Is Plains GP Holdings (PAGP) Still Attractive After Its 52% One Year Share Price Gain

Plains GP Holdings LP Class A PAGP | 0.00 |

- Wondering whether Plains GP Holdings is still reasonably priced after its strong run, or if expectations have gone too far? This breakdown will help you frame the stock's current value against its fundamentals.

- The stock last closed at US$24.23, with returns of 3.6% over 7 days, 0.7% over 30 days, 24.8% year to date and 52.0% over the past year, plus 128.0% over 3 years and 247.1% over 5 years.

- Recent coverage has focused on Plains GP Holdings as an established player in the midstream energy space, with attention on how it is positioned within the broader oil and gas infrastructure system. This context is important when you think about whether the current share price still reflects the risks and opportunities tied to that role.

- On Simply Wall St's 6 point valuation checklist, Plains GP Holdings scores 5. The next step is to walk through the key valuation methods investors typically use and then finish with one way to pull those methods together into a clearer overall view of value.

Approach 1: Plains GP Holdings Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model looks at the cash Plains GP Holdings is expected to generate in the future and then discounts those cash flows back to today to estimate what the business could be worth now.

For Plains GP Holdings, the latest twelve month free cash flow is about $2.44b. Analysts have provided free cash flow estimates out to 2030, with Simply Wall St extending the projections further to 2035 using its own assumptions. The model used here is a 2 Stage Free Cash Flow to Equity approach, which applies one pattern of cash flows for the earlier years and a different pattern for the later years, all in dollar terms.

