Is Okta Stock Set for a Turnaround After Recent Cybersecurity Expansion?

Okta, Inc. Class A OKTA | 0.00 |

Thinking about what to do with Okta stock? You’re not the only one. Whether you’re a cautious investor weighing the company’s recent performance, or a growth seeker hoping to catch the next wave, Okta has been on plenty of radars. The last year has seen the share price gain 23.3%, and it’s up 13.0% year-to-date. But zoom out a bit. The three-year gain is an impressive 55.5%, while the five-year return tells another story, down 57.6%. That is quite a journey for any stock and suggests a complex picture where old risks may be fading but other challenges could be lingering.

Recent news surrounding Okta’s push to expand its identity security offerings and strategic moves in the cybersecurity sector has helped shift sentiment, and some investors are interpreting these headlines as signs the company could be turning a corner. This optimism was modestly reflected in a 1.9% rise over the last week, though the stock may still be digesting earlier volatility and a degree of wariness in the broader tech market.

With this backdrop, the big question is still valuation. Is Okta actually undervalued right now, or is the current price justified? Looking at our standard set of six valuation checks, Okta scores a 3, suggesting it is undervalued on half of them. Next up, we will break down exactly what is behind that score, comparing several valuation approaches. Plus, stick around for what might be the most insightful way to judge Okta’s real value at the end of the article.

Approach 1: Okta Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model projects Okta’s future cash flows and then discounts them back to today’s value using an appropriate rate. This approach aims to estimate what the company is truly worth based on its ability to generate future cash, making it a popular method for long-term investors.

For Okta, the current Free Cash Flow stands at $830 Million. Analyst forecasts stretch over the next five years, pointing to steady growth in Okta’s ability to generate cash. Projections indicate that by 2030, annual Free Cash Flow could reach approximately $1.28 Billion, based on a combination of analyst estimates and further extrapolation by Simply Wall St beyond the first five years.

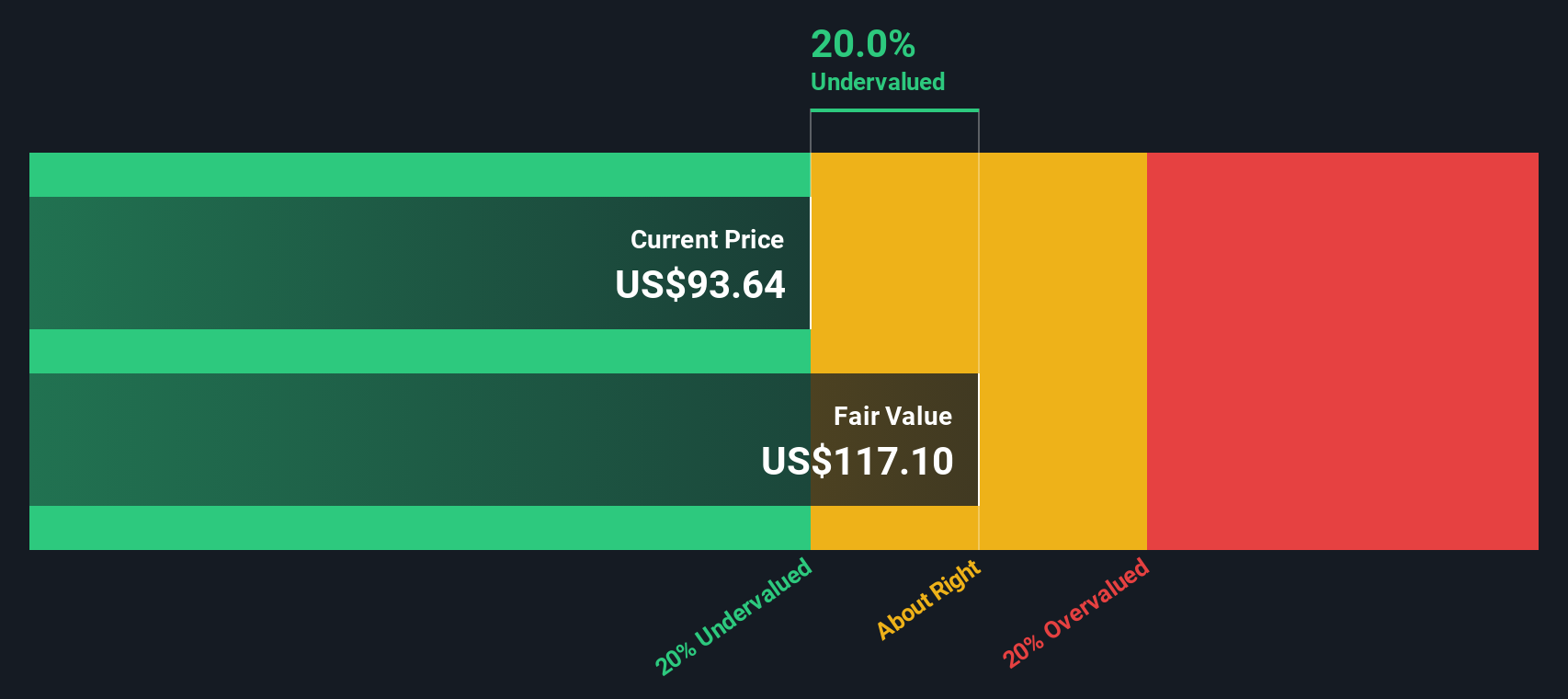

Using DCF, Okta’s intrinsic value is estimated at $116.49 per share. With the stock currently trading at a 23.5% discount to this calculated fair value, the DCF approach suggests Okta may be significantly undervalued at its current share price.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Okta is undervalued by 23.5%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

Approach 2: Okta Price vs Earnings (PE Ratio)

For profitable companies like Okta, the Price-to-Earnings (PE) ratio is often an effective way to assess valuation. PE ratios let investors see how much they are paying for each dollar of current earnings, which is especially meaningful for businesses that have reached or are approaching consistent profitability.

