Is On Holding (ONON) Still Attractive After Strong Multi Year Share Price Run?

On Holding AG Class A ONON | 33.03 | -5.00% |

- If you are wondering whether On Holding's share price still offers value after a strong run in recent years, the key question is how the current market price lines up with the underlying business.

- The stock last closed at US$49.12, with returns of 4.6% over the past week, 0.7% over the past month, 4.6% year to date, and a 13.3% decline over the past year, while the three year return sits at 137.3%.

- Recent attention on the company has been shaped by ongoing interest in branded athletic footwear and athleisure, as investors weigh how consumer trends could influence premium sportswear demand. This backdrop helps explain why the share price has seen both strong multi year gains and more mixed shorter term moves, as expectations around brand strength and growth potential continue to shift.

- On Holding currently has a valuation score of 1 out of 6. This means it screens as undervalued on only one of six checks. We will look at what traditional valuation tools say, then finish by pointing you to a more complete way to think about the stock's value.

On Holding scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

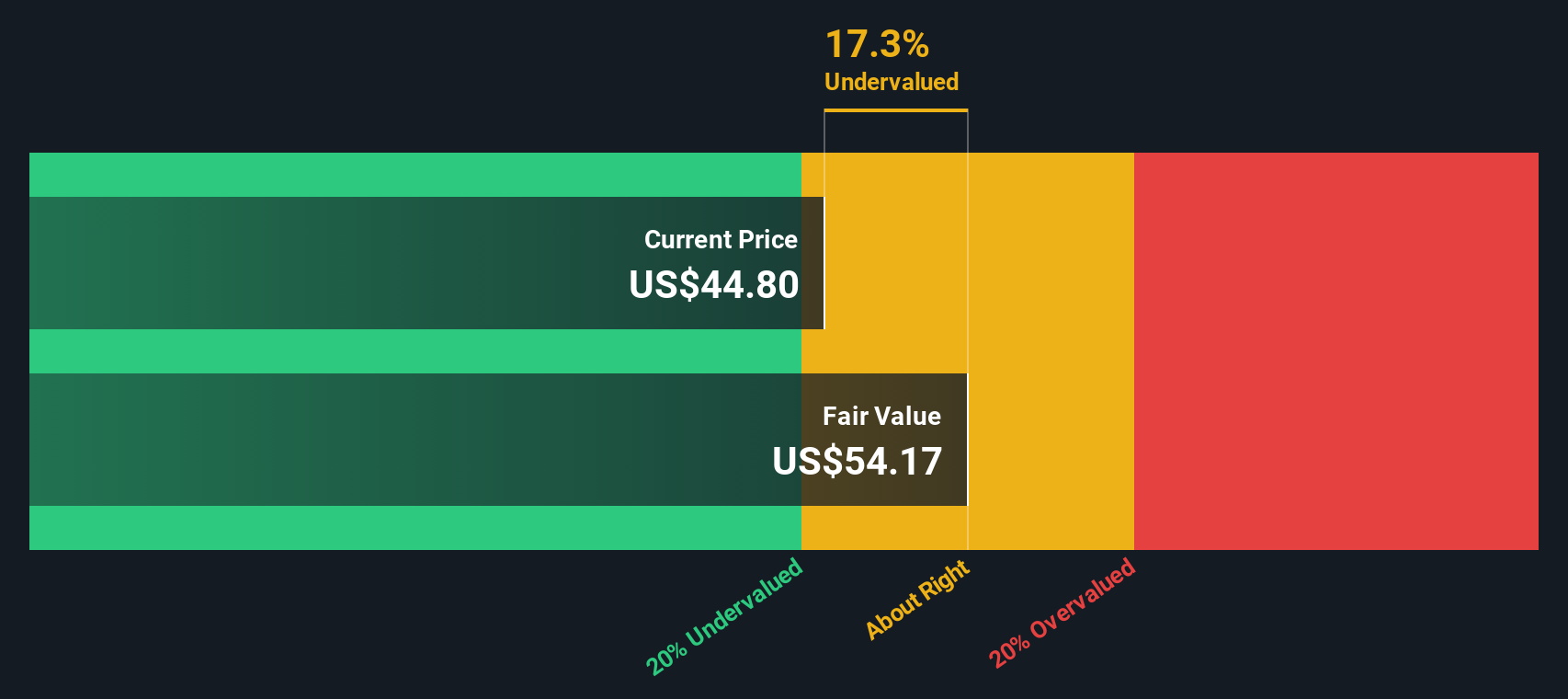

Approach 1: On Holding Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes estimates of a company’s future cash flows and discounts them back to today using a required rate of return. The idea is to estimate what those future CHF cash flows are worth in present terms and compare that figure with the market price.

For On Holding, the model uses last twelve month Free Cash Flow of about CHF 331.7 million, then applies a 2 Stage Free Cash Flow to Equity approach. Analyst inputs cover the earlier years, such as projected Free Cash Flow of CHF 386 million in 2026 and CHF 609 million in 2028, with Simply Wall St extrapolating the remaining years out to 2035. All these projected CHF cash flows are then discounted back and combined to arrive at an intrinsic value per share.

The result is an estimated fair value of US$54.98 per share, compared with the recent share price of US$49.12. That implies the shares trade at about a 10.7% discount to this DCF estimate, which points to the stock screening as undervalued on this model.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests On Holding is undervalued by 10.7%. Track this in your watchlist or portfolio, or discover 880 more undervalued stocks based on cash flows.