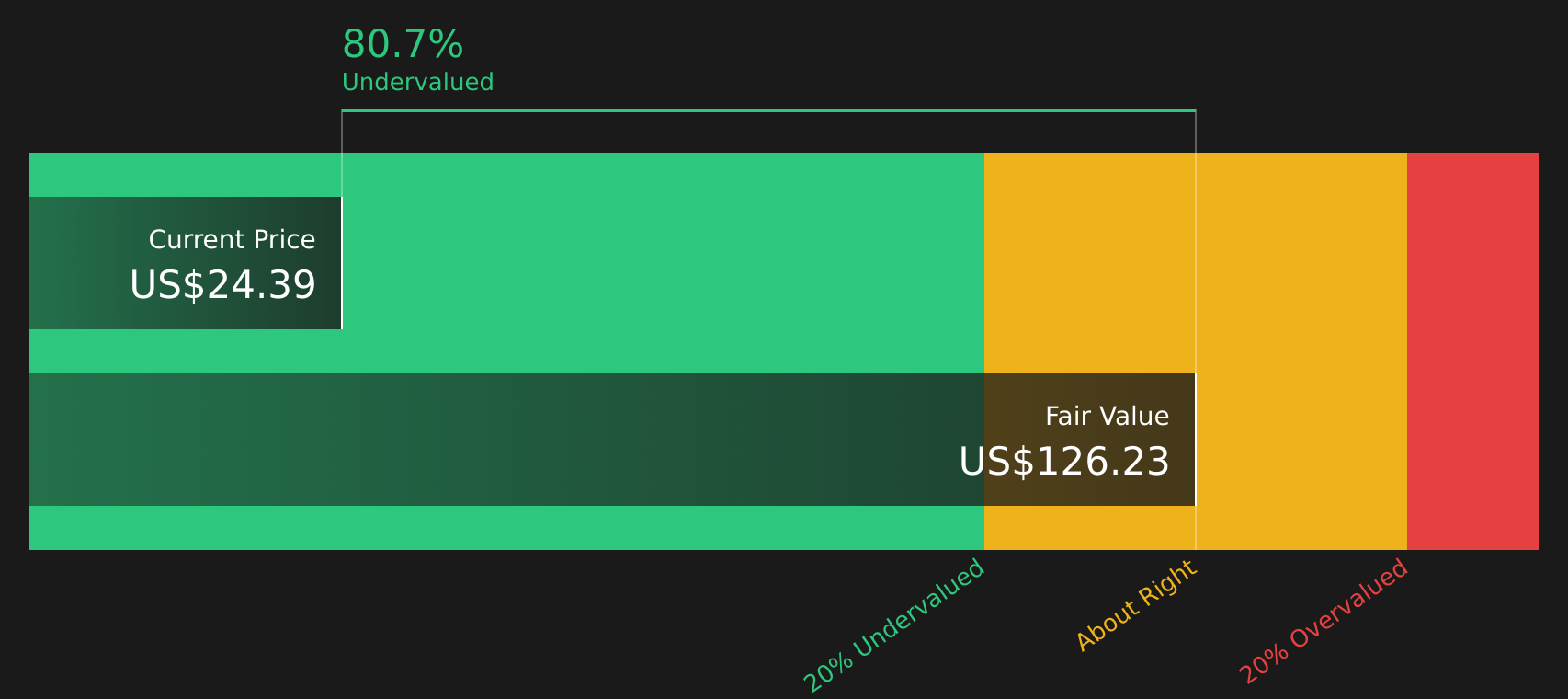

After discounting each projected year of cash flow back to today, the model arrives at an estimated intrinsic value of roughly $109.80 per share. Compared with the recent share price of $24.23, this implies a 77.9% discount, which indicates that Plains GP Holdings stock appears significantly undervalued on this DCF view.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Plains GP Holdings is undervalued by 77.9%. Track this in your watchlist or portfolio, or discover 48 more high quality undervalued stocks.

Approach 2: Plains GP Holdings Price vs Sales

For companies that generate meaningful revenue, the P/S ratio is a useful cross check because it compares what the market is paying for each dollar of sales. It tends to be less affected by short term swings in earnings, which can make it helpful when profits are volatile or influenced by accounting items.

In general, higher growth expectations and lower perceived risk can support a higher P/S multiple, while slower growth or higher risk usually correspond with a lower multiple. That is why it is common to compare a stock's P/S to its industry average and to close peers.

