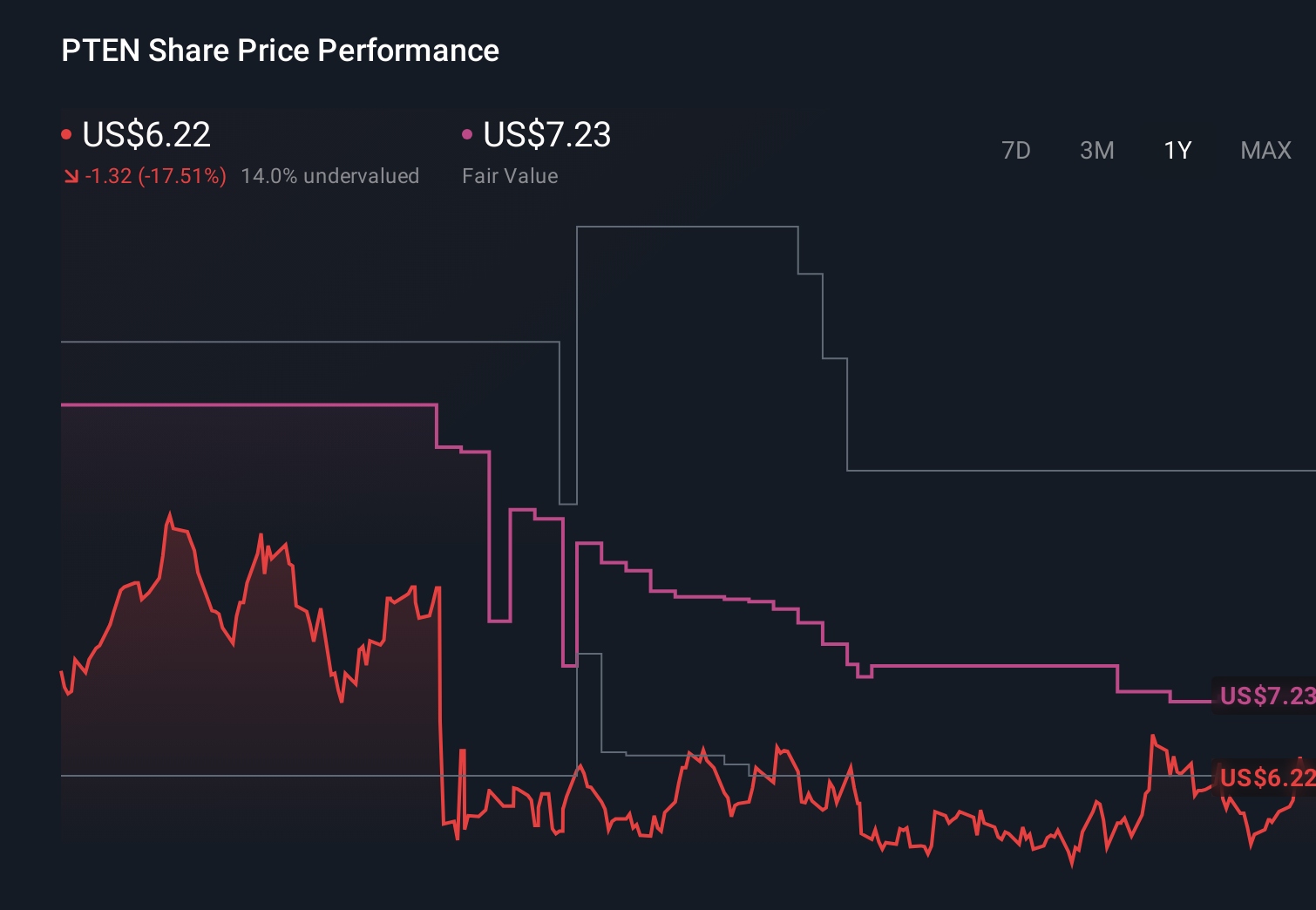

Is Patterson-UTI (PTEN) Quietly Recasting Its Risk Profile With New Debt And Shifting Shareholders?

Patterson-UTI Energy, Inc. PTEN | 0.00 |

- In early May 2026, Patterson-UTI Energy completed a US$499.27 million offering of 6.050% senior unsecured notes due 2036 and extended US$450 million of its revolving credit facility to 2031, reinforcing balance sheet flexibility following a quarter in which earnings and revenue exceeded expectations.

- Alongside these financing moves, a series of routine insider stock sales and equity awards occurred while an affiliate of Blackstone reduced its ownership below 5%, highlighting an ongoing transition in the company’s shareholder base rather than signaling new fundamental information.

- Next, we’ll examine how the stronger liquidity position, underpinned by the 2036 bond issuance, interacts with Patterson-UTI’s existing investment narrative.

This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

Patterson-UTI Energy Investment Narrative Recap

To own Patterson-UTI today, you need to believe its high-spec rigs and integrated completions platform can convert cyclical drilling demand into sustainable cash generation despite recent losses. The new 2036 notes and extended credit facility enhance liquidity, but they do not fundamentally alter the near term catalyst around activity levels and pricing, nor the key risk that ongoing capex and softening customer spending could keep free cash flow under pressure if conditions stay muted.

The most relevant update here is the US$499.27 million 6.050% senior notes due 2036, paired with the extension of US$450 million in revolving commitments to 2031. Together, these financings give Patterson-UTI more time and flexibility to fund its equipment and technology investments that underpin its drilling and completions thesis, while also bridging through potential periods of weaker utilization that could otherwise strain liquidity.

Yet even with this stronger liquidity, investors should be aware that rising capital needs and softer drilling activity could...

Patterson-UTI Energy's narrative projects $4.8 billion revenue and $337.4 million earnings by 2028. This assumes revenue will decline by 1.3% per year and an earnings increase of about $1.4 billion from -$1.1 billion today.

Uncover how Patterson-UTI Energy's forecasts yield a $8.84 fair value, a 24% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming around US$4.8 billion of revenue and US$150 million of earnings by 2029, so this new financing could either reinforce that automation driven upside story or prove those expectations too aggressive, depending on how you see the balance between higher capex and the potential for much stronger margins.

Explore 3 other fair value estimates on Patterson-UTI Energy - why the stock might be worth 39% less than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Patterson-UTI Energy research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Patterson-UTI Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Patterson-UTI Energy's overall financial health at a glance.

Ready For A Different Approach?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 19 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.