Is NuScale Power (SMR) Pricing In Nuclear Policy Support Despite Mixed Long Term Returns

NuScale Power SMR | 0.00 |

- If you are wondering whether NuScale Power's current share price reflects its true worth, this article will help you size up the stock using several valuation tools.

- The stock recently closed at US$11.87, with returns of 0.4% over 7 days, 16.9% over 30 days, a 27.2% decline year to date, a 32.8% decline over 1 year, 47.6% over 3 years and 19.8% over 5 years. This gives you a wide range of outcomes to think about.

- Recent coverage has focused on NuScale Power's role in nuclear energy infrastructure and how changing sentiment around the sector may affect companies involved in advanced reactor design. Media attention on policy support for low carbon power and debates around nuclear's role in future grids has provided extra context for recent price moves.

- On Simply Wall St's valuation checks, NuScale Power scores 1 out of 6. The next sections will compare different valuation approaches, with a look at an even more complete way to think about value at the end of the article.

NuScale Power scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

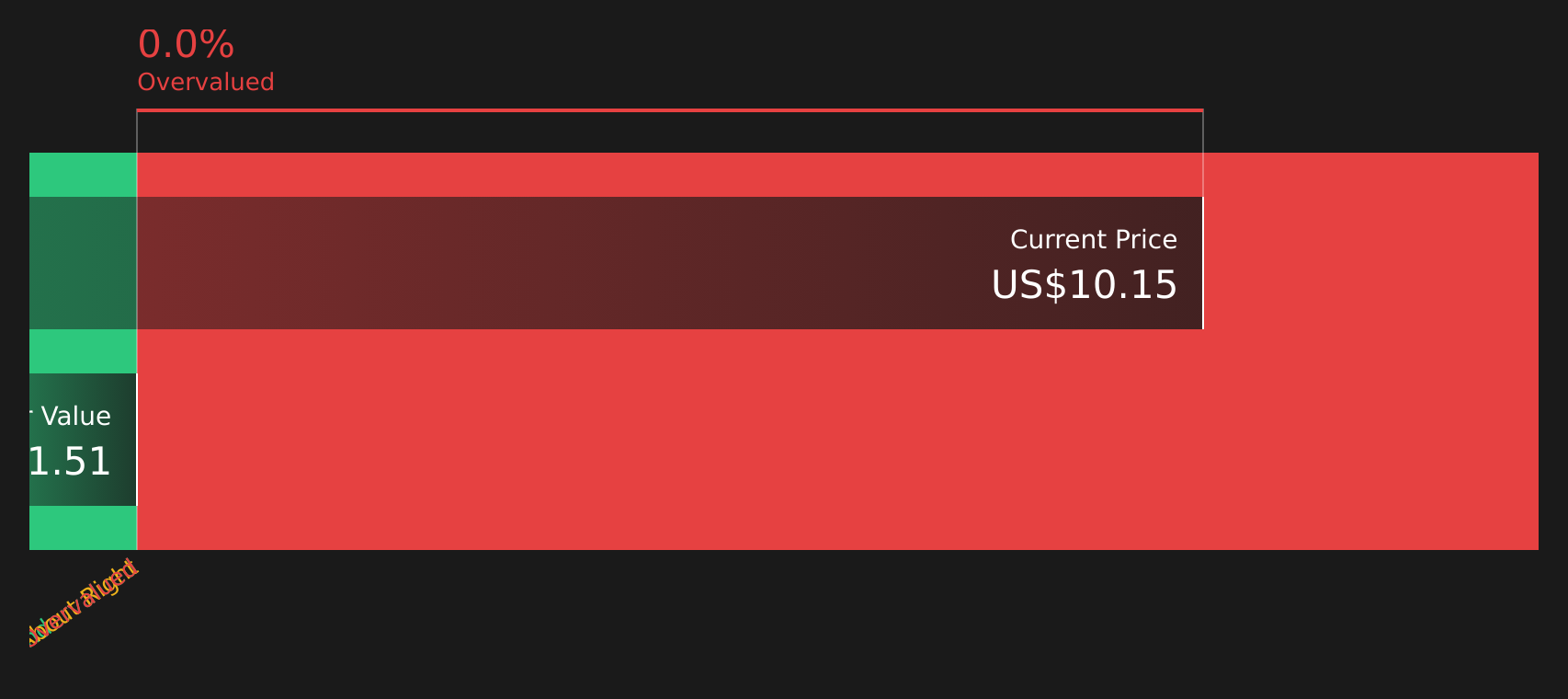

Approach 1: NuScale Power Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a stock could be worth by projecting the company’s future cash flows and discounting them back to today’s value.

