Is Now the Right Time to Reassess PDD After Its 42% Rally in 2025?

PINDUODUO INC. PDD | 0.00 |

- Ever wonder if PDD Holdings is still a bargain or if you might be late to the party? Let’s take a closer look at why this might be a pivotal moment for investors who are keeping an eye on valuation.

- In the past week, PDD’s share price jumped 6.2%, is up 5.7% over the last month, and has surged an impressive 42.5% year-to-date. These moves suggest renewed optimism and may indicate some big shifts in risk perception.

- Recent headlines have highlighted PDD’s ongoing expansion into international markets and strategic partnerships with major brands. Both developments have caught the attention of investors and the business press. This increased visibility is fueling speculation about its future growth and could be a key driver behind the latest price moves.

- On valuation, PDD scores a strong 5 out of 6 checks for being undervalued according to common metrics. We will walk through what those valuation methods say, but stick around, as there may be an even more insightful way to think about value by the end of this article.

Approach 1: PDD Holdings Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company’s intrinsic value by projecting future cash flows and discounting them back to today using a risk-adjusted rate. This approach helps investors understand what a business might be worth based on its potential to generate cash over time.

For PDD Holdings, the latest reported Free Cash Flow stands at CN¥93.25 billion. Analyst forecasts suggest this figure will continue to grow steadily, reaching a projected CN¥287.88 billion in 2035. While analysts only provide cash flow projections for the next five years, models such as Simply Wall St’s 2 Stage Free Cash Flow to Equity build on these estimates by extrapolating future trends beyond the available data.

