Is Now the Right Moment to Consider Western Digital After Its 155% Surge in 2025?

Western Digital Corporation WDC | 343.43 | +1.64% |

- Wondering if Western Digital is a smart buy right now? You're not alone. Curiosity about whether the current price is justified is increasing among investors.

- The stock just soared 31.0% over the past month and is up an incredible 155.1% year-to-date, showing strong momentum, even with a brief 3.1% dip in the past week.

- Recent headlines have highlighted the semiconductor sector's resurgence and Western Digital's strategic decisions on product innovation. Buzz around artificial intelligence data growth and renewed focus on flash memory has also put the company in the spotlight for potential long-term relevance.

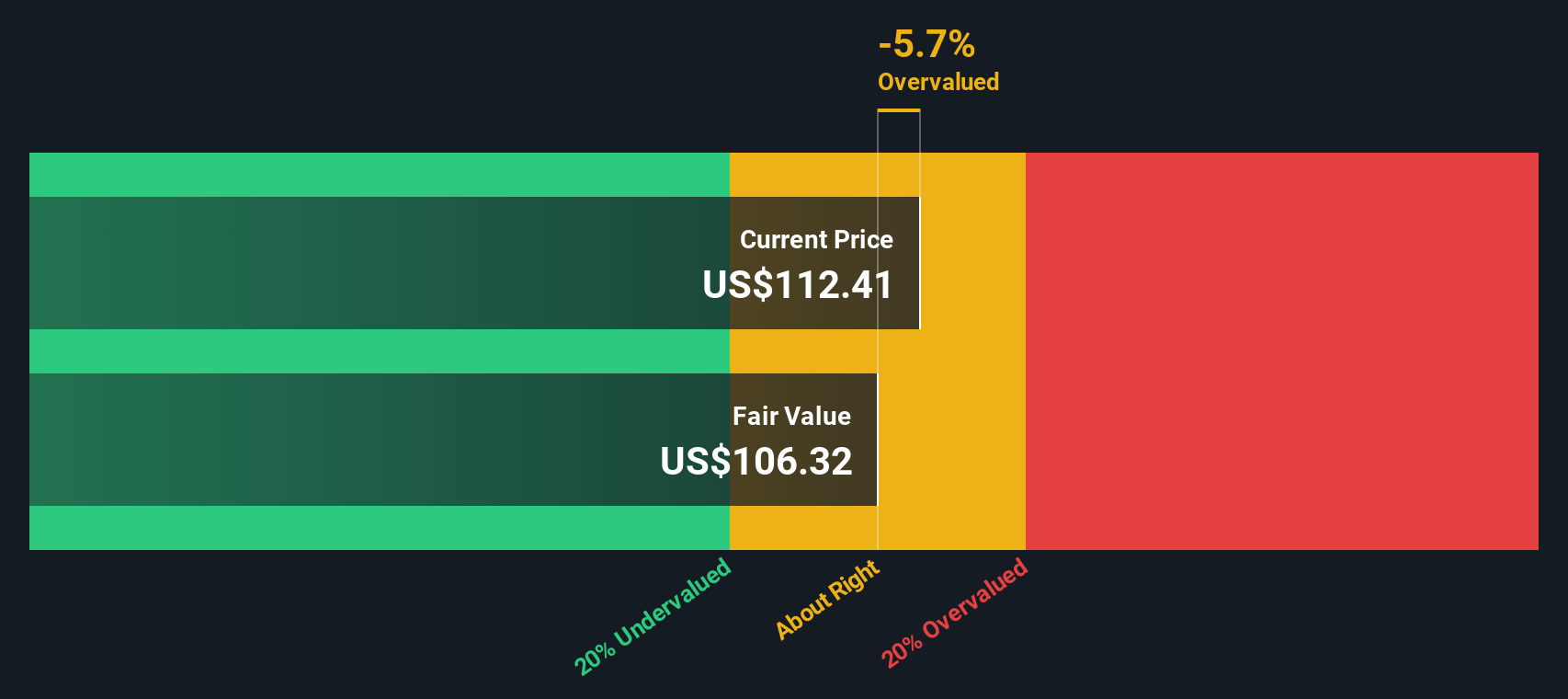

- Western Digital currently scores a 5 out of 6 on our undervaluation checklist, suggesting strong value credentials. Here is a closer look at how this score is determined using a range of valuation methods, and why it might not tell the entire story.

Approach 1: Western Digital Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future free cash flows and discounting them back to their present value. This approach helps investors determine what the business is really worth today based on its ability to generate cash in the years ahead.

For Western Digital, the most recent reported Free Cash Flow stands at $1.79 billion. Analysts provide detailed cash flow forecasts for the next five years, projecting continued growth. By the year 2030, Western Digital's Free Cash Flow is anticipated to reach $4.29 billion, reflecting healthy expectations for expansion in the data storage and flash memory markets. Beyond analyst coverage, further cash flow projections are extrapolated to extend the valuation horizon.

Using a 2 Stage Free Cash Flow to Equity model, the DCF analysis results in an estimated intrinsic value of $230.25 per share. This is substantially higher than the company's current market price. This suggests that the stock is trading at a 31.5% discount to its calculated fair value.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Western Digital is undervalued by 31.5%. Track this in your watchlist or portfolio, or discover 874 more undervalued stocks based on cash flows.

