Is PDD Holdings (PDD) Pricing In Recent Share Price Weakness Or Longer Term Growth Prospects

PINDUODUO INC. PDD | 0.00 |

- This article considers whether PDD Holdings, at around US$107 per share, is priced for opportunity or already reflects its current story by examining what the market price may be implying about its value.

- The stock has had a mixed run, with a 7.1% return over the past year and longer-term 3-year returns of 19.1%. However, a 7.2% decline year to date and an 11.7% fall over the last week hint at shifting sentiment and changing perceptions of risk.

- Recent attention on PDD Holdings has centered on its position in global e-commerce and competition with other major online platforms. Investors have been reacting to headlines around its business momentum and debates over market share. These developments help explain why the share price has been active recently and why opinions on its long-term potential may be divided.

- In this context, PDD Holdings currently scores 6 out of 6 on our valuation checks. This sets up a closer look at how different models assess its value today and points to a broader way of thinking about valuation that we will return to at the end of this article.

Approach 1: PDD Holdings Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a business could be worth by projecting its future cash flows and then discounting them back to today to reflect risk and the time value of money.

For PDD Holdings, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month free cash flow is CN¥111.4b. Analysts provide estimates out to 2027, with Simply Wall St extrapolating further. Within these projections, free cash flow for 2026 is CN¥138.5b and CN¥164.6b for 2027, with ten year projections extending up to around CN¥276.3b in 2035, all expressed in nominal terms before discounting.

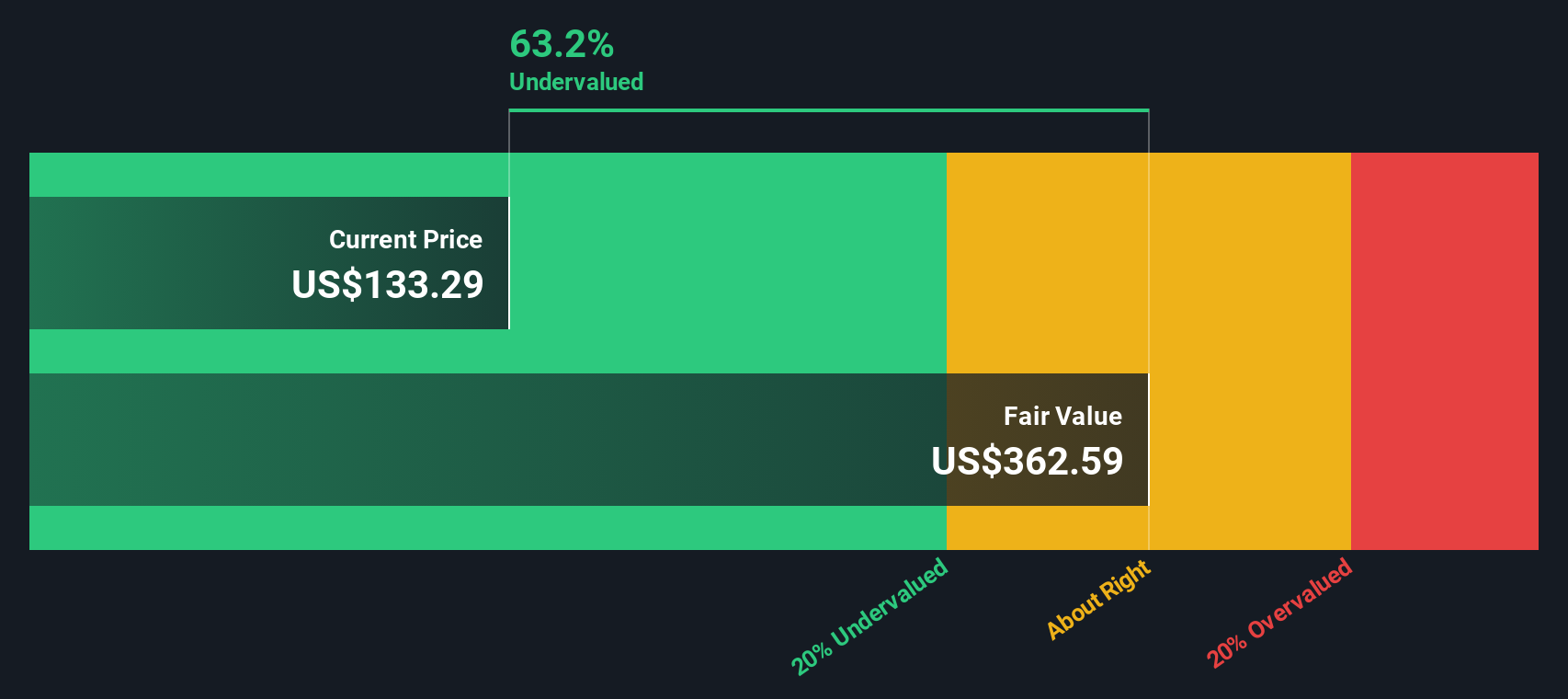

After discounting these projected cash flows, the DCF output points to an estimated intrinsic value of about US$349.09 per share, compared with the current share price of roughly US$107. Based on this model, the implied discount of 69.2% indicates that the shares are priced below the DCF estimate.