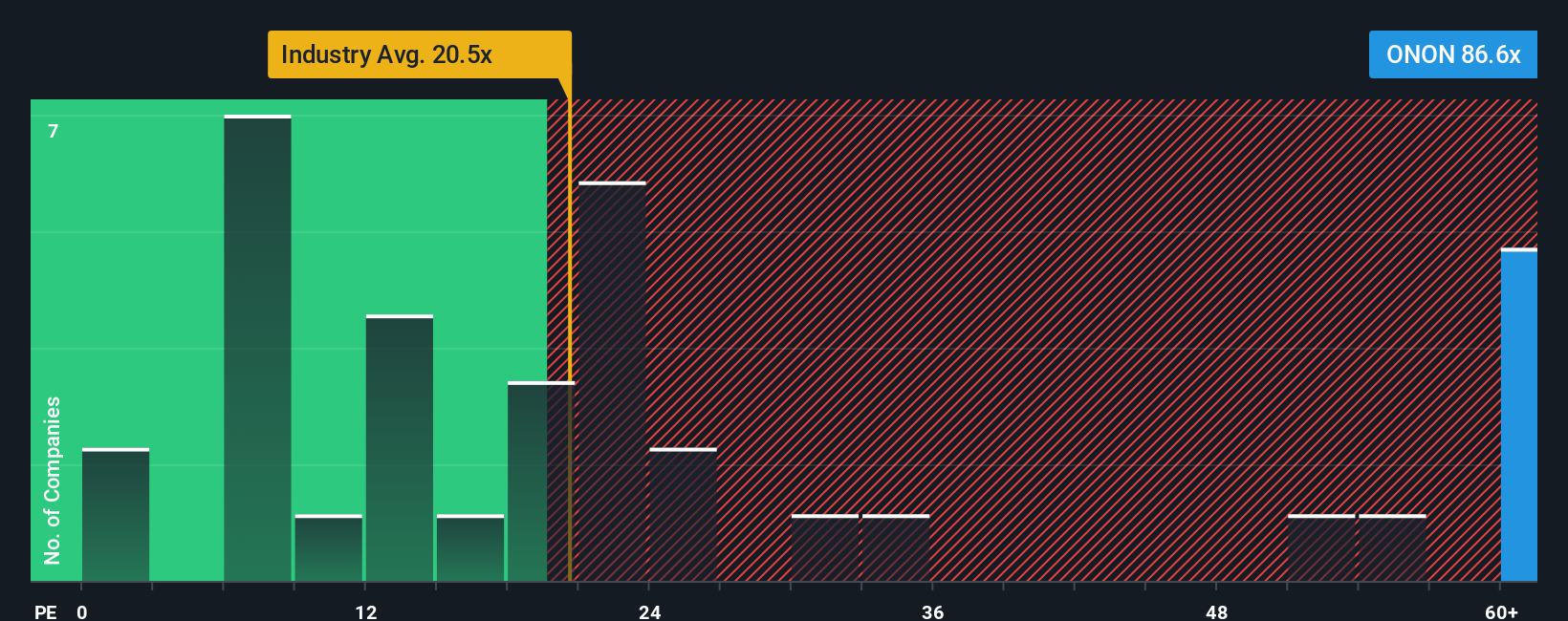

Approach 2: On Holding Price vs Earnings

For profitable companies, the P/E ratio is a useful shorthand because it links what you pay directly to the earnings the business is already generating. It gives you a quick way to see how much the market is willing to pay for each dollar of earnings.

What counts as a “normal” P/E depends on how the market views a company’s growth potential and risk. Higher expected growth or lower perceived risk can justify a higher P/E, while slower growth or higher risk tends to line up with a lower P/E.

On Holding currently trades on a P/E of 58.51x. That sits above the Luxury industry average of 21.24x and also above the peer group average of 29.31x. Simply Wall St’s Fair Ratio for On Holding is 31.03x. This Fair Ratio is a proprietary estimate of what P/E might be reasonable given the company’s earnings growth profile, industry, profit margins, market cap and specific risks.

Because the Fair Ratio builds in those company level factors, it can be more informative than a simple comparison with industry or peer averages. With the current P/E of 58.51x versus a Fair Ratio of 31.03x, the shares screen as trading above this Fair Ratio based metric.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1446 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your On Holding Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives, which are simple stories you build around your own view of On Holding's future revenue, earnings, margins and fair value. You can then connect these directly to a financial forecast and a fair value estimate that you can compare with the current share price to decide whether the stock looks attractive or expensive to you.

On Simply Wall St's Community page, Narratives are an easy tool used by millions of investors, where your story and numbers are linked. When new information such as earnings, guidance or news is added, the fair value you see is refreshed automatically without you needing to rebuild your whole view.

For On Holding, one investor might focus on growth in DTC, international expansion and margin assumptions similar to the higher analyst targets, leading to a fair value closer to the upper end of the recent US$75 range. Another might focus on competition, premium pricing risk and more conservative P/E assumptions, landing nearer the lower end around US$52. Narratives let you see these different viewpoints side by side and decide which aligns more closely with your own expectations.

Do you think there's more to the story for On Holding? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.