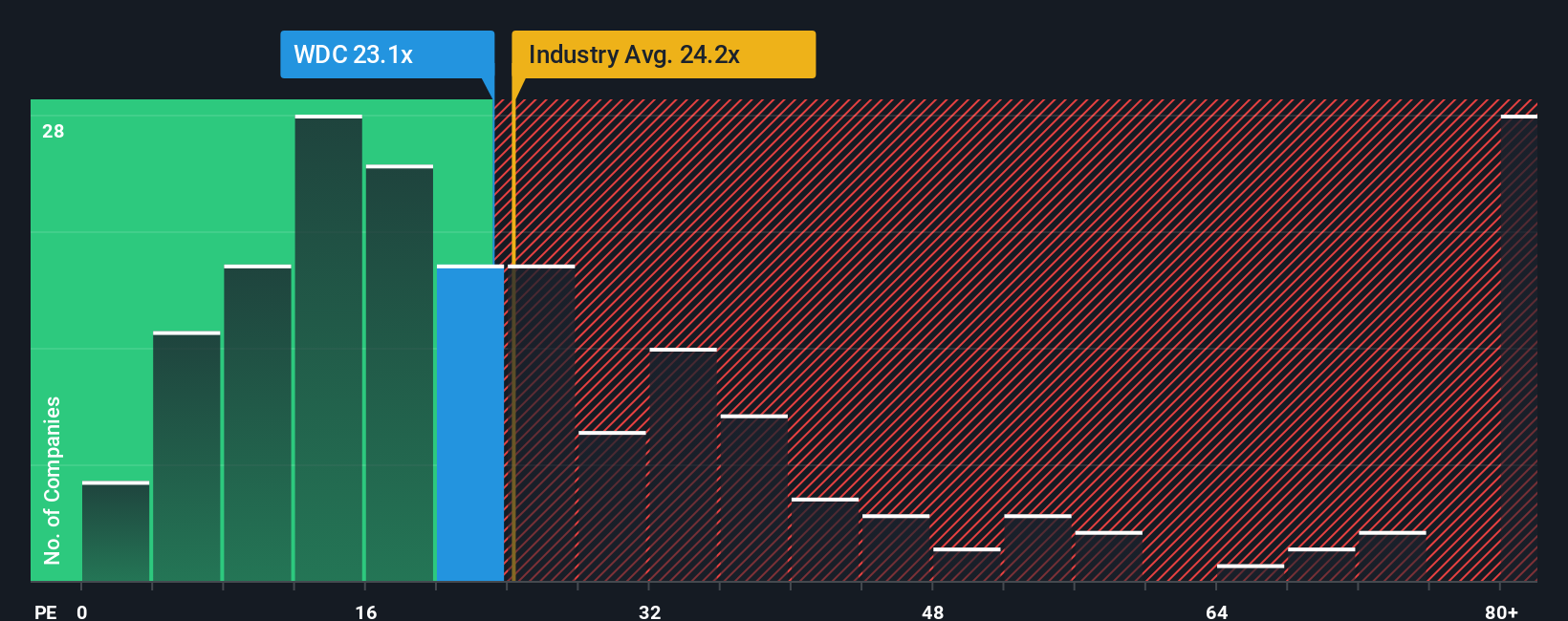

Approach 2: Western Digital Price vs Earnings

The Price-to-Earnings (PE) ratio is a widely used valuation metric for profitable companies like Western Digital because it relates a company's market value directly to its earnings power. For investors, a lower PE can signal an attractive entry point if earnings are expected to grow, while a higher PE may indicate the stock is priced for high future growth or lower risk.

Determining what counts as a “fair” PE ratio depends on both growth expectations and company-specific risks. Typically, higher growth companies can justify higher PE ratios, while riskier businesses or those in more mature industries tend to trade closer to the average or below.

Western Digital currently trades on a PE ratio of 20.75x. This is just below the average for the US tech industry, which sits at 22.05x, and slightly under the peer group average of 21.64x. However, Simply Wall St's proprietary Fair Ratio for Western Digital is calculated as 38.63x. This calculation incorporates not only the company’s expected earnings growth but also its profit margins, industry conditions, market cap, and specific risk profile.

Unlike a simple comparison to industry or peer averages, the Fair Ratio provides a more tailored benchmark by capturing the unique characteristics that drive value for Western Digital. This makes it a more holistic and informed basis for valuation.

With Western Digital's actual PE ratio sitting well below the Fair Ratio, the stock looks undervalued based on this approach.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1401 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Western Digital Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. Narratives are the stories investors build around a company, anchoring their personal assumptions about future revenue, earnings, and margins to a clear financial forecast and a calculated fair value. This approach gives context to the numbers.

With Narratives, anyone can connect “the story” they believe about Western Digital to numbers such as fair value estimates, growth trajectories, and margin outlooks right on Simply Wall St’s Community page. This feature makes it simple to compare your own outlook to the consensus or see how diverging opinions play out as new information arrives, since Narratives automatically update with each news release or earnings result.

By comparing the fair value from your unique Narrative to the current share price, Narratives help guide your decisions about when to buy or sell, all based on logic you believe in. For example, some investors might see Western Digital’s long-term integration with hyperscale cloud as a reason to set a high price target, while others may focus on risk from emerging storage technologies and choose a much lower fair value, all within the same dynamic tool.

Do you think there's more to the story for Western Digital? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.