Is Now the Right Moment for Enphase Stock After the Recent 6.7% Rally?

Enphase Energy, Inc. ENPH | 38.28 38.40 | +1.24% +0.31% Post |

If you are holding Enphase Energy stock or eyeing it with curiosity, you are definitely not alone. The company’s recent price swings have caught the attention of more than a few market-watchers. After notching a 6.7% gain in the past seven days, the stock has turned some heads, even as it still sits well below its previous highs. That short-term pop stands out, especially against its longer-term track record, with shares down around 48.8% year-to-date and an even steeper 60.1% drop over the past year. When you look back further, the three- and five-year declines paint an even starker picture, keeping both optimists and skeptics on their toes.

What is driving the latest shift in sentiment? Some of it tracks to renewed interest in alternative energy plays, as global policy moves encourage greener solutions. There is also fresh momentum in the solar sector at large, with investors recalibrating risk and potential as market conditions evolve. If you are feeling pulled between caution and opportunity, that is understandable. Enphase continues to be a lightning rod for opinions in both camps.

So is Enphase a bargain, or is the recovery just a pause on a downward slide? According to a comprehensive valuation analysis, Enphase Energy scores 4 out of 6 on key undervaluation checks. That is a strong signal there may be value that the broader market is overlooking. Next, let us dive into the specific valuation measures and see how the numbers stack up, before wrapping up with an even more insightful way to think about what Enphase might really be worth.

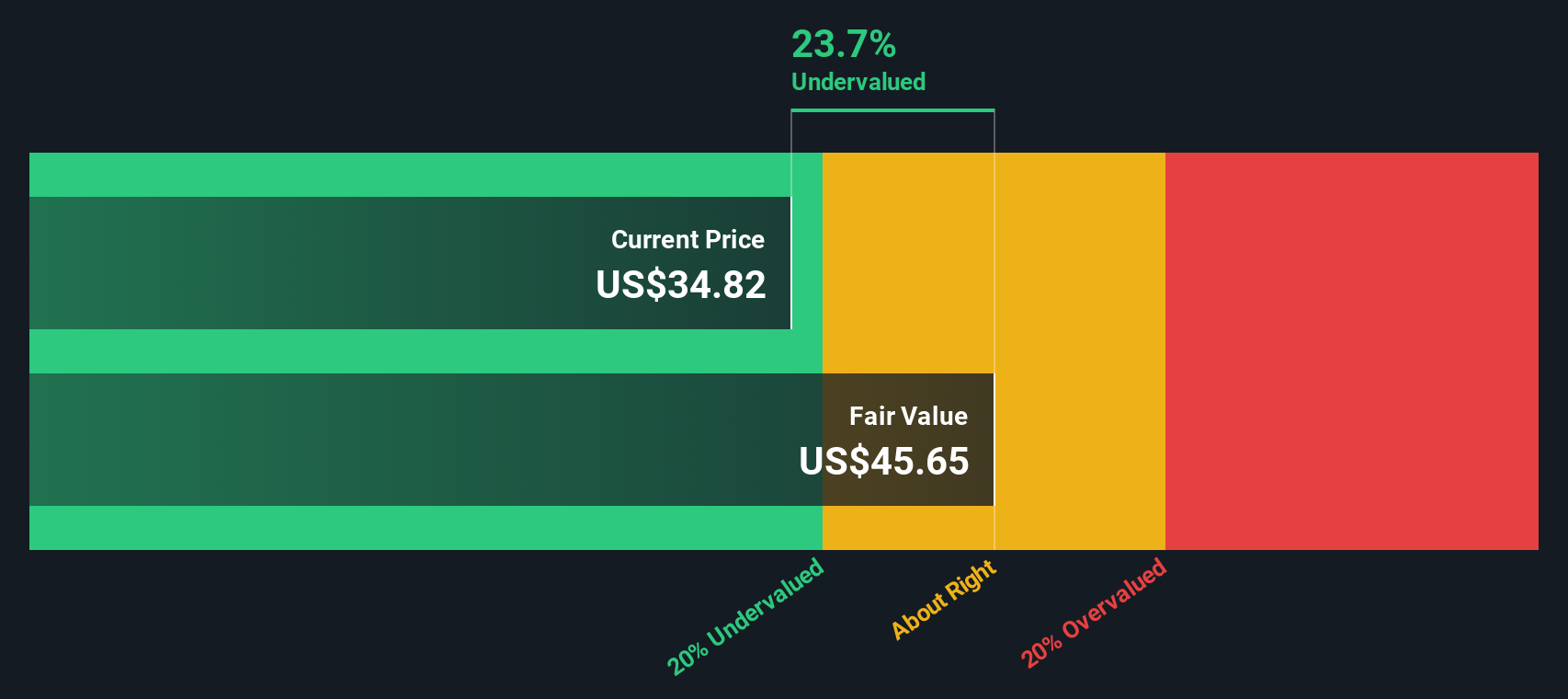

Approach 1: Enphase Energy Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model projects a company’s future cash flows, then discounts them back to today’s dollars to estimate what the business might truly be worth. This approach allows investors to cut through short-term market noise and focus on long-term fundamentals.