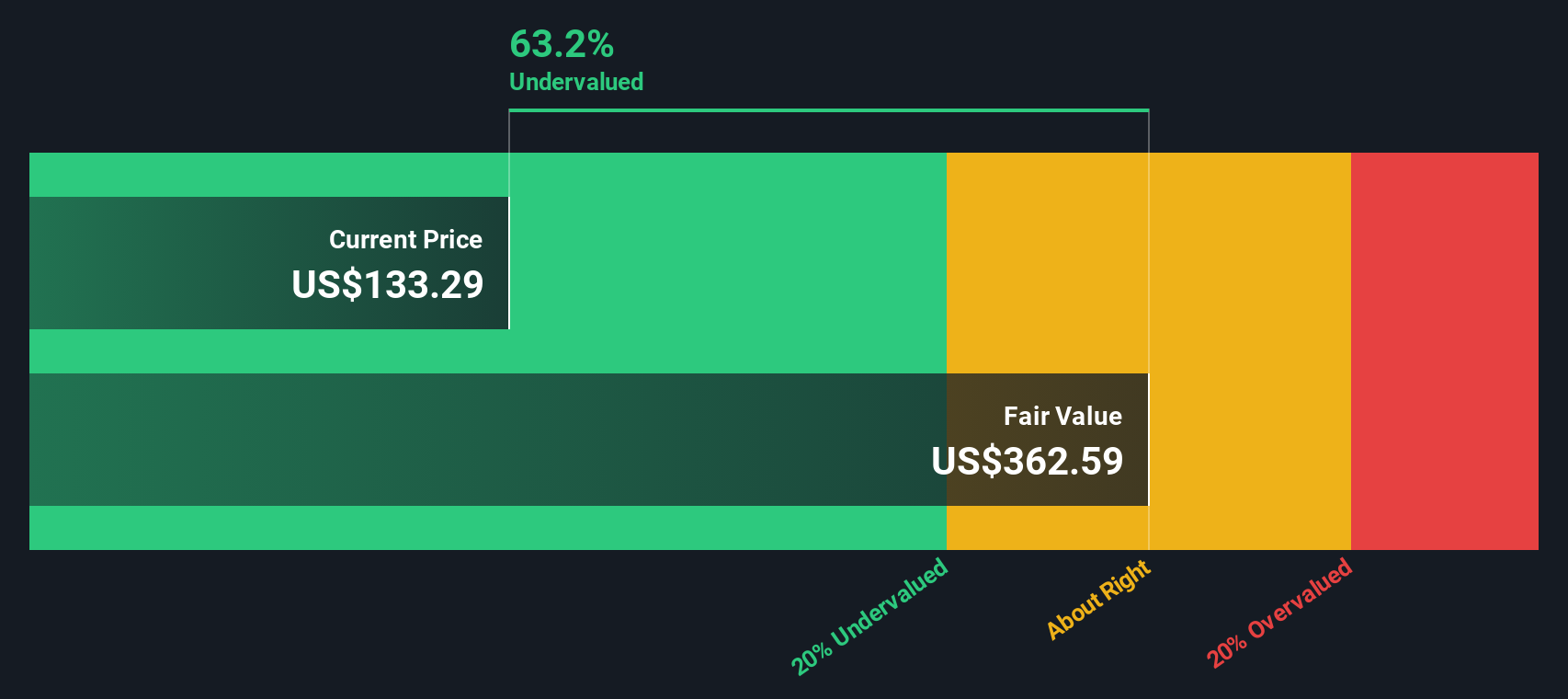

Based on the DCF analysis, PDD’s estimated fair value is approximately $363.13 per share. Compared to its current market price, this suggests the stock is trading with a 62.0% discount, which may indicate the market is undervaluing the company’s future cash flow potential.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests PDD Holdings is undervalued by 62.0%. Track this in your watchlist or portfolio, or discover 848 more undervalued stocks based on cash flows.

Approach 2: PDD Holdings Price vs Earnings

The Price-to-Earnings (PE) ratio is often the go-to metric for valuing profitable companies like PDD Holdings. This ratio tells investors how much they are paying for each dollar of current earnings, making it a widely understood and relevant tool for companies with strong, consistent profits.

However, a "fair" PE ratio is not one-size-fits-all. Higher growth expectations or lower perceived risk generally justify a higher PE, while greater risks or slower growth call for a more modest number. This is why context matters so much in drawing conclusions from any valuation multiple.

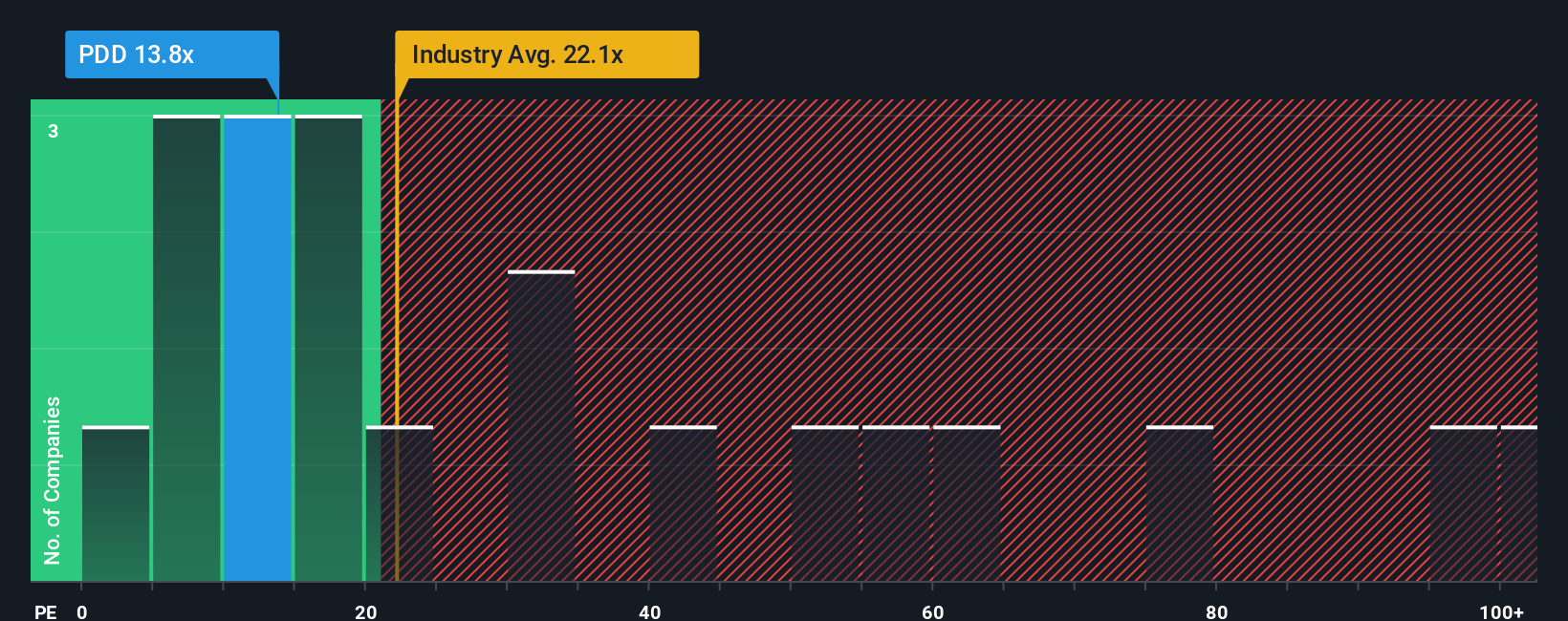

PDD Holdings currently trades at a PE ratio of 14.2x. Compared to the Multiline Retail industry average of 21.4x and the peer average of 78.3x, PDD might appear undervalued at first glance. However, comparing plain PE ratios can be misleading because they do not account for important factors such as a company’s earnings growth, profitability, risk profile, industry sector, or size.

