Is PG&E Virtual Power Plant Momentum Recasting the Grid Services Investment Case For Sunrun (RUN)?

Sunrun Inc. RUN | 0.00 |

- In early June 2026, Sunrun reported first-quarter results that exceeded analyst revenue expectations, while co-founder Lynn Jurich sold 50,000 shares under a pre-arranged Rule 10b5-1 plan and Pacific Gas and Electric announced that more than 1 million customer solar systems are now connected to its grid, including virtual power plant projects using Sunrun’s solar-plus-storage units to ease local constraints.

- Together, these developments underscore Sunrun’s expanding role in grid services and distributed energy, even as investor sentiment remains sensitive to macroeconomic inflation and interest rate concerns.

- We’ll now examine how Sunrun’s expanding virtual power plant work with PG&E may influence the company’s investment narrative around grid services.

The latest GPUs need a type of rare earth metal called Neodymium and there are only 29 companies in the world exploring or producing it. Find the list for free.

Sunrun Investment Narrative Recap

To own Sunrun, you need to believe residential solar plus storage and grid services can remain attractive even when incentives fade and financing is more expensive. Right now, the key near term catalyst is the company’s ability to grow higher margin grid services, while the biggest risk is tighter credit and higher rates increasing funding costs. The latest CPI driven share pullback reflects that risk but does not appear to change the core grid services thesis.

The most relevant development is PG&E’s milestone of 1 million customer solar systems connected to its grid, including virtual power plant projects using Sunrun units. This directly ties into Sunrun’s grid services catalyst by showing real world deployment of its solar plus storage fleet for local grid relief, which may strengthen the case for recurring services revenue if similar programs expand or deepen over time.

Yet the real issue investors should be watching is how prolonged higher interest rates could affect Sunrun’s ability to fund new systems and...

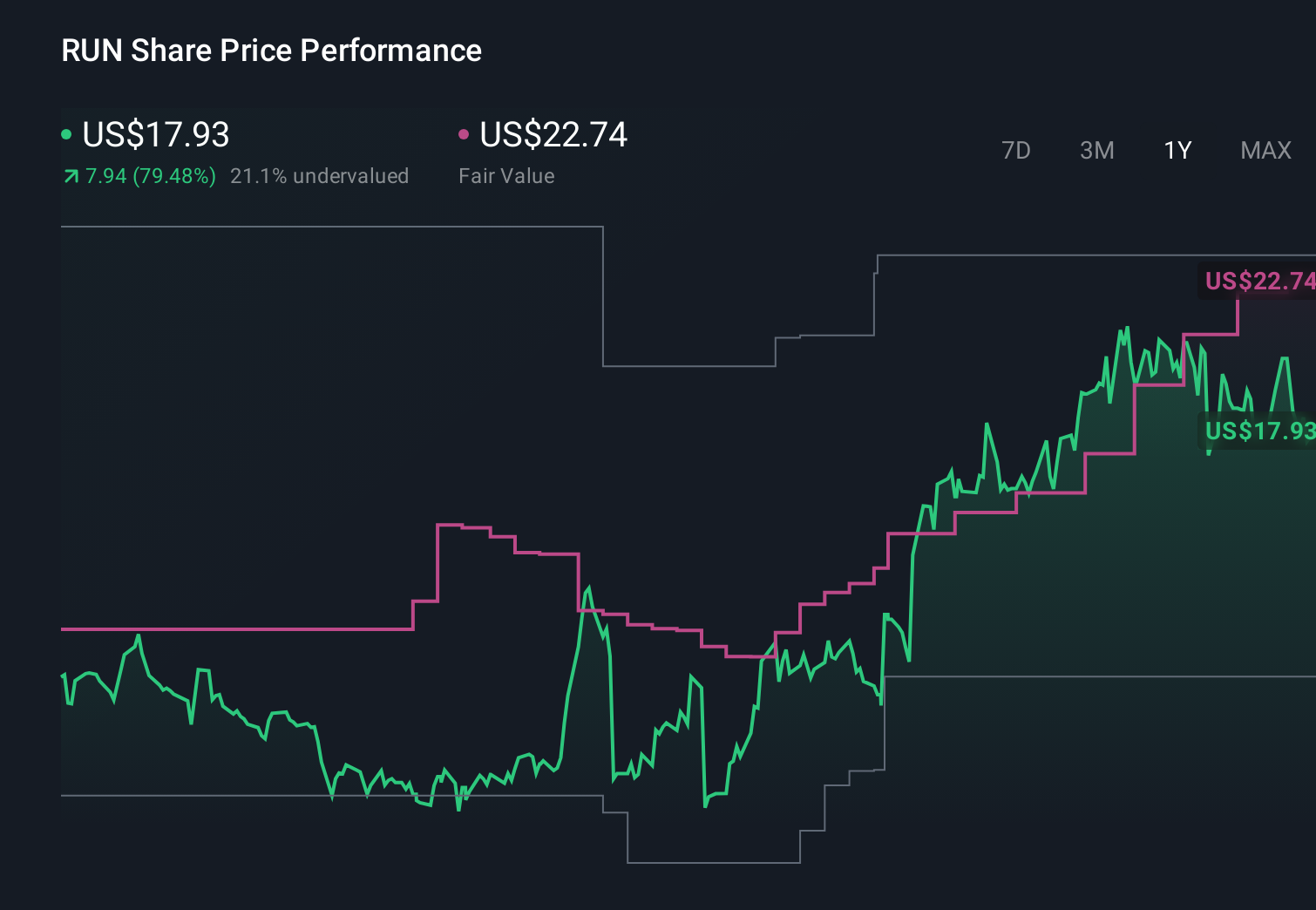

Sunrun's narrative projects $3.7 billion revenue and $56.5 million earnings by 2029. This requires 8.0% yearly revenue growth and a $391.1 million earnings decrease from $447.6 million today.

Uncover how Sunrun's forecasts yield a $19.67 fair value, a 53% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were expecting Sunrun’s revenue to reach about US$4.9 billion and earnings US$1.1 billion by 2029, which is a far more bullish story than the consensus view and could be challenged or reinforced by inflation and rate driven volatility in the stock that we are seeing now.

Explore 3 other fair value estimates on Sunrun - why the stock might be worth over 2x more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Sunrun research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Sunrun research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Sunrun's overall financial health at a glance.

Interested In Other Possibilities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.