Is Planet Labs (PL) Stock’s Triple Digit Gain Still Supported By Fundamentals

Planet Labs PBC PL | 0.00 |

- If you are wondering whether Planet Labs PBC’s soaring share price still lines up with the underlying business, you are in the right place for a closer look at what that could mean for value.

- The stock has had a mixed recent run, with a 0.6% decline over the last 7 days and a 14.9% decline over the last 30 days, while still showing a 6.1% gain year to date and a 254.3% return over the last year, along with a 347.3% return over the last 3 years.

- These moves sit against a backdrop of ongoing interest in Earth observation and data services, where investors often weigh growth potential against the risks that come with relatively young listed companies. That mix of enthusiasm and caution is a useful backdrop as we look more closely at how the market is currently pricing Planet Labs PBC.

- On our simple valuation checklist, Planet Labs PBC scores 0 out of 6, as shown in the valuation score. Next, we will walk through the usual valuation methods, then finish with a different way of thinking about value that can help tie all those numbers together.

Planet Labs PBC scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

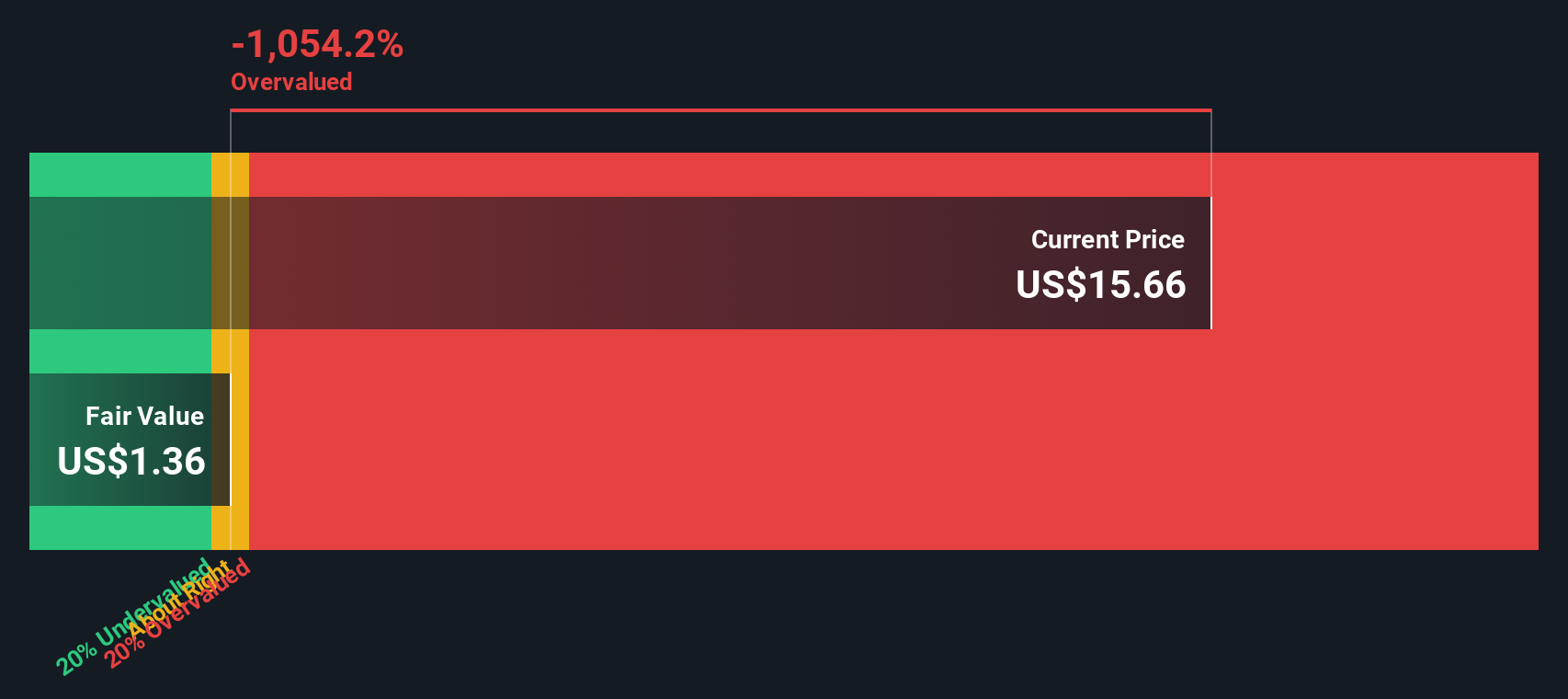

Approach 1: Planet Labs PBC Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model looks at the cash Planet Labs PBC is expected to generate in the future, then discounts those projected cash flows back to today to estimate what the business might be worth right now.

For Planet Labs PBC, the model uses a 2 Stage Free Cash Flow to Equity approach, based on cash flow projections in $. The latest twelve month free cash flow is about $46.8 million, and analysts and extrapolated estimates point to free cash flow of about $36.4 million in 2035, with interim projections such as $23.6 million in 2026 and $40.0 million in 2028. Simply Wall St only uses direct analyst estimates for the nearer years, then extends the trend further out to complete the 10 year path.

Pulling those discounted projections together, the DCF model arrives at an estimated intrinsic value of about $2.08 per share. Compared with the current share price, the model suggests the stock is very expensive, with an implied overvaluation of roughly 941.5%.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Planet Labs PBC may be overvalued by 941.5%. Discover 51 high quality undervalued stocks or create your own screener to find better value opportunities.

