Is Now the Right Time to Reassess FICO Shares After Recent Market Drop?

Fair Isaac Corporation FICO | 1060.96 | -0.62% |

Thinking about what to do with Fair Isaac stock right now? You are definitely not alone. If you have been tracking the markets, you have likely noticed that Fair Isaac has taken its investors on quite a ride recently. After a dip of 5.2% over the past week, and a modest 4.3% gain across the last month, the stock is still down a steep 18.8% year-to-date. Go back a year and the pain is similar, with a 20.5% slide. But zoom out a little further and the story shifts: Fair Isaac has delivered an impressive 296.5% return over three years and 274.1% over five, far outpacing many peers.

It is no wonder investors are debating whether this is a moment of renewed value, a warning flag, or maybe just a classic market mood swing. Part of the recent weakness seems connected to broader sector rotation and shifting risk appetites among institutional buyers, rather than any dramatic change in the company's underlying fundamentals. That is why now is a perfect time to pause and ask: how does Fair Isaac actually stack up on valuation?

Based on six widely used valuation checks, Fair Isaac earns a value score of just 2. That signals the stock is currently undervalued in only two out of those six common measures. Does that mean it is a bargain in disguise, or are investors right to be cautious? Let us break down exactly how those valuation methods apply to Fair Isaac. Stay tuned, because there is an even sharper way to look at value that we will reveal at the end.

Fair Isaac scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Fair Isaac Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s intrinsic value by projecting future cash flows and discounting them back to today’s dollars. For Fair Isaac, this approach takes into account expected Free Cash Flow (FCF) growth and then adjusts for present value to help investors judge whether the current price is justified.

Fair Isaac’s latest twelve-month Free Cash Flow stands at $772 Million. Analysts project continued growth, forecasting FCF to reach $1.69 Billion by 2029. Estimates cover up to five years, with longer-term projections extrapolated by Simply Wall St based on trends and company performance.

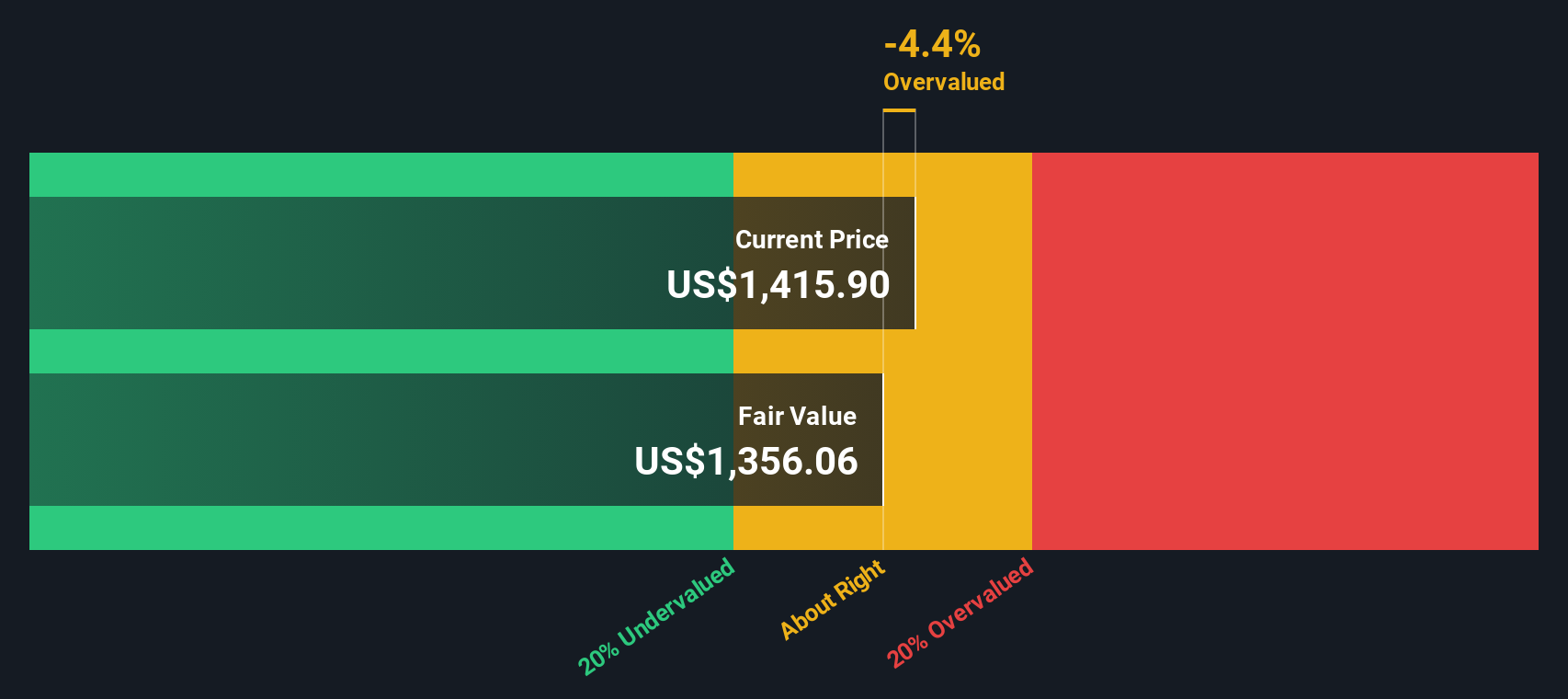

When these cash flows and long-term assumptions are incorporated, the DCF model calculates an intrinsic fair value of $1,305.74 per share. However, the analysis indicates the stock trades at a 24.1% premium to this assessment. This suggests Fair Isaac appears considerably overvalued according to its projected future cash generation.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Fair Isaac may be overvalued by 24.1%. Find undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Fair Isaac Price vs Earnings (PE)

The Price-to-Earnings (PE) ratio is a widely used valuation metric for profitable companies like Fair Isaac, because it directly connects a company's current share price to its per-share earnings. For investors, the PE ratio provides a quick sense of how much they are paying for each dollar of earnings generated by the business.

