Is Phibro Animal Health’s (PAHC) Efficiency Surge Quietly Rewriting Its Competitive Position in Animal Health?

Phibro Animal Health Corporation Class A PAHC | 55.66 55.66 | +1.31% 0.00% Post |

- In recent years, Phibro Animal Health has reported annual revenue growth of 21.7% alongside higher operating profits and efficiency, pointing to stronger execution in its animal health portfolio.

- This combination of faster sales expansion and better cost leverage suggests Phibro has been gaining share and improving how effectively it converts revenue into profit.

- Now we’ll examine how this improved operating performance may reshape Phibro Animal Health’s existing investment narrative and future expectations.

Find 55 companies with promising cash flow potential yet trading below their fair value.

Phibro Animal Health Investment Narrative Recap

To own Phibro Animal Health, you need to believe its animal health portfolio can keep converting sales into profit efficiently while managing its reliance on medicated feed additives. The recent 21.7% annual revenue growth and stronger operating leverage support that belief in the near term, but they also sharpen the key short term question: how sustainable are these gains if regulatory or competitive pressure builds around its core MFA business?

Among recent announcements, the February 4, 2026 guidance stands out alongside the latest results, as it frames expectations around the stronger revenue and profit trends now visible. With FY2026 net sales guided to US$1.45 billion to US$1.50 billion and net income to US$85 million to US$95 million, the company is effectively anchoring how investors think about the payoff from better execution and the integration of acquired products in the next year or so.

Yet beneath the improving margins, investors should be aware that heavy dependence on medicated feed additives still leaves Phibro exposed to...

Phibro Animal Health's narrative projects $1.5 billion revenue and $119.1 million earnings by 2028. This requires 6.1% yearly revenue growth and a $70.8 million earnings increase from $48.3 million.

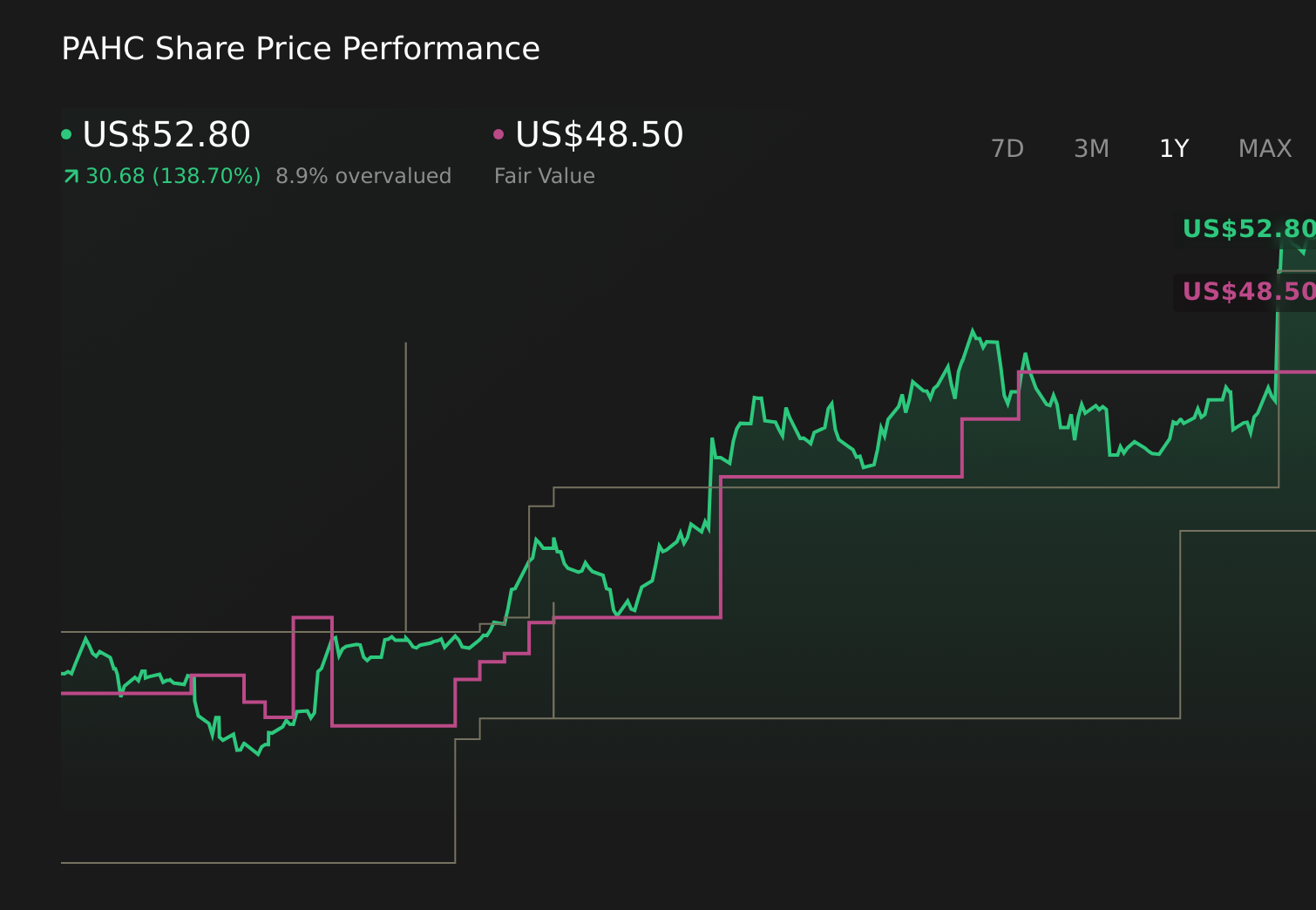

Uncover how Phibro Animal Health's forecasts yield a $48.50 fair value, a 15% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming revenue of about US$1.6 billion and earnings of roughly US$154.7 million by 2029, so this latest profitability news could either reinforce their faster growth and margin expansion story or prompt you to question whether that upside view underestimates risks like long term pressure on medicated feed additives.

Explore 3 other fair value estimates on Phibro Animal Health - why the stock might be worth less than half the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Phibro Animal Health research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Phibro Animal Health research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Phibro Animal Health's overall financial health at a glance.

Want Some Alternatives?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- AI is about to change healthcare. These 36 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with 29 elite penny stocks that balance risk and reward.

- Rare earth metals are the new gold rush. Find out which 26 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.