For NuScale Power, the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow is a loss of about US$460.4 million. Analysts provide free cash flow estimates out to 2030, with Simply Wall St extrapolating further years. Within these projections, free cash flow is still negative in the nearer years, then shifts to a projected US$103.66 million by 2030, with additional estimated figures out to 2035.

Bringing all of these projected cash flows back to today, the DCF results in an estimated intrinsic value of about US$6.93 per share. Compared with the recent share price of US$11.87, this model implies the stock is around 71.2% overvalued on these assumptions.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests NuScale Power may be overvalued by 71.2%. Discover 50 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: NuScale Power Price vs Book

For companies that are not yet consistently profitable, P/B can be a useful way to think about value because it compares the share price with the accounting value of net assets. It is often used alongside expectations for future growth and the risks around turning those assets into sustainable profits.

A higher “normal” or “fair” P/B ratio is usually linked to stronger growth expectations and lower perceived risk, while lower ratios often reflect weaker growth prospects or higher uncertainty. For NuScale Power, the current P/B ratio is 3.29x. This is close to the Electrical industry average of 3.21x and below the peer group average of 12.57x, which gives you a first sense of how the stock is valued against its sector and selected peers.

Simply Wall St’s Fair Ratio is a proprietary estimate of what the P/B ratio “should” be, given NuScale Power’s earnings profile, industry, profit margins, market value and key risks. Because it combines these factors into a single number, it can be more tailored than a simple comparison to industry or peer averages. However, no Fair Ratio figure is available here, so it is not possible to say whether the current P/B suggests the stock is overvalued, undervalued or about right.

Result: ABOUT RIGHT

P/B ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your NuScale Power Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives are introduced here as your way of attaching a clear story about NuScale Power to the numbers, linking what you believe about its reactors, projects and risks to a forecast for revenue, earnings and margins, which then flows through to a fair value that you can compare with the current price.

On Simply Wall St’s Community page, Narratives are set up as simple, editable profiles where you choose your assumptions rather than accept a single “right” answer. You can, for example, line up one view that is closer to the lower US$8 fair value implied by the most cautious targets against another that resembles the upper US$60 fair value used by more optimistic forecasts and decide where you sit between them.

Because these Narratives update when fresh information arrives, such as NuScale Power’s cash balance, ENTRA1 developments, analyst revisions or new project milestones, you always see how those changes filter through to fair value. This can help you decide whether today’s share price offers a margin of safety, looks stretched or sits somewhere in the middle based on your own story for the company.

For NuScale Power, here are previews of two leading NuScale Power Narratives:

Fair value: US$20.42 per share

Implied upside vs last close: about 42.0% below this fair value

Revenue growth assumption: 119.02% a year

- Analysts frame a thesis around small modular reactor commercialization, with projects like RoPower and ENTRA1 described as key to turning current technology progress into future revenue.

- The narrative highlights NuScale Power's NRC approved SMR design, existing partnerships and a reported liquidity position that is viewed as supportive for funding development and project milestones.

- Risks flagged include long power purchase agreement negotiations, funding uncertainty, supply chain bottlenecks, regulatory timing and dependence on ENTRA1 execution, all of which could affect when and how cash flows arrive.

Fair value: US$0.81 per share

Implied downside vs last close: about 93.2% above this fair value

Revenue growth assumption: 49.16% a year

- This narrative focuses on execution and financing risks, highlighting the ENTRA1 controversy, class action claims, large milestone payment exposure and visible shareholder dilution from capital raising.

- It notes that all reported revenue currently comes from the US utilities segment, with analysts modeling ongoing losses even as they project strong top line growth and a wide spread in future price targets.

- The author describes NuScale Power as a high risk, high potential stock that may need to clear legal and commercialization hurdles and demonstrate that current cash and projects can translate into reactors in operation and sustainable earnings.

To see how these contrasting stories line up with the full set of Community views and live assumptions that feed into fair value, go to the NuScale Power narrative hub and compare them side by side with the See what the community is saying about NuScale Power.

Do you think there's more to the story for NuScale Power? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.