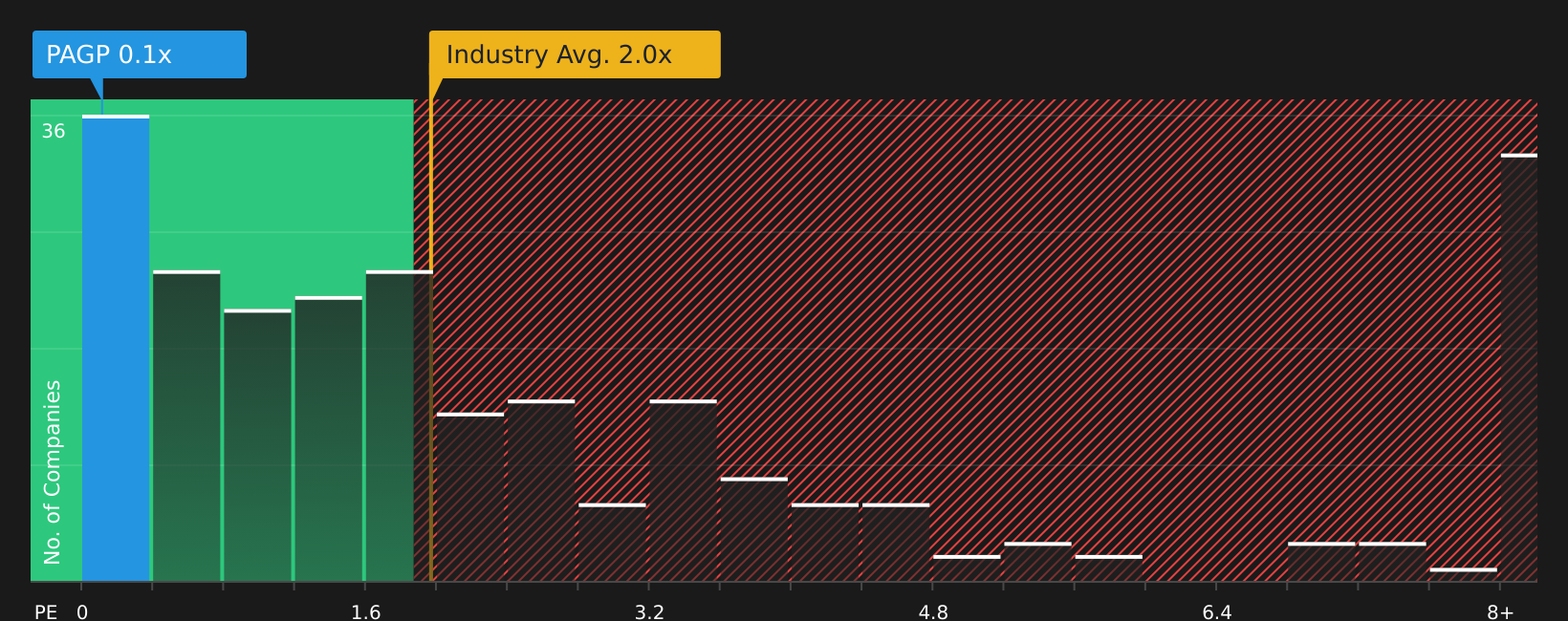

Plains GP Holdings currently trades on a P/S of 0.11x, compared with an Oil and Gas industry average of 2.15x and a peer average of 6.73x. Simply Wall St also calculates a Fair Ratio of 0.72x, which is an estimate of the P/S that might be expected given factors such as earnings growth, profit margins, size and risk profile. Because this Fair Ratio adjusts for these company specific drivers, it can provide a more tailored benchmark than broad industry or peer comparisons. The current 0.11x P/S sits below the 0.72x Fair Ratio, so Plains GP Holdings appears undervalued on this P/S view.

Result: UNDERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 17 top founder-led companies.

Upgrade Your Decision Making: Choose your Plains GP Holdings Narrative

Earlier the article mentioned that there is an even better way to think about valuation, and that is through Narratives, which are simply your story about Plains GP Holdings linked directly to a set of numbers like future revenue, earnings, margins and a fair value estimate.

On Simply Wall St, Narratives live in the Community page and let you set out your view in plain language. You can then tie that view to a financial forecast and a fair value that you can compare with the current share price to help you decide whether you see the stock as priced above or below your expectations.

Narratives update automatically when new information comes in, such as earnings or news, so your fair value stays aligned with the latest data rather than a static spreadsheet you built months ago.

For Plains GP Holdings, one investor might build a bullish Narrative around a fair value close to US$26.00. Another might lean on a more cautious Narrative nearer US$17.00, and seeing these side by side can help you decide which story and set of assumptions you find more reasonable for your own decision making.

For Plains GP Holdings, however, we will make it really easy for you with previews of two leading Plains GP Holdings Narratives:

Fair value in this bullish narrative: US$26.00 per share

Implied pricing vs this fair value: Plains GP Holdings trades at around 6.8% below this narrative fair value based on the last close of US$24.23

Revenue growth assumption: 4.95% per year

- Assumes steady revenue growth with profit margins roughly doubling over the next few years, lifting earnings per share to US$1.71 by around 2028.

- Views the extensive pipeline network, fee based contracts and higher credit rating as positives that support higher quality cash flows and optionality for acquisitions or buybacks.

- Accepts exposure to oil demand, regulation and Permian concentration as risks, but sees them as manageable within a US$26.00 fair value estimate using a 10.0% discount rate.

Fair value in this more cautious narrative: US$22.57 per share

Implied pricing vs this fair value: Plains GP Holdings trades at around 7.4% above this narrative fair value based on the last close of US$24.23

Revenue growth assumption: 4.16% per year

- Assumes moderate revenue growth and margin improvement with earnings per share reaching US$2.02 by about 2029, but applies a P/E of 14.6x that sits closer to the wider US Oil and Gas sector.

- Sees the focus on crude oil, fee based contracts and balance sheet work as supportive for cash flow, yet flags higher reliance on crude volumes and contract resets as ongoing headwinds.

- Frames the consensus fair value of US$22.57 as implying the stock is nearer to fairly priced, with upside and downside risks tied to how crude demand, regulation and capital allocation actually play out.

Used together, these Narratives give you a practical range for thinking about Plains GP Holdings, from a higher conviction upside case to a more conservative fair value view, so you can decide which set of assumptions fits closest to your own expectations.

Do you think there's more to the story for Plains GP Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.