This is where Simply Wall St’s proprietary “Fair Ratio” comes into play. The Fair Ratio, calculated here as 28.5x for PDD, blends factors including expected growth, market cap, margins, and relevant industry benchmarks to produce a more tailored and meaningful standard than peers or industry averages alone.

In PDD's case, its actual PE ratio of 14.2x is well below the Fair Ratio of 28.5x. This suggests the stock is noticeably undervalued based on its earnings power relative to its unique situation and outlook.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1387 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your PDD Holdings Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is more than just a number; it is a story you create that connects your own perspective on a company with specific forecasts for its future revenue, profit margins, and a fair value per share.

Narratives let you put your investment thesis into action by linking the big picture, such as PDD’s international expansion, profitability trends, or market challenges, to concrete financial outcomes. On Simply Wall St’s Community page, millions of investors are already using the Narratives tool to visualize, share, and update their views as new facts come in. This makes it easy to see how the market’s story about PDD evolves over time.

Narratives go further than traditional ratios by showing you at a glance how your fair value compares to the current price, so you can decide whether now is the right moment to buy or sell. And since Narratives dynamically incorporate fresh information, like news headlines or quarterly results, you are never stuck with out-of-date assumptions.

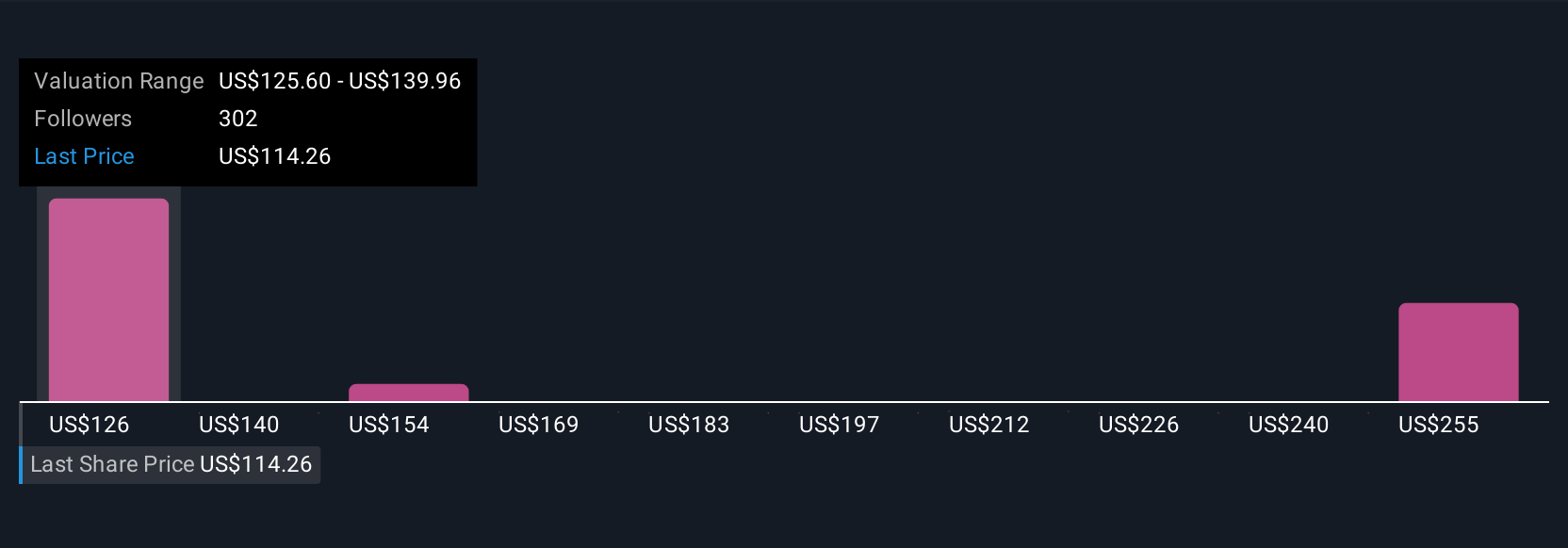

For example, one investor’s Narrative might point to accelerating growth and set a bullish price target of $176.36, while another could be more cautious and estimate a fair value as low as $117.02, based on different outlooks for PDD’s margins, competition, or global strategy.

Do you think there's more to the story for PDD Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.