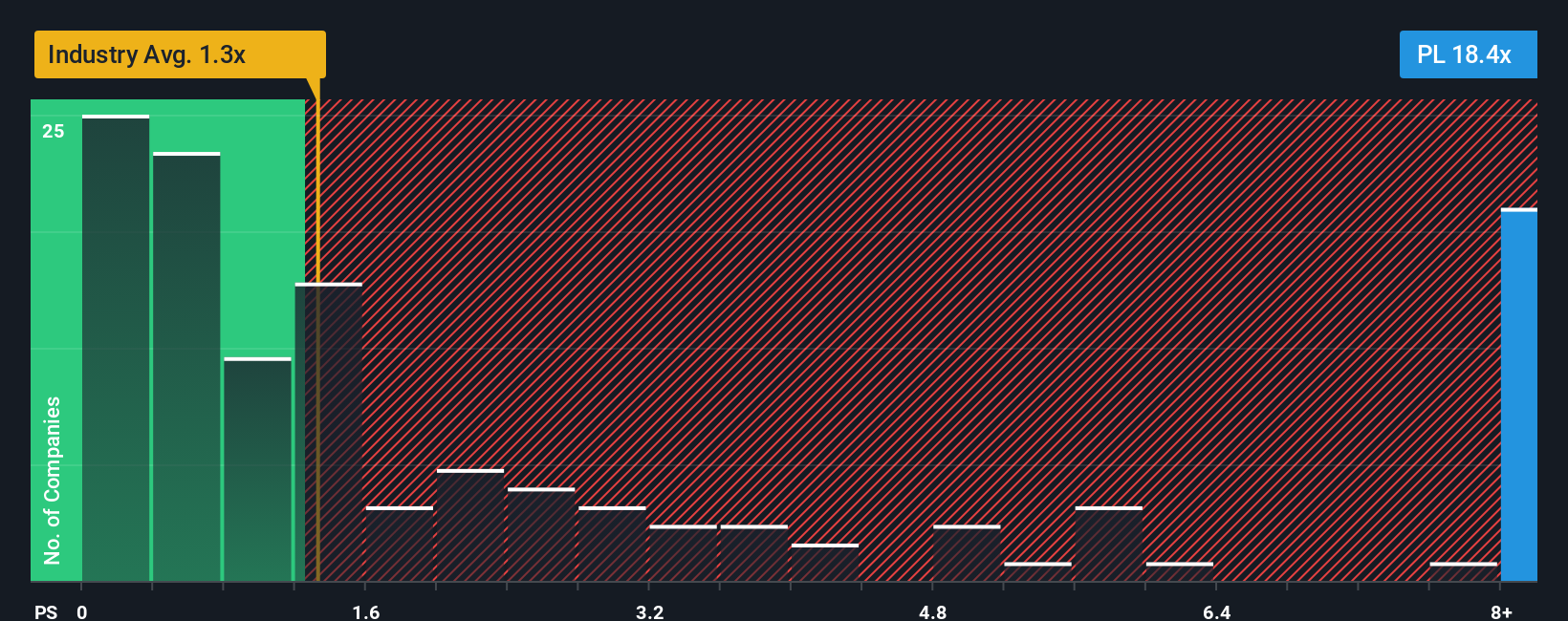

Approach 2: Planet Labs PBC Price vs Sales

For companies where earnings are not yet a clear guide, the P/S ratio is often a practical way to think about value, because it compares what investors pay with the revenue the business is already generating.

In general, higher growth expectations and lower perceived risk can justify a higher P/S multiple, while slower growth or higher risk usually lines up with a lower, more conservative multiple. So the question for you is whether the current P/S properly reflects Planet Labs PBC’s profile.

Planet Labs PBC currently trades on a P/S of 26.14x. That is well above the Professional Services industry average of 1.06x, and also above the peer group average of 0.86x. Simply Wall St’s Fair Ratio framework estimates a P/S of 6.07x for Planet Labs PBC, based on factors such as its growth outlook, industry, profit margins, market cap and key risks. This Fair Ratio can be more informative than a simple comparison with peers or the broader industry, because it adjusts for the company’s own characteristics rather than assuming all businesses deserve similar multiples. Compared with this Fair Ratio, the current 26.14x P/S points to a rich valuation.

Result: OVERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 22 top founder-led companies.

Upgrade Your Decision Making: Choose your Planet Labs PBC Narrative

Earlier we mentioned that there is an even better way to think about valuation. Let us introduce Narratives, which let you attach a simple story about a company to your own numbers on future revenue, earnings, margins and fair value. You can then compare that Fair Value with the current price to help decide whether to buy, hold or sell, all within Simply Wall St’s Community page where Narratives are kept up to date as new news or earnings arrive. For Planet Labs PBC you might see one Narrative with a Fair Value of US$4.50 and another at US$33.00, reflecting very different views on contracts, regulation and long term economics, and you can decide which story and set of assumptions feels closer to your own view.

