Is NIKE (NKE) Overvalued On Flat Sales And Ongoing China Weakness?

NIKE, Inc. Class B NKE | 0.00 |

Nike (NKE) has become a flashpoint for debate after its latest quarterly report, which showed higher net income but flat revenue and continued weakness in China, drawing sharply different reactions from market commentators.

NIKE's latest earnings and the mixed reaction from commentators come after a difficult stretch for investors, with the share price down 29.88% year to date and the 1 year total shareholder return declining 36.9%. At the same time, the 1 day share price return of 3.72% and 7 day share price return of 2.38% suggest some short term momentum building around the recent results and ongoing debates about its China exposure, direct to consumer strategy and insider buying.

If NIKE's recent volatility has you thinking about where else growth stories might emerge, it could be worth scanning companies tied to the build out of AI infrastructure using the 52 AI infrastructure stocks

The bull case says Nike’s brand, insider buying, and North American wholesale strength are mispriced, while the bear case leans on flat sales, China weakness, and DTC weakness. Which side do the current valuation numbers support?

Most Popular Narrative: 20.5% Overvalued

Compared with NIKE's last close of $44.37, the most followed narrative pegs fair value at $36.83 using a 10.05% discount rate, painting a more conservative picture than the current market price.

Nike runs with a solid operating margin above the ~10% mark, showing it still has some competitive advantage over competitors even with the maturity of its business and a highly competitive industry. Despite currently having a flat revenue growth, its projections point to a slightly below economy growth rate of ~3% over the next couple of years. The fact that the ROIC is almost double its cost of capital is good to see.

The narrative leans heavily on strong returns on capital, modest growth expectations and a detailed cost of capital build. Want the full set of earnings, revenue and margin assumptions that sit behind that $36.83 number and the overvaluation call? The complete breakdown shows how different valuation methods are weighted, when the author thinks NIKE becomes attractive again and how cash flows, earnings paths and implied multiples tie together into that single fair value label.

Result: Fair Value of $36.83 (OVERVALUED)

However, weaker China demand and uncertainty around NIKE's direct to consumer performance could quickly challenge the current fair value story if sentiment shifts.

Another View on NIKE’s Valuation

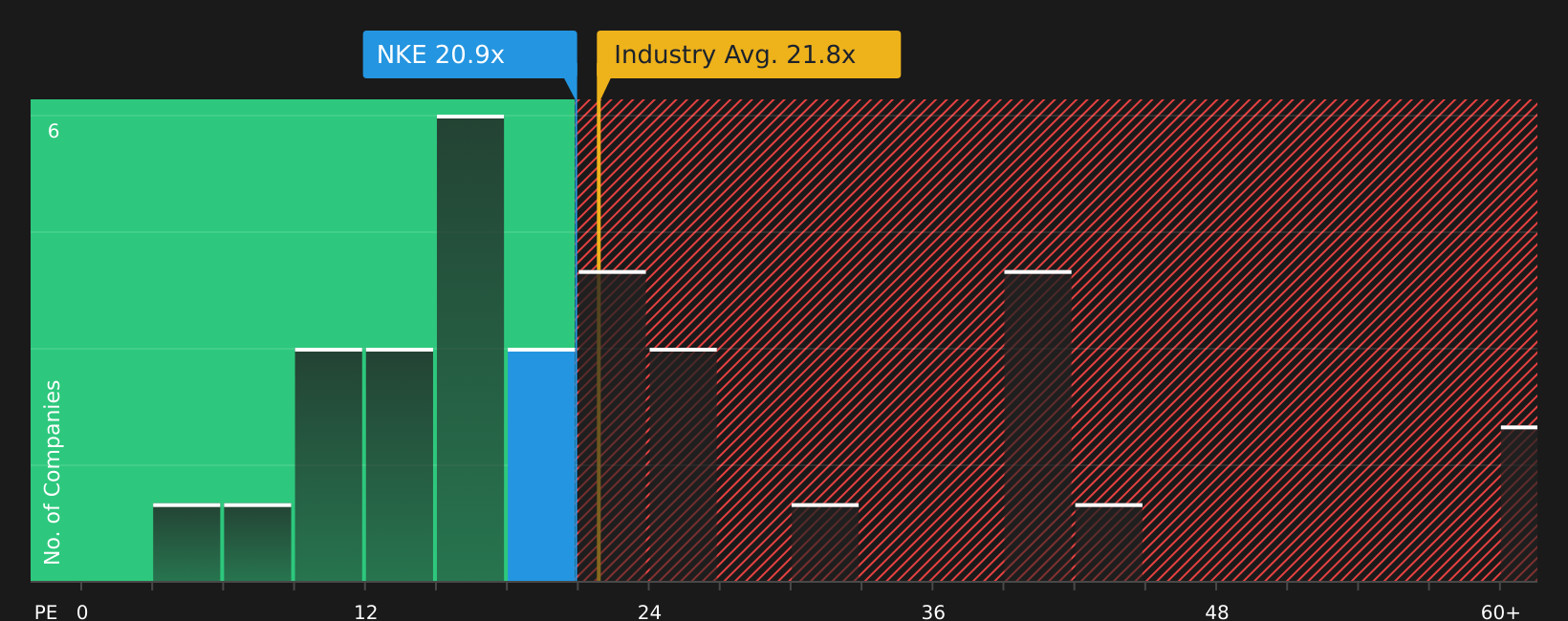

The user narrative leans on detailed cash flow work and ends at a fair value of $36.83 per share, which implies NIKE is overvalued. Our preferred P/E measure points in a different direction. At 21.1x earnings, NIKE trades below both the peer average of 29.1x and an estimated fair ratio of 26.6x, suggesting the market may already be pricing in a good chunk of earnings and growth risk. When one method says overvalued but the current P/E sits at a discount instead, it raises the question of which signal to weigh more heavily.

For readers weighing these mixed signals, it can be helpful to see how the numbers stack up in a single place, including how current pricing compares with peers, the industry and that fair ratio over time, in the See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment on NIKE so split, it makes sense to move quickly, review the numbers yourself, and weigh both sides of the story with the 3 key rewards and 1 important warning sign

Looking for more investment ideas beyond NIKE?

If NIKE's debate has sharpened your thinking, use that momentum to scan other opportunities where fundamentals, income potential and risk profiles align more closely with your goals.

- Target resilient cash flow compounding by reviewing companies in the 45 high quality undervalued stocks that combine solid fundamentals with valuations some investors may be overlooking.

- Strengthen your income stream by assessing stocks in the 9 dividend fortresses that focus on higher yields backed by underlying business stability.

- Prioritise capital preservation by filtering for companies in the 79 resilient stocks with low risk scores that emphasise stronger balance sheets and lower overall risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.