Growth expectations and perceived business risks shape what a "normal" or "fair" PE ratio should be. Generally, companies with strong growth prospects or lower risks command higher PE ratios, while slower-growing or riskier stocks tend to trade at lower multiples.

Okta currently trades at a PE ratio of 93.5x, which is much higher than the IT industry average of 30.1x and also well above the peer group average of 30.8x. At first glance, this might suggest rich pricing compared to typical benchmarks. However, it is important to dig deeper before making a call.

This is where Simply Wall St’s proprietary “Fair Ratio” becomes useful. The Fair Ratio for Okta is calculated as 41.5x, taking into consideration not just peer and industry averages, but also Okta’s own earnings growth, profit margins, industry, market cap, and company-specific risks. This holistic calculation provides a more balanced and realistic benchmark for the company’s true value, beyond surface-level comparisons.

When we compare Okta’s current PE of 93.5x to its Fair Ratio of 41.5x, the market seems to be pricing in significant optimism beyond what the company's fundamentals and risk profile suggest. This means Okta is trading well above what would be considered a fair value based on a full view of its outlook and circumstances.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Okta Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives, a smarter tool that empowers you to connect your own story about Okta with real numbers and future forecasts, creating a more personal, actionable investing view.

A Narrative is a simple, structured story you create about a company, where you combine your assumptions about its future revenue, earnings, profit margins and other factors to arrive at your own fair value estimate. Instead of just looking at static ratios, Narratives let you bring together the numbers you believe in and the reasons behind them, tying Okta’s unique journey, risks, and opportunities directly to the financial outcome you expect.

On Simply Wall St’s platform, in the Community page used by millions, Narratives are easy to use, allowing you to clearly see whether Okta looks undervalued or overvalued by comparing your fair value to the current market price. They update automatically when new information or news arrives, making sure your story always stays relevant and current.

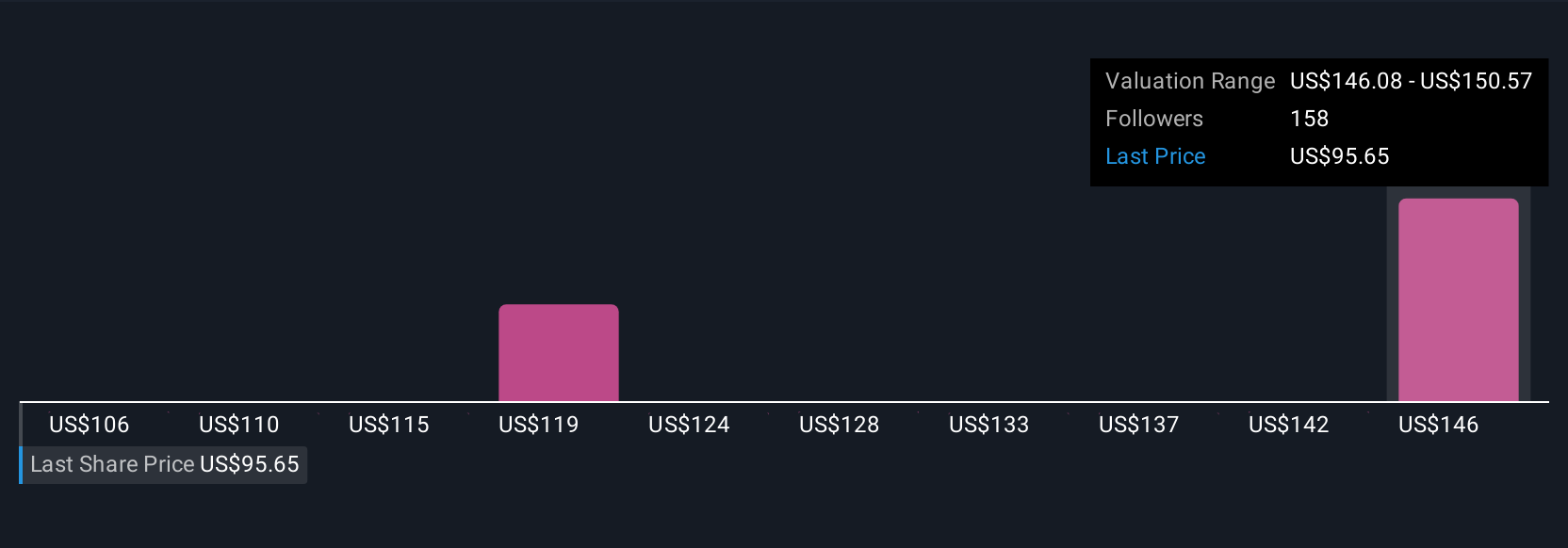

For example, some investors believe Okta’s fair value could be as high as $147.87 due to rapid AI-driven security adoption and margin improvement, while others see greater risks and assign a more cautious value around $75. Narratives help you compare these perspectives, make your own call, and decide with greater confidence when to buy or sell.

Do you think there's more to the story for Okta? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.