For Planet Labs PBC however we'll make it really easy for you with previews of two leading Planet Labs PBC Narratives:

Fair value: US$33.00 per share

Current price vs this fair value: roughly 52% below the bull fair value estimate

Revenue growth assumption: 29.25%

- Sees Planet as a critical data infrastructure provider, with recurring, higher margin revenue from AI driven analytics and broader adoption across security, agriculture and energy customers.

- Highlights multi year government and sovereign contracts, new satellite constellations and a growing backlog as support for longer term earnings power and revenue visibility.

- Flags meaningful risks around regulation, government contract dependence, capital intensive satellite launches and rising competition that could pressure margins and free cash flow if things do not go to plan.

Fair value: US$11.31 per share

Current price vs this fair value: roughly 91% above the bear fair value estimate

Revenue growth assumption: 30%

- Focuses on Planet’s leading satellite constellation and exposure to demand for Earth observation and geospatial data from both companies and governments.

- Emphasizes how lower launch and computing costs, plus advances in CubeSats and AI, increase the usefulness of Planet’s data but also frame expectations that are already reflected in the valuation.

- Views the share price as relying heavily on faster commercial adoption of Earth observation solutions, even though government contracts and a solid balance sheet provide some support on the downside.

You can use these two narratives as reference points, then adjust the assumptions to match your own view on Planet Labs PBC’s contracts, capital needs and long term earnings power.

Do you think there's more to the story for Planet Labs PBC? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.