forecasts yield a $114.56 fair value, a 39% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts tell a much harsher story, assuming margins drift lower and 2029 earnings of only about US$16.8 billion, reminding you that reactions to the Warner breakup fee and “Attention OS” ambitions could still push expectations in very different directions.

Explore 27 other fair value estimates on Netflix - why the stock might be worth as much as 81% more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Netflix research is our analysis highlighting 5 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Netflix research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Netflix's overall financial health at a glance.

Searching For A Fresh Perspective?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Find 47 companies with promising cash flow potential yet trading below their fair value.

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.