Growth expectations and risks play a big role in what counts as a “normal” or “fair” PE ratio. Companies with strong, reliable earnings growth tend to justify higher PE multiples, while higher risks or slow growth call for lower ratios. That makes context crucial when interpreting any PE number, especially in fast-changing industries like software.

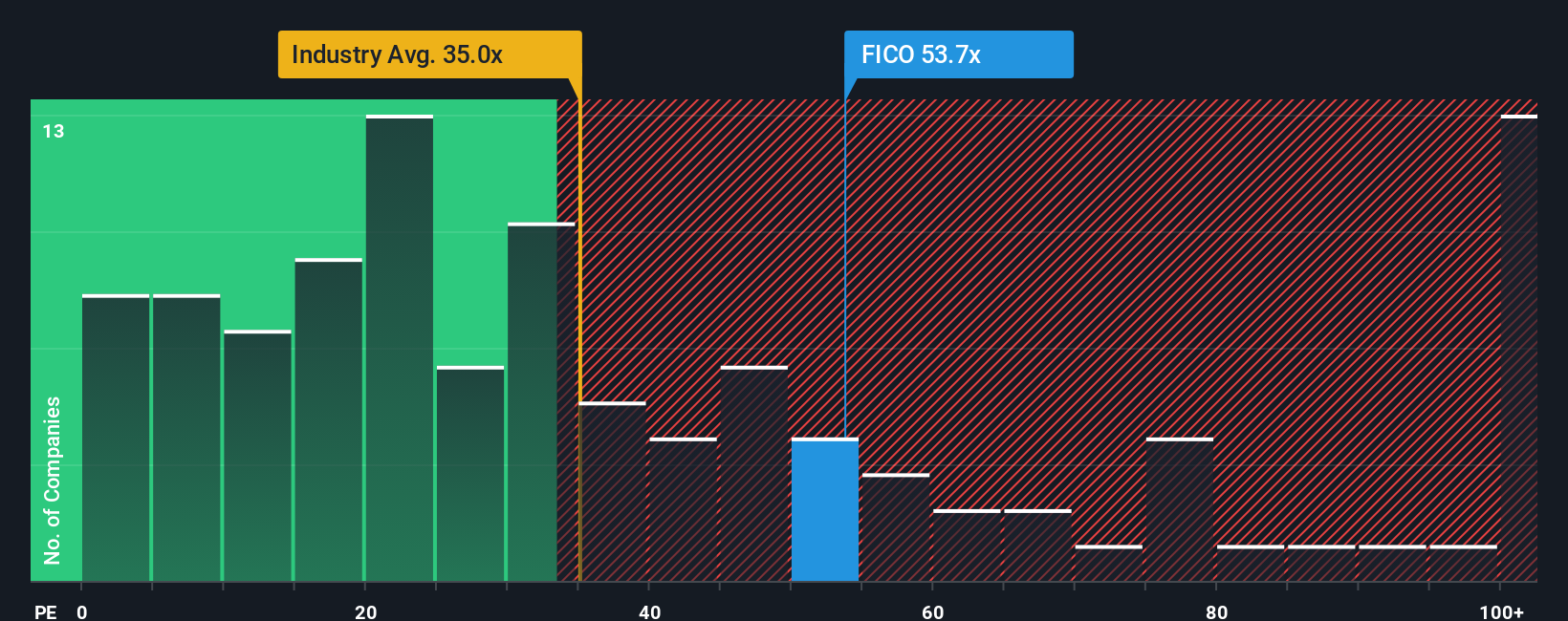

Fair Isaac currently trades at a PE ratio of 61.47x, which is right around the average of its closest peers at 61.89x and well above the broader software industry average of 34.97x. Rather than relying strictly on those benchmarks, Simply Wall St offers a proprietary “Fair Ratio,” which weighs not only industry averages and peer multiples, but also factors like Fair Isaac’s own earnings growth prospects, profit margins, company size, and risk factors. In this case, the Fair Ratio stands at 43.05x, reflecting the earnings multiple that best captures the company’s specific fundamentals and risk profile.

Because the actual PE ratio is meaningfully higher than the Fair Ratio, Fair Isaac appears overvalued on this metric, even accounting for company-specific strengths.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Fair Isaac Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. A Narrative goes beyond traditional ratios and projections by letting you attach a "story" to your numbers, focusing on your view of what drives Fair Isaac’s future and how those beliefs translate to revenue growth, profit margins, and ultimately, your own Fair Value estimate.

In simple terms, Narratives allow you to connect your big-picture perspective to real company forecasts and a calculated fair price. This creates a logical bridge between what you believe and the numbers behind your investment decisions. Narratives are accessible to everyone and built right into the Simply Wall St Community page, making it easy to try this smarter approach used by millions of investors worldwide.

By comparing your Narrative Fair Value to the current share price, you can instantly see whether your view leads you to consider buying or selling. As news or financial results emerge, your Narrative dynamically updates to reflect the latest information.

For example, some investors see Fair Isaac’s bold cloud migration and international partnerships unlocking durable earnings, leading them to set a bullish $2,300 fair value. Others, wary of disrupting regulations and rising competition, estimate value much lower, closer to $1,230. Which Narrative makes more sense? Now, you decide, with the numbers, story, and decision all in your hands.

Do you think there's more to the story for Fair Isaac? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.