Is Q2 Results And A UBS Downgrade Altering The Investment Case For Moelis (MC)?

Moelis & Co. Class A MC | 0.00 |

- On July 29, 2026, Moelis & Company released its second-quarter 2026 results after the market closed and hosted a same-day webcasted conference call led by its CEO and CFO to review the numbers and answer investor questions.

- Just weeks earlier, a UBS analyst had downgraded Moelis, arguing that market expectations for advisory revenue and earnings were too optimistic and pointing to insider share sales as a possible signal of weaker near-term confidence.

- Against this backdrop of an analyst downgrade flagging potentially over-optimistic earnings expectations, we'll examine how these developments reshape Moelis's investment narrative.

We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Moelis Investment Narrative Recap

To own Moelis, you need to believe in its advisory-focused model, its ability to retain top rainmakers and its discipline on compensation and costs. Right now, the key near term catalyst is whether upcoming deal activity translates into consistent advisory fees, while the biggest risk remains earnings volatility from a lumpy, transaction-driven revenue base. The UBS downgrade mainly challenges near term earnings expectations rather than altering that core thesis, but it does highlight how sensitive sentiment is to any perceived setback.

The most relevant recent announcement is Moelis scheduling its Q2 2026 results and same day Q&A call on July 29, 2026. With an analyst downgrade already questioning earnings expectations and insider selling, this update becomes a focal point for assessing whether revenue trends and margins support the current valuation, and how management talks about deal pipelines, hiring and costs against the backdrop of an event-driven earnings profile.

Yet behind the upbeat long term story, the risk that large, irregular deals can swing quarterly results is something investors should be aware of...

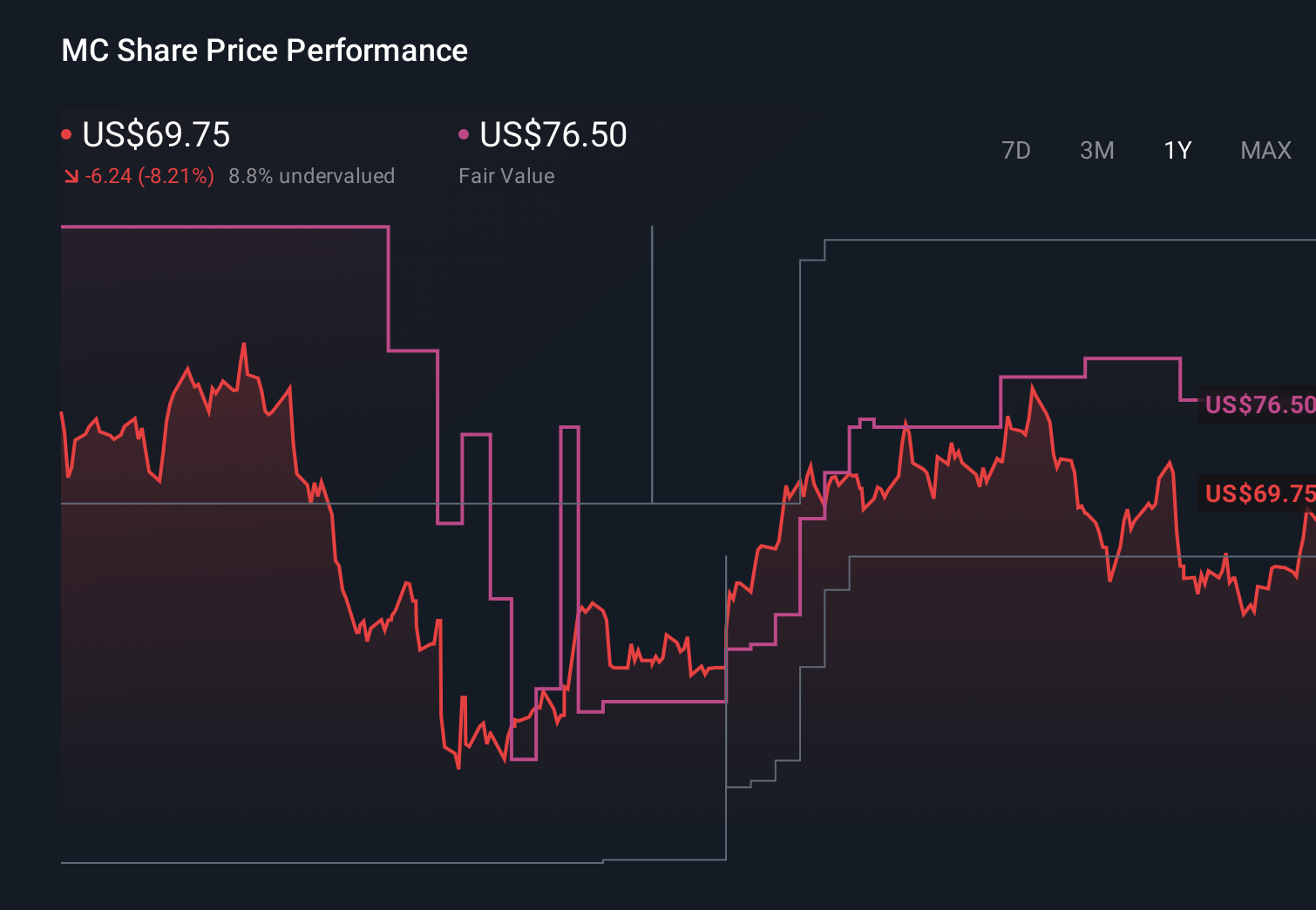

Moelis' narrative projects $2.4 billion revenue and $351.6 million earnings by 2029.

Uncover how Moelis' forecasts yield a $71.00 fair value, a 10% upside to its current price.

Exploring Other Perspectives

Before this news, the most optimistic analysts were assuming Moelis could reach about US$2.6 billion in revenue and US$320 million in earnings by 2029, yet the recent downgrade and questions around deal lumpiness show just how differently you and other investors might view both the upside and the risks.

Explore 3 other fair value estimates on Moelis - why the stock might be worth just $71.00!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Moelis research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Moelis research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Moelis' overall financial health at a glance.

Contemplating Other Strategies?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

- Find 44 companies with promising cash flow potential yet trading below their fair value.

- Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.