Is PMI’s Smoke Free Focused CFO Appointment Reframing The Investment Case For Philip Morris International (PM)?

Philip Morris International Inc. PM | 0.00 |

- Earlier this month, Philip Morris International’s board approved the appointment of Europe Region President Massimo Andolina as Group Chief Financial Officer, effective August 1, 2026, with current CFO Emmanuel Babeau moving to a strategic advisor role through March 31, 2027 to support the transition.

- The move places a long-time architect of PMI’s smoke-free push and European transformation at the center of capital allocation and financial decision-making, aligning the finance function more closely with the company’s smoke-free ambitions.

- We’ll now examine how elevating a smoke-free and Europe-focused leader to the CFO role could reshape Philip Morris International’s investment narrative.

Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

Philip Morris International Investment Narrative Recap

To own Philip Morris International today, you need to believe its shift toward smoke free products can offset pressure on traditional cigarettes and regulatory uncertainty, particularly in Europe. The CFO transition itself does not materially change that near term, but it does matter for execution risk around capital allocation at a time when smoke free growth and tighter EU rules on novel nicotine products are front and center.

In that context, the upcoming dbAccess Global Consumer Conference, where CEO Jacek Olczak will highlight that smoke free products already contribute 43% of net revenue, feels especially relevant. It will give investors a clearer read on how PMI sees regulation, Europe’s role, and capital priorities evolving ahead of Massimo Andolina’s move into the CFO seat and amid questions about valuation and smoke free growth durability.

Yet beneath the smoke free progress, investors still need to be aware of mounting EU regulatory proposals and how they could affect...

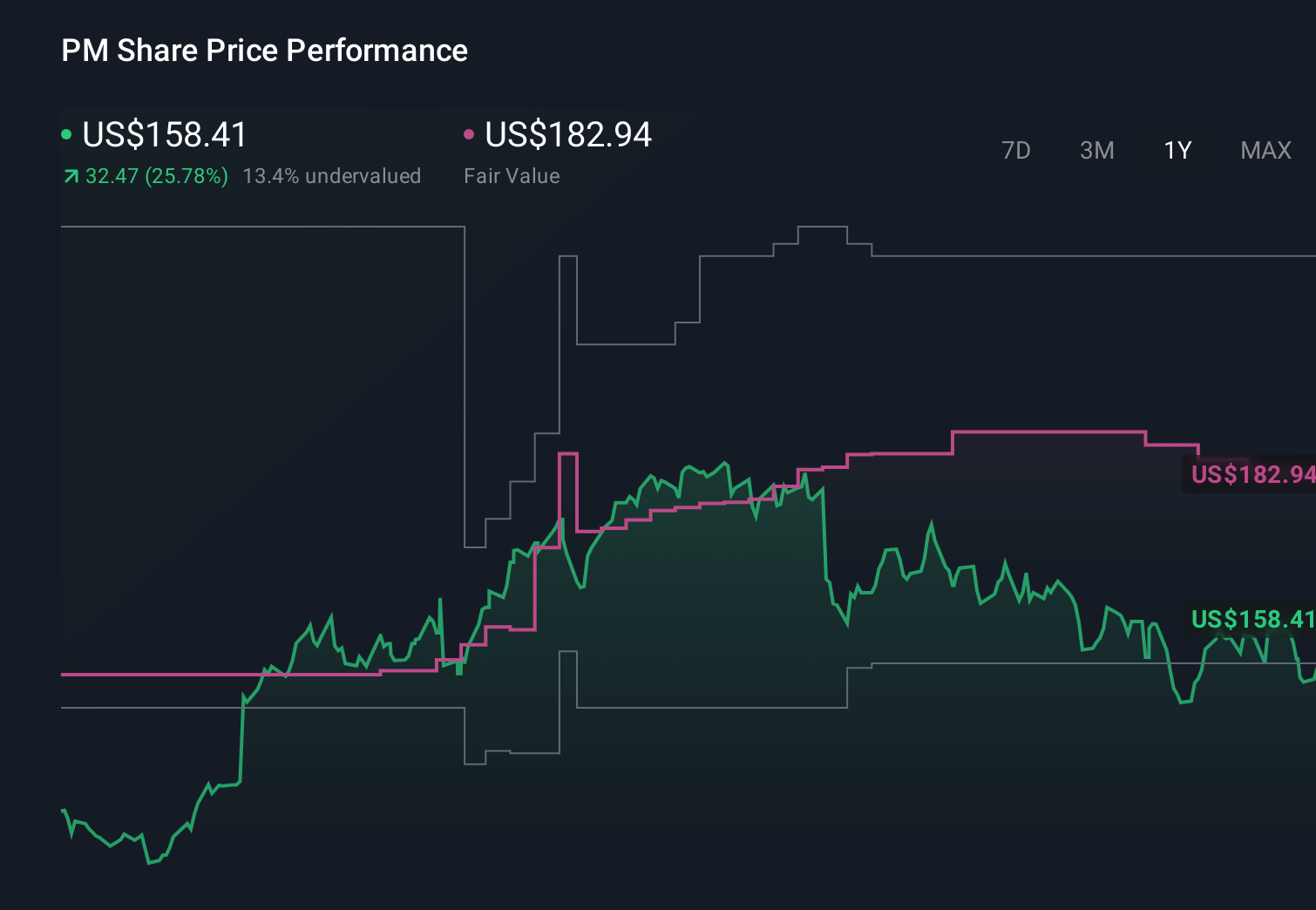

Philip Morris International's narrative projects $50.2 billion revenue and $15.4 billion earnings by 2029. This requires 6.5% yearly revenue growth and about a $4.3 billion earnings increase from $11.1 billion.

Uncover how Philip Morris International's forecasts yield a $192.60 fair value, a 6% upside to its current price.

Exploring Other Perspectives

While consensus focuses on steady smoke free growth, the most optimistic analysts were penciling in revenue of about US$52.2 billion and earnings near US$15.7 billion, which could look either ambitious or achievable once the CFO transition and fresh regulatory signals are fully reflected in the numbers.

Explore 9 other fair value estimates on Philip Morris International - why the stock might be worth as much as 15% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Philip Morris International research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Philip Morris International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Philip Morris International's overall financial health at a glance.

Interested In Other Possibilities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Outshine the giants: these 13 early-stage AI stocks could fund your retirement.

- The future of work is here. Discover the 35 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.