Result: UNDERVALUED (based on this DCF model)

Our Discounted Cash Flow (DCF) analysis suggests PDD Holdings is undervalued by 69.2%. Track this in your watchlist or portfolio, or discover 867 more undervalued stocks based on cash flows.

Approach 2: PDD Holdings Price vs Earnings

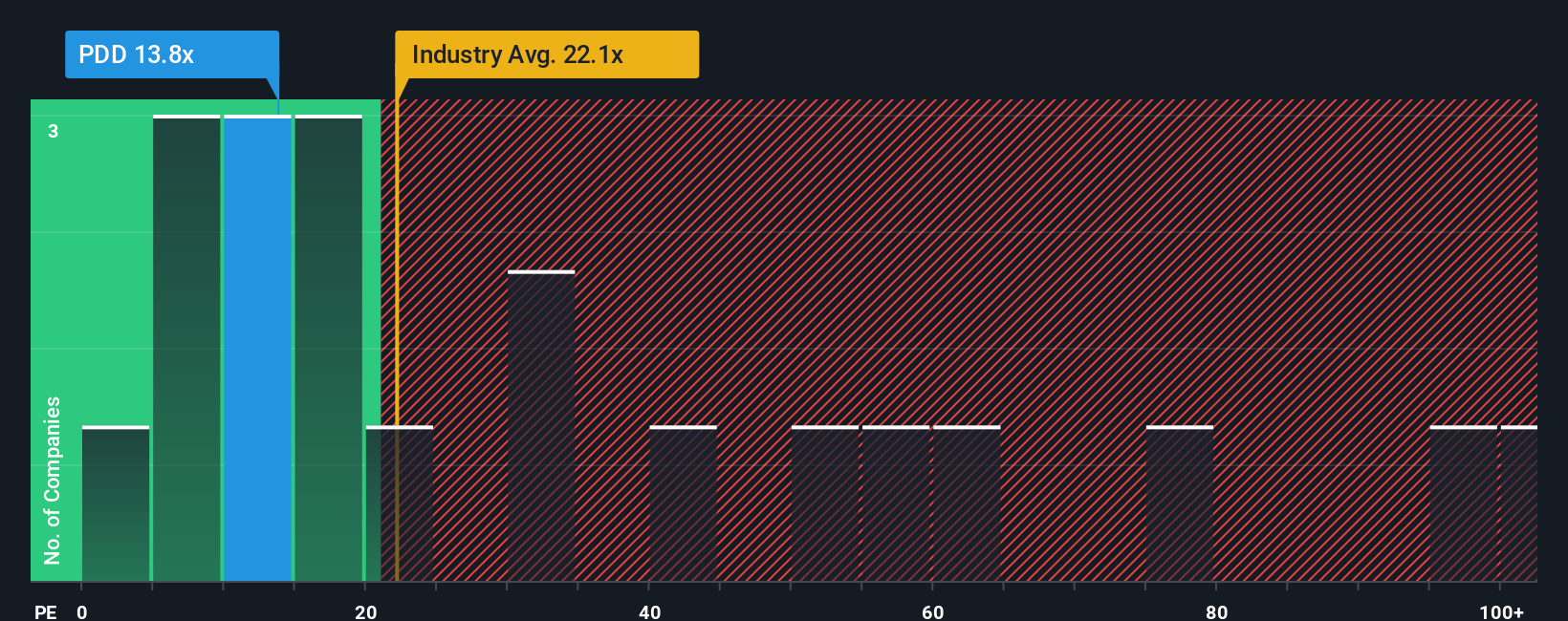

For a profitable company, the P/E ratio is a straightforward way to connect what you pay for each share with the earnings that support it. Investors usually accept a higher P/E if they expect stronger growth or see the earnings as relatively resilient, and a lower P/E if they see more risk, slower growth, or less predictable earnings.

PDD Holdings currently trades on a P/E of 10.39x. That sits below the Multiline Retail industry average P/E of 20.04x and well below the peer group average of 55.94x. On the surface, that gap suggests the market is placing a lower value on each dollar of PDD Holdings earnings than it does for many peers.

Simply Wall St introduces a Fair Ratio of 25.57x, which is its view of what a more appropriate P/E might be after accounting for factors like the company’s earnings growth profile, industry, profit margins, market cap and key risks. This is more tailored than a simple comparison against peers or the industry because those broad benchmarks do not reflect PDD Holdings specific characteristics. Comparing the Fair Ratio of 25.57x with the current P/E of 10.39x indicates that the shares are trading below that model-based assessment.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1440 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your PDD Holdings Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which are simple stories you create about a company that link your view of its future revenues, earnings and margins to a financial forecast and then to a fair value that you can compare with today’s share price.

On Simply Wall St’s Community page, Narratives are an accessible tool used by millions of investors that let you turn your assumptions into numbers, so you can see whether your fair value suggests the stock is expensive or cheap relative to the current price and quickly spot when that gap widens or closes.

Narratives also update as new information such as earnings or news is added, so you are not locked into a static model. You can also see how other investors’ stories differ. For example, one PDD Holdings Narrative currently assumes a fair value of US$117.02 while another assumes US$176.36. These reflect very different views about how its global commerce business could develop and what multiples might be appropriate.

Do you think there's more to the story for PDD Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.