Is NXP Semiconductors (NXPI) Cheap As Raised Guidance Lifts Its Valuation Outlook?

NXP Semiconductors NV NXPI | 0.00 |

NXP Semiconductors (NasdaqGS:NXPI) recently raised its revenue and earnings guidance after quarterly results topped analyst expectations, putting the stock back in focus as investors reassess valuation, growth drivers and risk-reward trade-offs.

Despite the recent guidance upgrade, NXP Semiconductors’ share price has eased, with a 1-month share price return down 7.6% and a 7-day share price return down 1.8%, while the 90-day share price return of 40.1% and 1-year total shareholder return of 23.1% indicate strong underlying momentum.

If NXP’s edge AI push has your attention, it may be worth broadening your watchlist with other semiconductor enablers of this trend through 52 AI infrastructure stocks

After a sharp run over the past quarter and a pullback despite stronger guidance, NXP Semiconductors sits at an interesting crossroads. Is the recent rally already pricing in the edge AI and automotive story, or is there still valuation headroom?

Most Popular Narrative: 10% Undervalued

At a last close of $273.36 versus a narrative fair value of about $303.68, NXP Semiconductors is framed as having a valuation gap that analysts tie to a specific earnings and margin roadmap.

The analysts have a consensus price target of $303.68 for NXP Semiconductors based on their expectations of its future earnings growth, profit margins and other risk factors.

In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $17.0 billion, earnings will come to $4.5 billion, and it would be trading on a PE ratio of 23.9x, assuming you use a discount rate of 11.3%.

Want to see what underpins that fair value for NXP Semiconductors? Revenue, earnings and margins all shift in a way that reshapes the profit base and valuation multiple. Curious which specific assumptions have the biggest impact on that $303.68 figure?

Result: Fair Value of $303.68 (UNDERVALUED)

However, the NXP Semiconductors story could change quickly if competition from China pressures pricing or if the recovery in auto and industrial demand falls short of analyst assumptions.

Another View: Cash Flows Point To A Tighter Picture

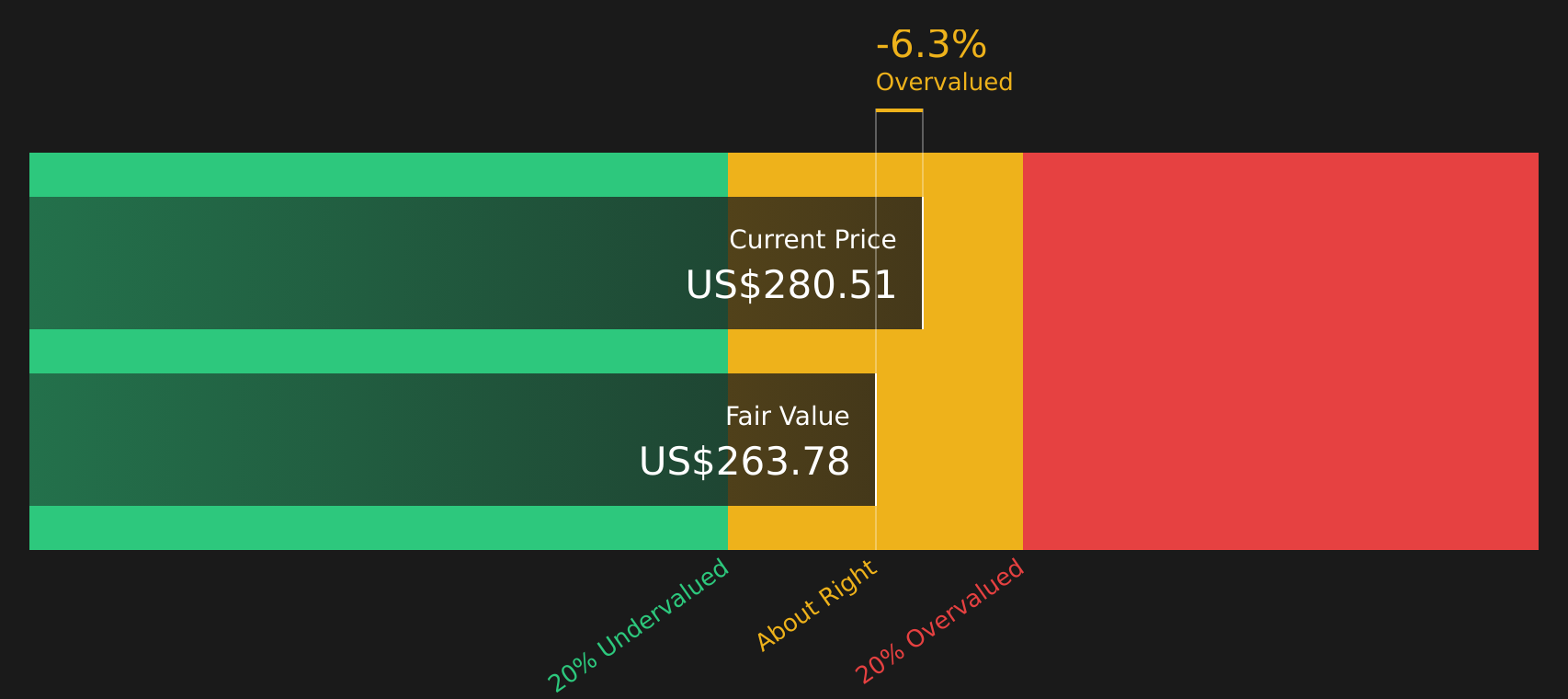

While the fair value narrative for NXP Semiconductors sits around $303.68, our DCF model using future cash flows arrives at about $263.78 per share, which is above the recent $273.36 price. On this view, the stock screens as slightly overvalued rather than 10% undervalued. Which lens feels more realistic to you: the earnings multiple, or the cash flow path?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out NXP Semiconductors for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on fair value and sentiment around both risks and rewards for NXP Semiconductors, it makes sense to review the numbers yourself and move quickly to shape your own view by weighing 4 key rewards and 1 important warning sign

Looking for more investment ideas beyond NXP Semiconductors?

If NXP Semiconductors has sharpened your interest in quality opportunities, do not stop here. Broaden your research now or risk overlooking stocks that better fit your goals.

- Supercharge your hunt for mispriced opportunities by scanning 44 high quality undervalued stocks that combine quality fundamentals with attractive entry points.

- Strengthen your income stream by reviewing 7 dividend fortresses built around higher-yield companies that prioritise consistent shareholder returns.

- Protect your capital by zeroing in on 73 resilient stocks with low risk scores that score well on resilience and financial strength.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.