For Enphase Energy, the latest twelve-month Free Cash Flow (FCF) stands at $362.5 million. Analysts expect FCF to trend higher over several years, with estimates up to 2029 showing annual cash flow reaching $491.45 million. Beyond that, further growth is extrapolated by Simply Wall St to reflect potential performance ten years out.

Using these projections, the DCF valuation model estimates Enphase’s intrinsic value at $46.66 per share. This value is based on detailed cash flow forecasts, all measured in US dollars, and reflects both analyst insights and longer-term estimates. Compared to the current market price, this means Enphase stock trades at a 21.6% discount. This suggests it is undervalued according to this model.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Enphase Energy is undervalued by 21.6%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

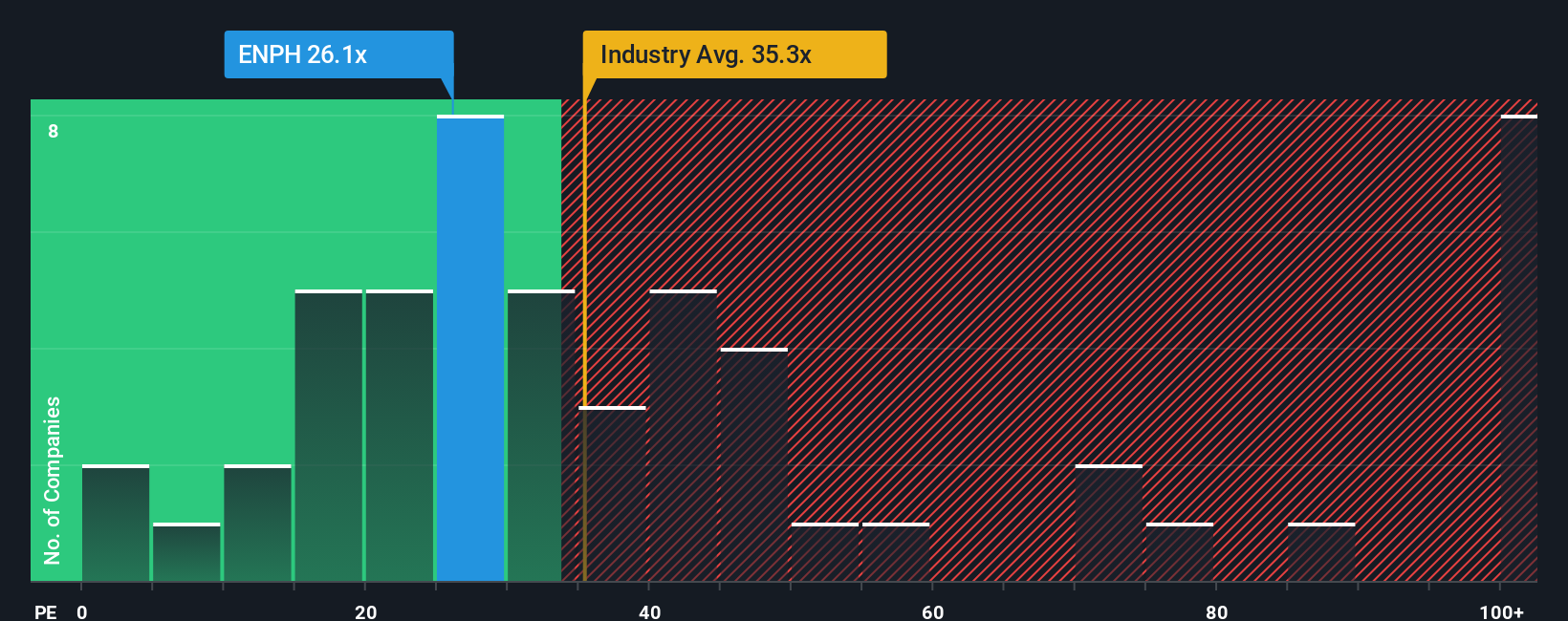

Approach 2: Enphase Energy Price vs Earnings

For companies like Enphase Energy that are generating consistent profits, the Price-to-Earnings (PE) ratio is one of the most widely accepted tools for gauging value. It provides a straightforward way to see how much investors are willing to pay today for a dollar of earnings, which is especially relevant for profitable, growing businesses.

