Is Norfolk Southern (NSC) Fairly Valued As Index Removal Clouds Its Earnings Outlook?

Norfolk Southern Corporation NSC | 0.00 |

Norfolk Southern (NSC) is back in focus after being dropped from the Russell 1000 Dynamic Index. This type of index change often triggers portfolio reshuffling by tracking funds and can affect short term trading activity.

Norfolk Southern’s recent removal from the Russell 1000 Dynamic Index comes against a backdrop of firm share price momentum, with a 90-day share price return of 12.05% and a 1-year total shareholder return of 25.22%. This suggests sentiment has been improving even as macro, network and coal related headwinds remain in focus.

If index reshuffles and sector headwinds have you reassessing your watchlist, this is a good moment to widen the search using our 35 power grid technology and infrastructure stocks

So with Norfolk Southern delivering solid recent returns, trading close to analyst targets, and still wrestling with earnings headwinds, is the stock now pricing in much of its future potential, or is there still a genuine opportunity for investors?

Most Popular Narrative: 3.2% Undervalued

Norfolk Southern is trading at $322.71 against a widely followed fair value narrative of about $333, which frames the stock as slightly undervalued on that model.

The commitment to $150 million in productivity and cost reduction initiatives over three years is being propelled by better labor productivity and fuel efficiency, which are anticipated to sustain EPS growth even if revenue growth slows. The company's focus on increasing customer confidence through consistent service improvements is leading to meaningful market share gains, particularly in merchandise and intermodal segments, which could bolster future revenue growth.

Want to see how that cost program, margin rebuild, and future earnings multiple all fit together for Norfolk Southern? The narrative leans on specific growth, profitability, and discount rate assumptions that materially shape that $333 fair value story.

Result: Fair Value of $333 (UNDERVALUED)

However, the Norfolk Southern narrative could be tested if storm restoration costs recur at scale or if weaker export coal pricing keeps pressure on revenue and margins.

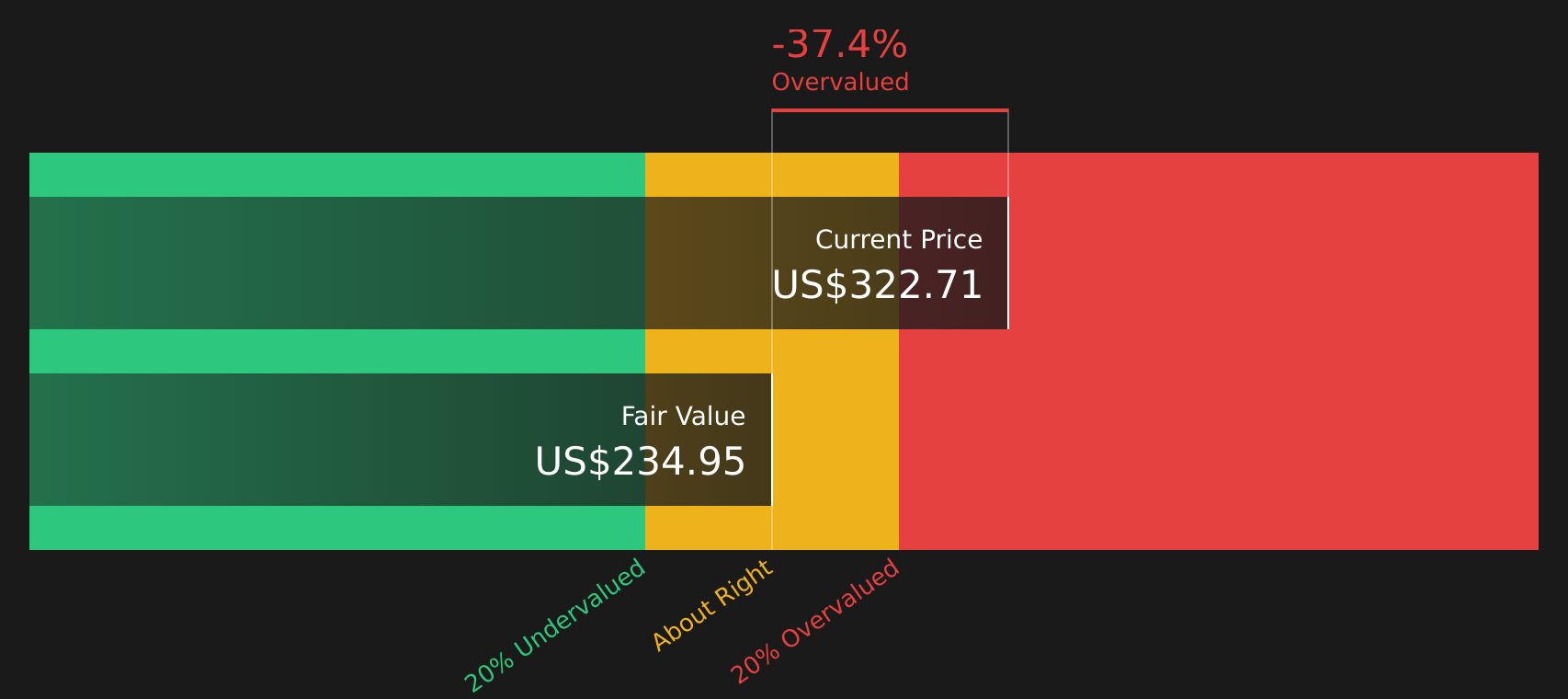

Another View: Norfolk Southern Through a Cash Flow Lens

There is also a very different message coming from our DCF model. On that approach, Norfolk Southern at $322.71 is trading above an estimated future cash flow value of about $235, which screens as expensive and sits awkwardly against the $333 fair value narrative you just saw.

For you, the question is which story feels more realistic: a market that pays up for earnings and potential merger outcomes, or one that pulls the price closer to what the SWS DCF model suggests is justified over time.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Norfolk Southern for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Sentiment around Norfolk Southern in this article is clearly mixed, so treat it as a prompt to move quickly and pressure test the data yourself using the full breakdown of 3 key rewards and 1 important warning sign

Looking for more Norfolk Southern style investment ideas?

If you are reassessing Norfolk Southern and want fresh opportunities on your radar, use the Simply Wall Street Screener to spot other stocks that match your criteria.

- Target quality at a discount by scanning companies that pass strict value and fundamentals checks with the 44 high quality undervalued stocks

- Prioritize resilience by focusing on companies that pair earnings power with low risk profiles using the 74 resilient stocks with low risk scores

- Get ahead of the crowd by searching for solid fundamentals in companies that the market has not yet focused on through the screener containing 18 high quality undiscovered gems

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.