The "right" PE ratio depends on expectations. Investors pay up for growth while demanding lower multiples for risk or slower expansion. As of now, Enphase trades on a PE ratio of 27.4x, notably below the semiconductor industry average of 35.9x and even further below the peer group average of 43.3x. This suggests investors see either less growth ahead for Enphase or are factoring in higher perceived risks.

Simply Wall St goes a step further with its proprietary Fair Ratio, which determines what PE multiple Enphase should command given its growth prospects, profit margins, risks, industry dynamics, and market capitalization. For Enphase, this Fair Ratio stands at 24.8x, a touch below its actual multiple. Rather than just a simple peer comparison, this Fair Ratio offers a more tailored evaluation and accounts for company- and sector-specific dynamics that traditional benchmarks can miss.

With Enphase’s current PE just slightly above the Fair Ratio, the valuation looks fairly balanced at these levels.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

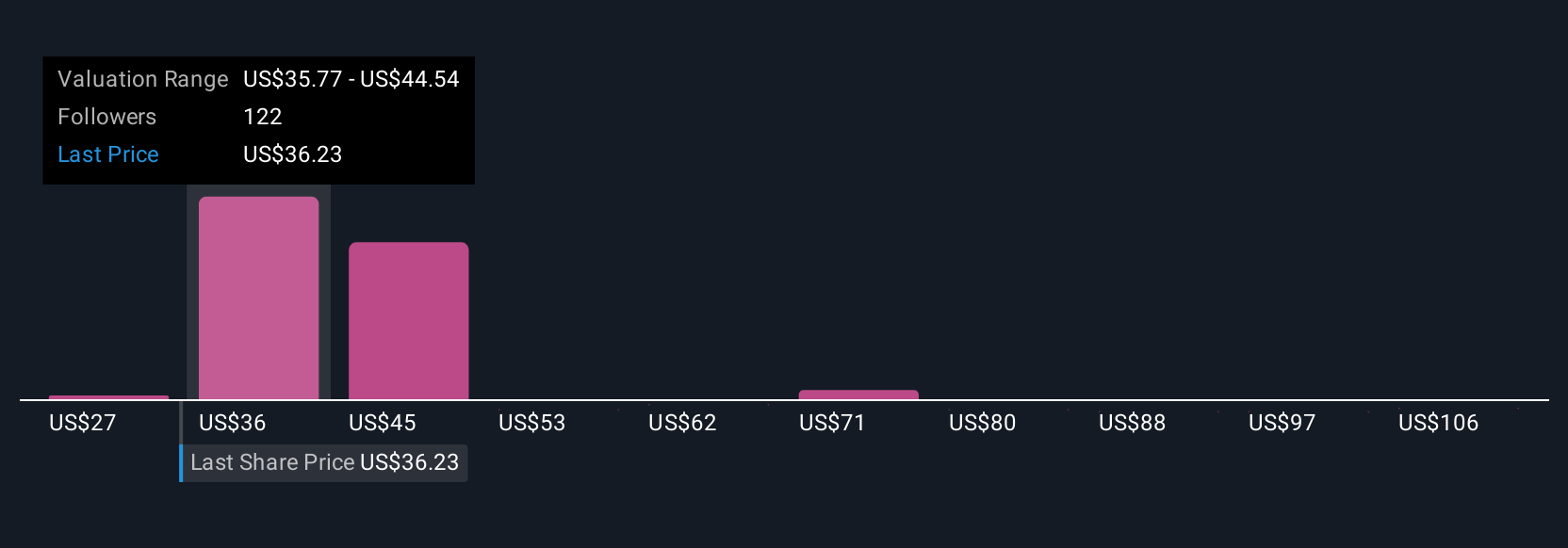

Upgrade Your Decision Making: Choose your Enphase Energy Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. A Narrative is your story about a company, including the assumptions you make about its future revenue, earnings, margins, and the fair value you estimate as a result. Narratives connect the dots between what you believe will drive a company's future, how that flows into a financial forecast, and ultimately, what you think a stock is really worth.

Narratives are a simple yet powerful tool available on Simply Wall St’s Community page, where millions of investors share and refine their perspectives in real time. By building your own Narrative or exploring others, you can compare your estimated Fair Value to the current share price, helping you decide when the numbers signal an opportunity to buy, sell, or wait. Whenever important news or new financial data emerges, Narratives are automatically updated so your decision is always grounded in the latest facts.

For example, when looking at Enphase Energy, some Narratives reflect optimism and expect a fair value as high as $120 per share driven by recovery and global expansion. Others anticipate further headwinds and project values as low as $27 based on policy risks and softer demand. Narratives make it clear that your investment decisions are most powerful when your story matches your strategy.

Do you think there's more to the story for Enphase Energy? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.